SINGAPORE - Even after its proposed acquisition of Singapore Press Holdings (SPH), Keppel Corp expects to have sufficient firepower for more investments in other growth segments "to create new profits to pay dividends in future".

Speaking to media and analysts on Monday (Aug 2) morning, Keppel Corp chief executive Loh Chin Hua noted that the group has sufficient debt headroom for other initiatives.

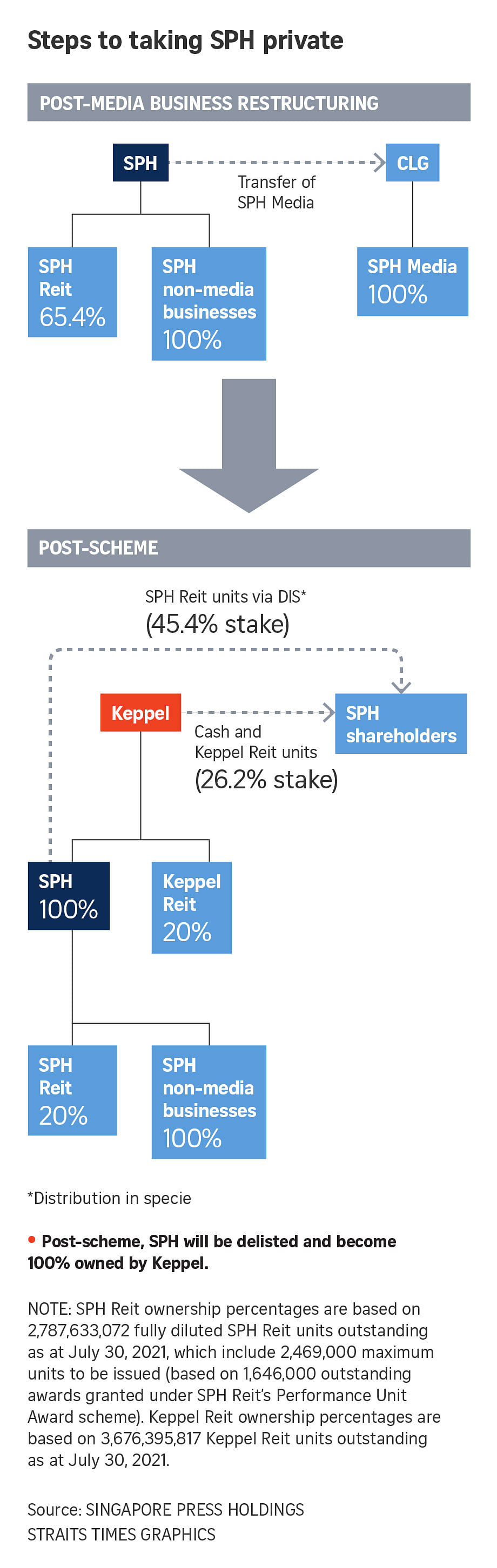

Keppel proposes to acquire SPH through a privatisation offer after SPH's media business has been hived off.

The offer, which values SPH at $3.4 billion, will see SPH delisted and become a wholly owned subsidiary of Keppel, the companies jointly announced on Monday.

Keppel's share of the deal is about $2.2 billion. Under the offer, SPH shareholders will receive a total consideration of $2.099 per share. This will comprise cash of 66.8 cents per share, 0.596 Keppel Reit unit (valued at $0.715) and 0.782 SPH Reit unit (valued at $0.716) per share.

The offer price is also equivalent to SPH's adjusted net asset value per share excluding the media business.

Asked why SPH minority shareholders will be attracted to the $2.099 offer, which is close to its book value of about $2.08 a share, Mr Loh said "it is for the SPH board to address to its unit holders".

"But we think it is a win-win for both. This is a unique and rare, attractive opportunity for Keppel and also for SPH unit holders to realise their investment post media demerger," Mr Loh said.

He said that with its asset monetisation plan in place, the group could pivot to new growth engines. "We have enough debt headroom to consider investments in renewables, decarbonisation solutions, and the ability to improve dividend payment to our shareholders.

"As we improve the quality of our earnings, by increasing the proportion of net income recurring, it will give us a better platform to pay dividends to shareholders," he said.

Mr Loh noted that the market has already "taken a shine" to Keppel raising its interim dividend to 12 cents a share, four times the dividend in the same period of the previous year. This is due to Keppel's return to profitability for the first half of the year, on the back of positive contributions across most of its units.

"We still need to invest to create new profits to pay dividends in future," Mr Loh said.

Under the terms of the scheme, Keppel will offer about $1.08 billion in cash and about $1.156 billion of Keppel Reit shares. SPH will concurrently distribute in specie SPH Reit shares valued at $1.157 billion, while retaining a 20 per cent stake in SPH Reit.

On how the deal will be funded, Keppel chief financial officer Chan Hon Chew said that the $1.08 billion will be drawn from "internal cash, borrowings and its asset monetisation plans".

"We expect another $1 billion from asset monetisations from July 2021 onwards," he added.

Mr Loh said the group's liquidity will remain robust post-acquisition.

From October 2020 to date, Keppel has announced asset monetisation of more than $2.3 billion. About half of the transactions have been completed so far, and the group has received cash of about $1.15 billion from October 2020 to end June 2021.

"Following this transaction and as we continue our asset monetisation programme, our leverage is expected to remain below 1.0x.

"We have said before that Keppel does not need to hold all of our current 46 per cent stake in Keppel Reit. The utilisation of Keppel Reit units to partly satisfy the scheme consideration allows us to limit the impact to our gearing."

He said one could expect further deleveraging over time at Keppel.

"This will in turn grow the asset management business and drive the growth in recurring fee-related income," Mr Loh added.

SPH's businesses and assets fit well in the Keppel ecosystem, he said.

The largest segment is asset management, which includes SPH's Student Castle and Capitol Students PBSA (purpose-built student accommodation) platform, which has grown over the past few years to become a large PBSA owner-operator in the UK, he said.

SPH Reit owns some of the highest quality and scarce retail assets in Singapore, including medical suites within Paragon; and the senior living business, comprising Orange Valley in Singapore and a portfolio of nursing homes in Japan.

Within the urban development segment, it had Seletar Mall, as well as the Woodleigh integrated development that is currently under construction.

"These assets generate recurring investment income, and will accelerate our plans to pivot Keppel Land's business model from residential trading with lumpy earnings towards more recurring income as an urban solutions provider," Mr Loh said.

"These assets may also potentially be pipeline assets for injection into our asset management platform," he added.

In particular, the acquisition of the SPH Reit platform will give Keppel the opportunity to tap the recovery and growth in the retail sector.

Mr Loh said: "While the retail sector has been affected by Covid-19, we note that the SPH Reit portfolio both in Singapore and Australia, particularly its suburban assets providing essential retail, has shown resilience during the peak of the pandemic.

"With continuing vaccination and progressive reopening of borders, we expect the retail market to further improve, particularly for prime downtown assets like Paragon, which could rebound sharply as more borders reopen. As it currently stands, SPH Reit's distributions have already rebounded to near pre-Covid-19 levels with portfolio occupancy averaging above 90 per cent."

Keppel and SPH are already close partners in M1 and the Genting Lane data centre project. The move to acquire SPH will streamline decision making, he said.

Asked if a partial sale of M1 will occur soon, Mr Loh said "M1 remains an important part of the group in the connectivity segment.

"M1 is in a multi-year journey to transform itself from telco to a cloud native connectivity platform. We are focused on that, so it makes more sense for M1 to remain private for now.

"This will make M1 into a very important growth engine for the group, especially with the launch of 5G on consumers and businesses," Mr Loh added.