The belief among many is that millennials have Yolo - you only live once - attitudes and cannot be bothered about undertaking tedious things like retirement planning. Well, think again.

Manulife Singapore has found that one in two millennials, or Gen Y - those between ages 22 and 37 - has started saving for the future, ahead of other generations like the baby boomers (those born between 1946 and 1964) and Gen X (born after the baby boomers but before the 1980s). But its survey also showed that most millennials are likely to splurge their savings on short-term life goals, such as creating an Instagram-worthy home, over saving for retirement.

Mr Tan Kuan Ho, its head of product development, notes that millennials do not like to think about retirement as it reminds them of dying and getting old.

"For young millennials, a potential approach would be to talk to them about the concept of financial freedom so that they can go on living their life and pursuing their passion," he says. "Financial freedom is the ability to pay for your lifestyle through the rest of your life without relying on a regular salary."

Mr Brandon Lam, Singapore head of financial planning at DBS Bank, says everyone needs money now as well as in the future, so it is important to include some aspect of forward financial planning.

"Though retirement seems far off to a millennial, small well-informed decisions made today can make a significant, positive difference down the line," he adds.

The Sunday Times lists nine financial planning tips for millennials.

1. Start early

It is never too early to start and the big advantage millennials have is time. Mr Ben Fok, chief executive of Grandtag Financial Consultancy (Singapore), says: "Millennials, being young, should take advantage of time and start early in financial planning, which can include retirement planning.

"With about 40 years to save for retirement, it might seem far away but whatever they save or invest will grow and accumulate over time. Being a millennial, you are in the best position to plan for your future during the prime of your life."

Mr Lam notes that with longer life expectancies and increasing costs of living, it is prudent to start at the earliest opportunity.

2. Cultivate proper money management habits

Start planning by taking an honest look at your finances and draw up a simple, personal, "money in, money out" balance sheet so you know where your cash goes.

"From there, you can make adjustments to cut back on luxuries, reduce debt, start saving or set aside designated amounts for savings and protection," advises Mr Lam.

"Make use of free digital financial planners, such as the DBS/POSB Your Financial GPS that is available via DBS/POSB iBanking and mobile banking, to track expenses automatically and set and track budgets/savings goals any time, anywhere."

Mr Fok says it is crucial to have proper money management habits such as saving first and not spending as soon as you receive your first pay cheque.

Ask yourself this question: Do you spend first, then save the balance, or you save first, then spend the balance? Once you understand the importance of this question, you will be more prudent with your spending. The key is to start small but save regularly, he adds.

3. Set financial goals

Mr Tan suggests asking yourself when you would have to achieve financial freedom and what is your preferred lifestyle.

"Work out how much money you will need when you retire to provide for your desired lifestyle. As a rule of thumb, you should aim to draw an amount of at least two-thirds of your monthly income. The amount will vary from person to person, depending on the lifestyle each person wants," he adds.

Having a huge goal can be intimidating, and when that goal is for retirement, there can be a strong temptation to procrastinate.

"Set up different accounts for different goals and top them up round-robin rather than sequentially," adds Mr Lam.

4. Set aside emergency funds

Be prepared for an unexpected financial crisis by setting aside at least six to 12 months of your monthly expenses as liquid cash savings. Once you have taken care of this for emergency purposes, then you can start thinking about investing.

5. Avoid bad debts

If you have a study loan, you should have a plan to pay off the outstanding amount by setting aside a part of your income, says Mr Fok.

Avoid incurring credit card debt as the interest is very high. Note that it is easy to get into credit card debt if you continue to spend and not pay down what you owe.

You will likely pay an effective interest rate of more than 20 per cent a year, so develop a habit of paying your bills in full every month. Paying just the minimum monthly repayment will take a long time to reduce the debt as most of the payment comprises interest.

6. Think health insurance

Consider buying life insurance plans to hedge against premature death, illness and hospitalisation. It is better to buy such plans when you are still healthy and insurable. Once your health changes, you will be unable to buy or there might be exclusions or the cover may cost more. When buying insurance, consider whether you can afford the premium payments.

7. Consider compounding

Savvy millennials can use the long time horizon to their advantage by exploiting a concept known as compounding. This allows gains to be continually reinvested over time.

Mr Alfred Chia, chief executive at SingCapital, says a small compound interest coupled with a long enough time period can do wonders.

If a millennial starts saving $2,400 a year from age 25 to 40 (15 years' saving period) at an annual return of 5 per cent, and continues to stay invested at the same return till he reaches 60, his savings would be $158,181.33.

Another millennial who starts saving the same amount annually at a later age - from 40 to 60, or 20 years of saving - will accumulate only $90,012.51, despite saving for a longer period, he says.

8. Invest

Once savings and insurance needs are met, any excess funds not required in the short term should ideally be invested for a higher rate of return, says Mr Fok.

"There are many options, including equities, exchange-traded funds (ETFs) and unit trusts. If you do not have investment knowledge, then you can consider managed funds such as unit trusts. But if you have an investment background, then passive investments like ETFs will be suitable," he adds.

Mr Lam suggests investing designated amounts in a disciplined way. "Empower yourself by doing some research to learn about basic investment and protection products and concepts... so you can make informed and confident decisions. Stay steadily invested for the long term and avoid panic when the markets rumble," he says.

9. Plan multiple income flows

Mr Tan suggests regularly evaluating your investment portfolio and determining how much guaranteed and non-guaranteed incomes it can provide.

"Ask yourself what happens to your stream of income if there is a market downside and how your portfolio can benefit from a rising market. Your financial portfolio should be flexible to give you control over your investment," he says.

Savings plans and products to suit different needs

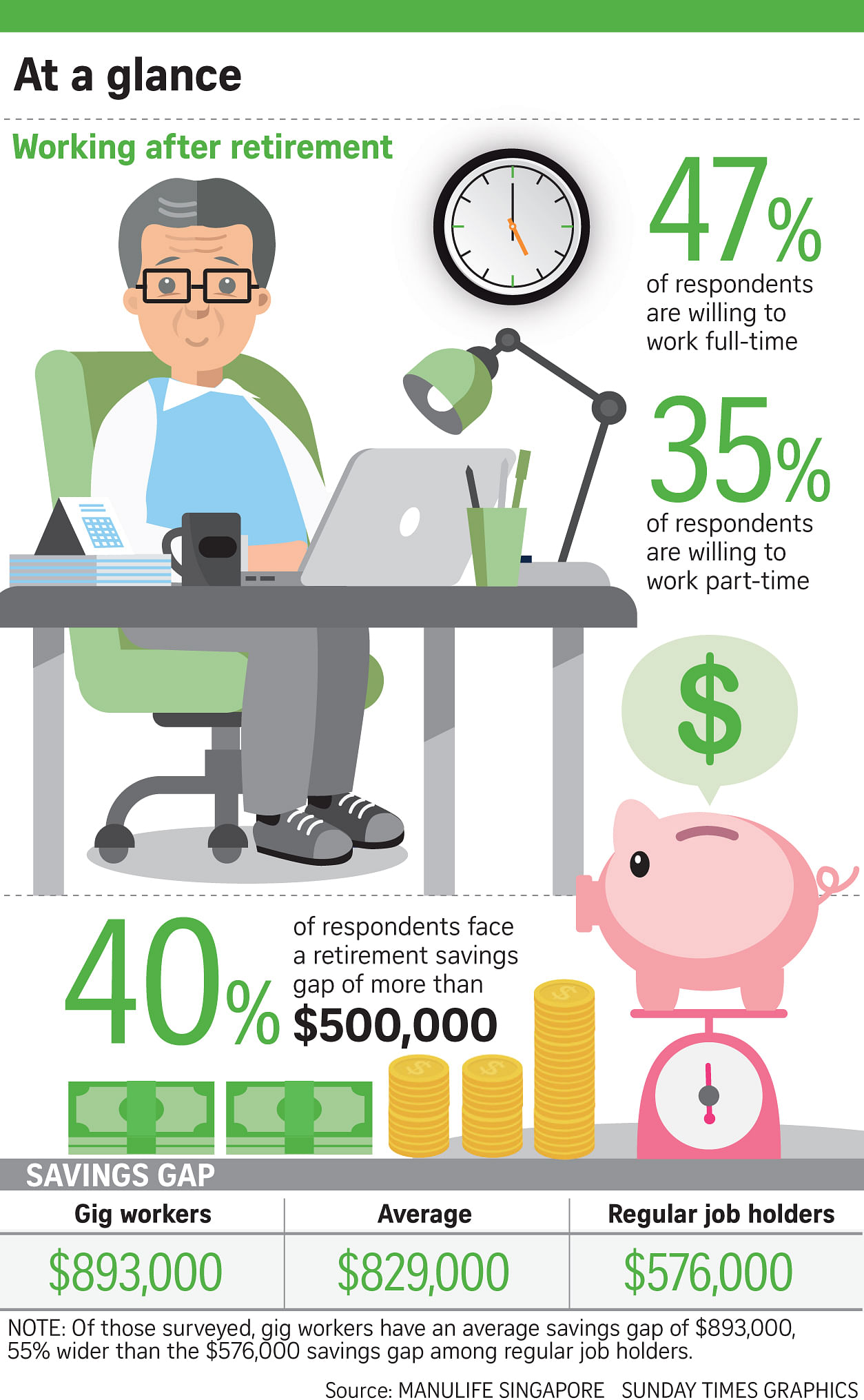

A Manulife Investor Sentiment Index noted that workers in the gig economy have an average retirement savings gap of $893,000, 55 per cent wider than the $576,000 savings gap among regular employees. The research polled 500 respondents here and was carried out between May and June.

Mr Brandon Lam, Singapore head of financial planning group at DBS Bank, says a considerable challenge facing freelancers is the irregularity of income. Once a pay cheque comes through, there could be accumulated bills to pay or a strong urge to "reward myself". Financial discipline is crucial.

Mr Tan Kuan Ho, head of product development at Manulife Singapore, advises that since they do not have a fixed income, it is important for them to start a disciplined savings plan. "Besides aiming to achieve returns higher than inflation, they should also ensure that there is financial flexibility in their investment portfolio."

Mr Ben Fok, chief executive of Grandtag Financial Consultancy (Singapore), suggests freelancers save more whenever they can and keep their savings fairly liquid, as having a healthy bank balance is crucial to help cover unexpected expenses and large tax bills.

Mr Lam suggests buying insurance cover to guard against disability or loss of income so that loved ones are provided for if a crisis hits. He also advises contributing to the Central Provident Fund (CPF) savings voluntarily to benefit from the national annuity CPF Life scheme that supports retirement planning. Last year, 42.6 per cent of CPF members who turned 55 were unable to set aside at least the Basic Retirement Sum.

In addition, it is prudent to supplement the payouts from the CPF Life scheme with other income streams. And, says Mr Lam, if you pay personal income tax, you can consider leveraging the Supplementary Retirement Scheme to benefit from deferred tax and disciplined retirement savings. Mr Alfred Chia, chief executive of SingCapital, says it is also prudent to keep proper accounting to comply with tax laws.

Product recommendations

1. PRODUCTS WITH BUILT-IN DIVERSIFICATION FOR BETTER RISK MANAGEMENT

As a novice investor, it can be difficult to determine which one company to invest in. Investing in a product like an exchange-traded fund (ETF) or unit trust gives you exposure to a range of companies locally and/or overseas, which helps spread your risks, says Mr Lam.

2. PRODUCTS THAT ARE WITHIN YOUR INVESTMENT BUDGET

While some products have a minimum investment sum that can be in the tens of thousands, there are many options with lower minimum sums available. For example, the minimum investment amount for the Singapore Savings Bond is $500, and the monthly investment amount for a regular savings plan in an ETF or unit trust is $100.

3. INSURANCE PRODUCTS

Manulife's ReadyBuilder encourages customers to start with a good savings habit in an insurance savings plan that is stable with potential high returns. Besides offering the freedom to withdraw the cash value for any life goals, it provides the flexibility of ceasing premium payments so you can take a two-year interest-free loan in times of financial difficulties.

For more information, check out https://www.manulife.com.sg/our-solutions/save/savings-plans/readybuilder.html

Manulife's InvestReady product lets you accumulate wealth through regular contributions to a suite of professionally managed unit trusts. It lets you control your portfolio according to market movements, with unlimited free fund switches and flexibility to stop paying the premium if needed. Free funds units are given with welcome and loyalty bonus. You can choose to generate a stream of income by investing or switching to dividend paying unit trust funds when you need it.

For more information, check out https://www.manulife.com.sg/our-solutions/invest/investment-linked-plans/invest-ready.html

Lorna Tan