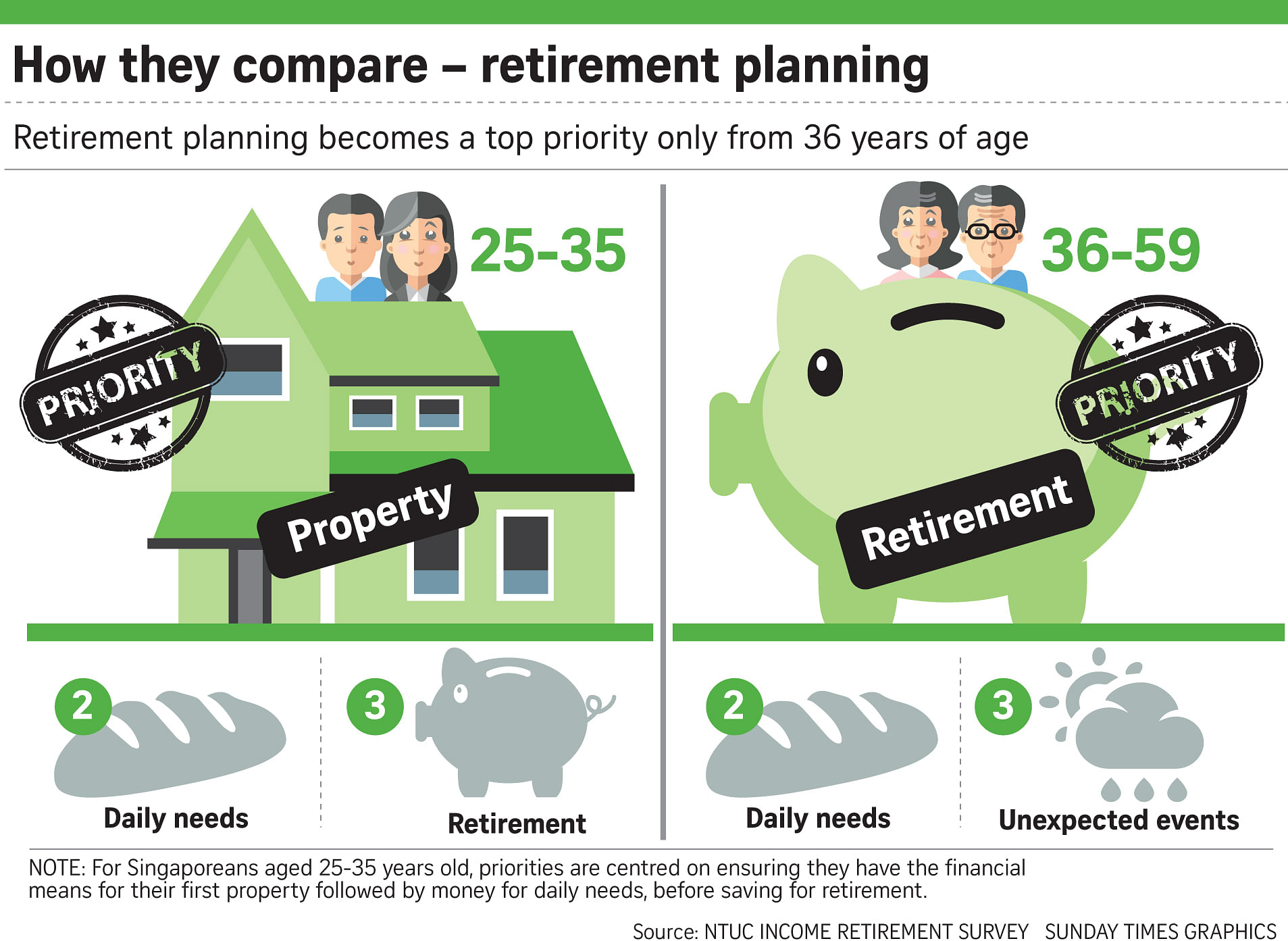

Last month, more than 15,000 university students graduated here. Now that they are entering the workforce, these millennials should set up a financial plan, whip their money management habits into shape and adopt financial discipline .

Experts say it is never too early to start. In fact, surveys have shown that the main reason most people cannot retire comfortably is that they started saving only around their 40s.

Ms Shirley Tan, head of marketing and customer experience at Etiqa Insurance, said the big advantage millennials have is time.

"Millennials are in the best possible position to get started, with about 40 years to save for retirement, and whatever they contribute will grow and accrue interest greatly over time," she noted.

Manulife Singapore said that its latest Manulife Investor Sentiment Index - carried out in March this year - shows a gap between millennials' expectations of their retired life and the steps they are taking to achieve those financial goals.

For instance, eight out of 10 millennial investors expect their lifestyles to remain the same, but only five out of 10 say they are on track to achieve that.

Retirement might seem far away, when in reality you are in the best position to plan for your future during the prime of your life, said Manulife.

Recognising that graduates should embark on their investment journey as early as possible, DBS Bank recently launched NAV Hub in Tanjong Pagar, which is targeted at young adults. They can enjoy free personalised financial planning sessions conducted independent of sales, and with no products sold.

The Sunday Times highlights what millennials should be thinking about when it comes to savings, insurance and investments.

Savings

1. SAVE AT LEAST 10 PER CENT OF INCOME

Mr Brandon Lam, Singapore head of financial planning group, DBS Bank, advises millennials to set aside savings of at least 10 per cent of their income on a recurring basis.

They should also set aside at least three to six months of their monthly expenses as liquid cash savings for contingencies.

2. CULTIVATE THE SAVING HABIT

Ms Shirley Tan, head of marketing and customer experience at Etiqa Insurance, said it is important to start cultivating the habit of saving as soon as you get your first pay cheque, whether it is saving for retirement or for big milestones to come.

"The value of compounding means you will have to set aside less later, whereas the amount you have to contribute per month goes up as you put it off for later. The key is to start small, but save regularly," she said.

3. PAY OFF STUDY LOANS

Graduates who have taken study loans should have a plan to pay off the outstanding amount by allocating a part of their income towards this, said Mr Lam.

Interest that is charged on the borrowed amount will be compounded over time, so it is financially prudent to redeem the loan as early as possible.

Insurance

1. ADDRESS YOUR NEEDS

-

Common insurance policies

-

Here's a summary of the common categories of life insurance:

•Term insurance covers you for a specified sum assured for a fixed term, for death, total and permanent disability, critical illness or other types of coverage. There is usually no cash value at expiry date.

•Whole life insurance covers a specified sum assured until you die or when another specified coverage condition is met (such as critical illness) or when it matures. The main plan usually has cash value.

•Endowment insurance - more for savings - covers a specified sum assured for a fixed term, with a lump sum payout upon maturity.

•Investment-linked insurance invests in sub-funds with insurance protection options. Cash values are based on investment values less charges.

• Critical illness insurance covers you for a specified sum assured for a specified term, against a list of critical illnesses. A variant of this is early critical illness insurance.

•Long-term care insurance covers you for a specified payout for a specified term, against being able to perform a specific number of activities of daily living such as dressing yourself.

•Medical expense insurance covers the likes of certain types of inpatient services, such as surgery, and out-patient treatments like chemotherapy. An age limit may apply or may offer lifetime cover.

•Disability income insurance covers you up to a specified sum assured to an age limit, when you are not able to work or are disabled.

•Annuity insurance provides a lump sum and/or regular payouts for a fixed term or for your lifetime. It helps supplement your income sources and cushions against outliving your resources.

SOURCE: AXA INSURANCE

Ms Pauline Lim, executive director of the Life Insurance Association, Singapore, said millennials should understand how insurance plans can address short- and long-term goals.

They must also consider the sustainability of meeting premium payments throughout the plan's tenure and the penalties should they opt for early redemption.

2. COMPARE FIRST

Compare and find insurance products most suited to your financial objectives.

One website that aggregates life insurance plans is compareFirst, an industry-led initiative.

A purely informational online portal, it does not promote or distribute life insurance products. You will have to buy the product directly from the life insurer or a financial adviser.

Another aggregator to check out is DIYInsurance.

3. TERM INSURANCE

If you have dependants, getting a term insurance plan which provides a payout upon death is something to consider.

4. HEALTH INSURANCE

Equally important is hospitalisation insurance cover such as an Integrated Shield Plan and a critical illness plan to manage any sudden influx of unforeseen expenses, said Ms Lim.

Mr Daniel Lum, director of products and marketing at Aviva Singapore, noted that 37 people in Singapore are diagnosed with cancer every day.

He said: "Critical illness could happen to anyone, and easily racks up hefty medical expenses for those affected. It is best to make sure you have a strong financial safety net to serve both your and your family's regular needs should the worst really occur."

Mr Ryan Sim, deputy vice-president of savings, investment and fund solutions at Prudential Singapore, said that critical illness plans are structured to pay out a lump sum should one be diagnosed with a serious illness such as cancer, and help provide much-needed financial security in times of a health crisis.

Investments

1. COMPOUNDING EFFECT

Once savings and insurance needs are met, any excess funds that may not be required in the short term should ideally be invested for a higher rate of return, said Mr Lam.

This is because starting investing early would enable compounding to work to your advantage.

"If returns and dividends from investments are re-invested regularly, over time, the total investment portfolio value will grow substantially," he said.

Investing would also help to mitigate the effects of inflation. As purchasing power is eroded over time due to inflation, one should always aim to invest at a rate of return above the inflation rate.

2. INVESTMENT OPTIONS

Options include equities, exchange traded funds (ETFs) and unit trusts. Investors who prefer to delegate the task to experts can consider investing in unit trusts or ETFs, and track market indexes.

Single equities may be more suitable for investors who are interested in assuming more control over their investment choices, added Mr Lam.

3. FACTORS TO CONSIDER WHEN INVESTING

Ms Ho Lee Yen, chief marketing officer at AIA Singapore, said that while investing helps you to set aside money for tomorrow, it is important to ensure that current needs are not compromised.

"It is essential to plan how much you can afford to comfortably allocate for investing," she said.

For example, it would not be financially prudent to invest all of your savings over the next 10 years if you plan to buy a home in the near future, she said.

Mr Lam said that your risk profile is another factor to consider before you start investing - how much volatility you can withstand and how much you can afford to risk or lose.

Another common but equally important question is whether you prefer investing a lump sum or investing smaller sums periodically.

Finally, ask yourself: What is your investment horizon and how long do you plan to stay invested?