S’pore households should stay prudent in making big financial commitments, including property: MAS

Sign up now: Get ST's newsletters delivered to your inbox

MAS noted that while outstanding mortgage loans have risen, household financial assets have grown faster than household debt.

ST PHOTO: LIM YAOHUI

SINGAPORE - The current trend of lower interest rates is helping Singapore households take out cheaper mortgages, but they should be careful when making big financial commitments, given uncertainties in the global environment, the central bank said on Nov 5.

The Monetary Authority of Singapore (MAS) in its annual financial stability review said: “Households should continue to exercise prudence in making large financial commitments, including property purchases.”

They should also maintain sufficient liquidity buffers, given the uncertain macro-financial environment. Due to the uncertainties, labour demand is expected to soften, with nominal wage growth moderating, it said.

MAS noted that while outstanding mortgage loans have risen, overall household sector vulnerabilities remain low as household financial assets have grown faster than household debt.

The authority’s latest stress test of households, where it incorporated a 20 per cent cut in household income and a 100-basis-point increase in mortgage rates, found a significant majority of households have the capacity to manage an income shock and higher debt-servicing costs.

But 1 per cent of households could face negative cashflows, with savings buffers that cover less than six months of this shortfall.

Among these vulnerable borrowers, the majority are middle-aged, comprising a mix of lower-income HDB dwellers with tighter cash buffers and upper middle-income segments with sizeable outstanding private housing loans, MAS said.

It said the Government would remain vigilant to evolving market developments, with the objective of ensuring a stable and sustainable private housing market.

Private residential property transaction volumes have picked up recently, driven by a strong recovery in new sales.

Average quarterly volumes in the first three quarters of 2025 exceeded average levels observed over the past three years. New sales increased firmly compared with the same period in 2024 as project launches saw firm take-up, while resale volumes also held up.

The pace of private residential property price increases has been more measured in 2025, averaging about 0.9 per cent over the first three quarters.

MAS said macroprudential and property market measures have restrained excessive demand, while the release of private housing sites via the Government Land Sales programme has ensured an adequate supply of new private housing.

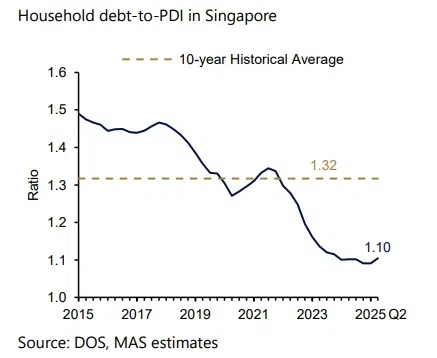

Outstanding mortgage loans have increased in Singapore, but household leverage risk is under control. In the second quarter of 2025, household debt increased by 6.1 per cent year on year, but household financial assets expanded by a faster 8.5 per cent.

Income growth has also kept pace, holding the household debt to personal disposable income ratio stable at 1.1.

The increase in debt was led by mortgage loans that are secured by property as collateral. This has been in line with a pickup in transaction activity in the property market, MAS said.

Debt-servicing capacity has remained healthy, underpinned by stable income growth and lower mortgage rates.

With the decline in the Singapore Overnight Rate Average over the past year, borrowers across all income profiles who refinanced into lower-rate packages have seen their mortgage servicing-to-income ratios fall.

The median mortgage rate for newly originated loans has fallen by around 90 basis points since the second quarter of 2024.

The credit quality of housing loans extended by financial institutions has also remained strong, with the non-performing loan ratio at a low of 0.3 per cent as at the second quarter of 2025.

Liquidity risk for households – the risk that a household cannot meet its short-term expenses and financial obligations because it lacks enough cash or assets that can be quickly converted to cash – remained low. This is because the growth in cash and deposits has kept pace with that of shorter-term household liabilities.

The ratio of personal loans to personal disposable income has been stable at a low of around 0.3 over the past year.

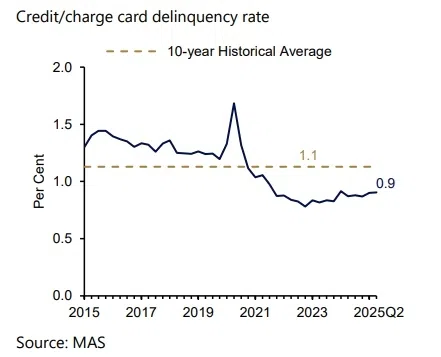

On credit card loans, MAS said the rollover balances as a share of personal disposable income edged up to 2.5 per cent in the second quarter of 2025, extending the uptrend since 2022.

A large majority of borrowers continue to be able to service their credit and charge card debts, as delinquency rates have remained low at 0.9 per cent.