The ElderShield Review Committee's interim report released last month may have addressed some big issues, but it was rather disappointing in not grappling with what people were really concerned about.

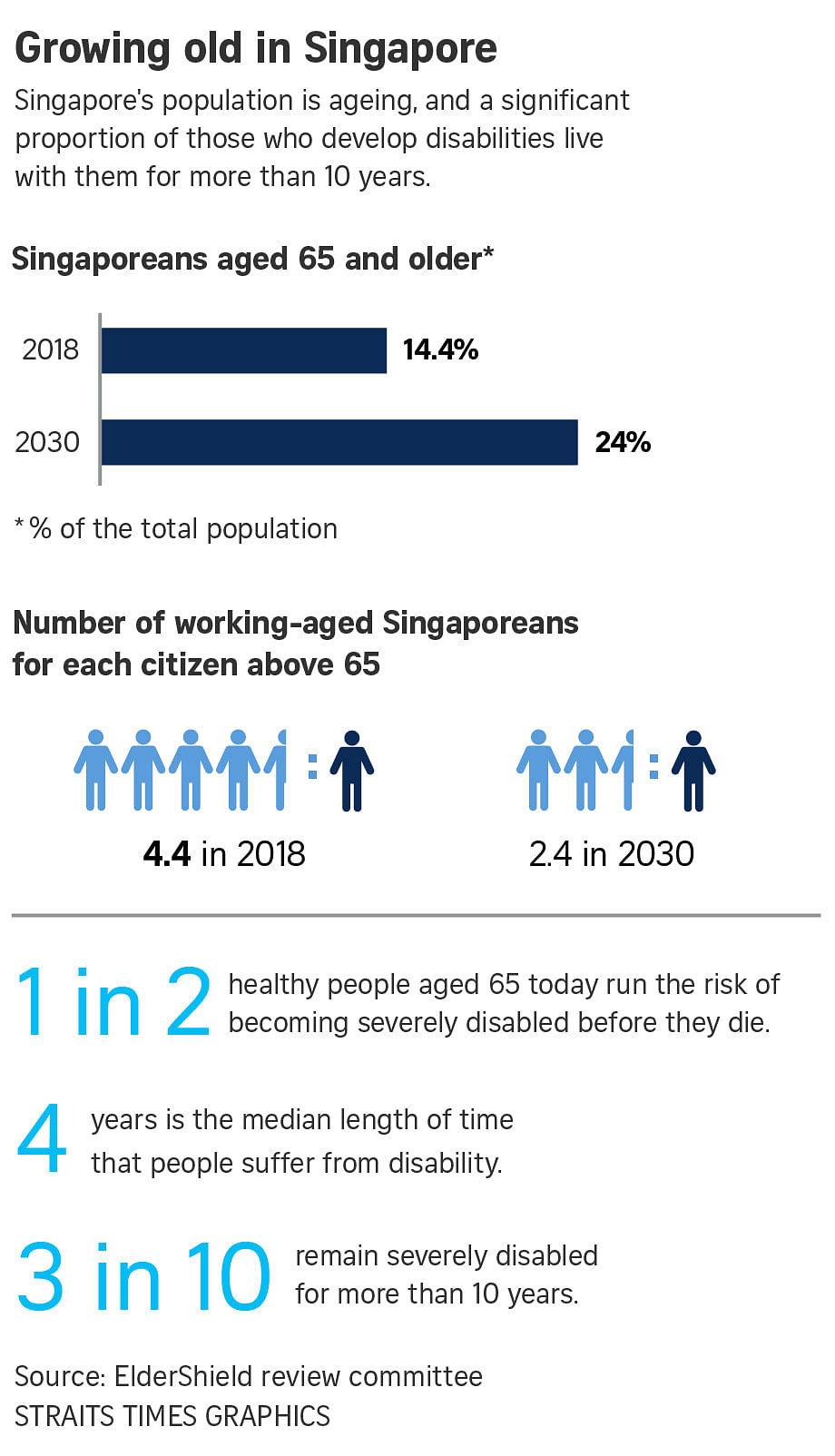

ElderShield is a disability insurance that pays people who need help with at least three daily living activities - such as eating, bathing and going to the toilet - $400 a month for six years.

The committee was set up in late 2016, so it has been working on this for more than a year.

Yet all it has come up with was to suggest that people should join at a younger age (30 years, as opposed to 40 years today); that it should be made compulsory; that the Government should take over the running of the scheme and help poorer people pay their premiums; and for the claims process to be easier.

While some may say that these cover the big issues, in fact the committee has not addressed what most people were waiting to hear:

• Will payouts be higher than the current $400 a month, which many have complained is not enough even to hire a helper?

• Will payment go on for more than six years, when data shows that one in three lives 10 years or more after disability has set in?

• Will premiums go up, or remain as it is at $174.96 a year for men and $217.76 for women, given that people will pay premiums over a longer period of time since the starting age will drop to 30 years?

• Will there be any change to the conditions that entitle people to start collecting from the long-term care insurance?

To be fair, the ElderShield review report was an interim one, and fuller recommendations are expected at mid-year.

In contrast, the MediShield Life Review Committee produced its full report in under a year. And its task was arguably more difficult, given the complexities of big healthcare bill coverage.

RECOMMENDATIONS

So let's look at what the ElderShield Review Committee has recommended:

• That the Government helps the poor pay premiums.

This is a good idea. The Government already does this for MediShield Life (the national health insurance plan used mainly for hospital care), so such subsidy will likely be forthcoming. This is especially since government aid will be needed, should the poor, who can't afford ElderShield premiums, not get any insurance payout to help them over this difficult time of their lives.

But how much aid should the Government provide and for whom? Since premiums, which come from Medisave, come up to less than $20 a month, only the very poor will need help.

• That the claims process be made easier.

Today, there is a panel of about 140 general practitioners who get to decide who qualifies for ElderShield, when they assess people for their ability to dress, walk around at home, get out of bed, go to the toilet, eat, as well as transfer, for example, from bed to wheelchair.

The committee suggested hospital professionals such as occupational and physiotherapists be also allowed to decide on a person's disabilities. This is a good suggestion, and something that should have been done long ago.

It should not be limited to acute hospitals, but include also community hospitals where most people who need assistance with daily living go for rehabilitation. In fact, such assessments should be extended to professionals at day care centres, since they would know when an elderly client deteriorates to the point where help is needed.

• That the Government take over the running of the scheme.

PREMIUMS AND PAYOUTS

While the reason for this is to remove the profit motive so that more of the premiums will be used for payouts, I question the wisdom of such a move.

Having the Government take over won't make the scheme more sustainable if the premiums and payouts are the same, as are the assessors. The assessors are independent healthcare professionals. They are the ones who decide if a person qualifies for aid, not the insurance company.

Would removing the profit insurers get from running the scheme lead to more money in the payout pool?

That's difficult to say since the Government does not have the expertise insurers have, so it might even end up costing more for the Government to run ElderShield.

And even if it doesn't, surely the Government can't be expected to take over the running of everything just because it would do it for no profit?

• Have people start contributing at a younger age.

The idea is that a longer period of payment would reduce the amount needed to be paid out annually. People pay premiums till the age of 65. Starting at the age of 40 means paying premiums for 25 years while starting at 30 means total premium will be paid over 35 years.

Given these precedents, it is obvious that there are some people who really do not want to be on some schemes, no matter how sensible it appears for everyone to participate.

On a national level, these are good schemes that benefit society as a whole. But not everything that is for the general good should be forced on all. Otherwise, we might as well stop selling sugar and salt, soft drinks, cigarettes, white rice and the like because these are known to be bad for one's health.

Paternalism has to stop somewhere.

By all means, explain, persuade and encourage them to join in. But don't take the decision out of their hands.

People should be given the freedom to decide for themselves if they want to join ElderShield at the age of 30, or later - as is currently possible - and pay higher annual premiums because of their delay. Or not to join at all. They will have to live with their decision. If they suffer for it, so be it. It was their choice.