Investors would do well to buckle up for a rocky ride in 2017, as uncertainties arising from both a Trump presidency in the United States and Britain's yet-to-be-negotiated exit from the European Union look set to give markets plenty of surprises.

For now, a casual observer could be lulled into a sense of upbeat complacency. Wall Street has been setting new highs daily as punters swoon over the tax cuts and fiscal stimulus the President-elect is said to be planning from the Oval Office.

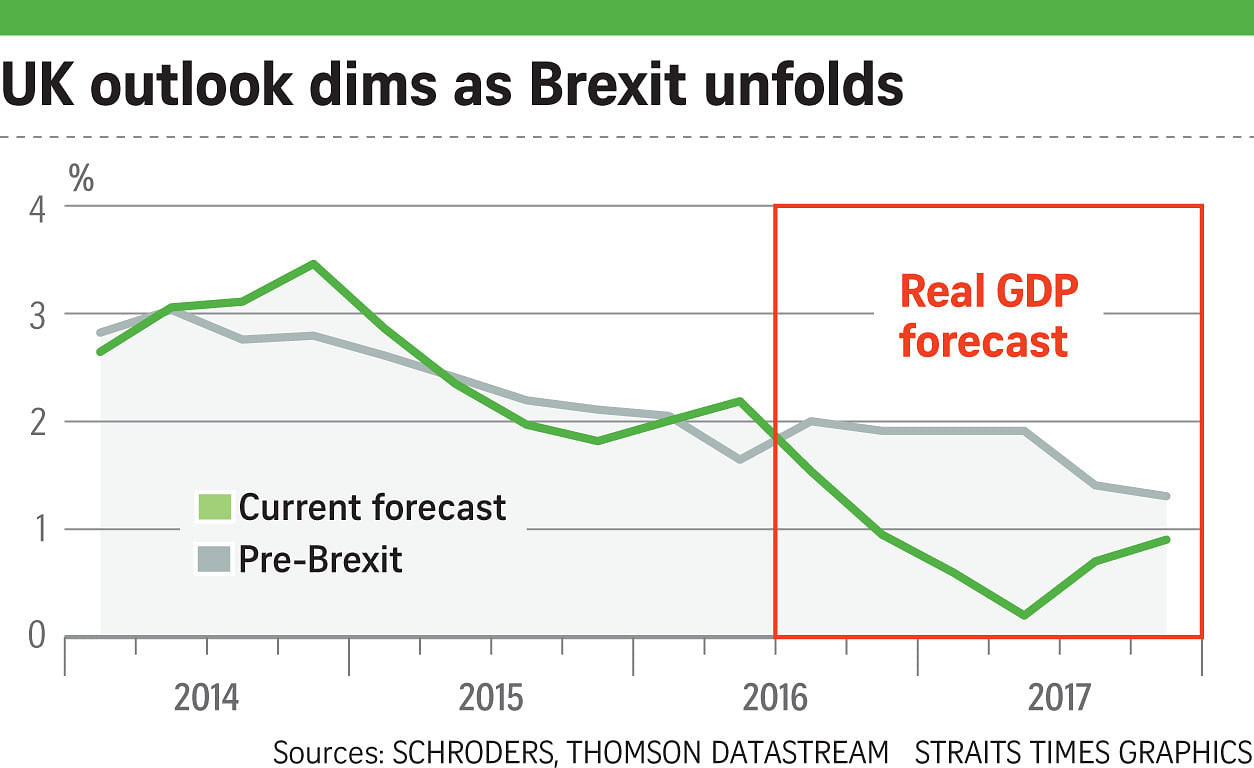

Meanwhile, Britain last week reported retail sales for last month grew at the fastest rate in 14 years as the jobless rate dipped to a new 11-year low in the third quarter.

But top figures at asset management giant Schroders, who gathered last week for its annual London conference, painted a mixed outlook - one with equal measures of uncertainty and opportunity.

WHITE HOUSE MYSTERY

Chief economist and strategist Keith Wade noted massive structural challenges reflected by near-zero growth in global trade, the worst level since the start of 2010, and labour productivity dropping to its lowest since at least the 1980s in both the US and Britain.

Against this backdrop, Mr Donald Trump's promise to create 25 million new jobs and 4 per cent annual economic growth could drive up inflation, while his pledge to raise tariffs, even selectively, could pour more cement onto stagnating trade.

"That will also push up the prices of many consumer goods, and then you'll get stagflation in the US - rising inflation met with slow or no growth," Mr Wade cautioned, while calling the economic rationale for tax cuts "complete nonsense".

In any case, the markets are just betting on what policies might be implemented, which remains very much up in the air, noted US equities portfolio manager Matt Ward.

"We have to be cautious of the timing factor, which the markets aren't taking into account. Trump doesn't get into office until January. He needs to staff up, implement, and all that takes time. We're also talking about a national deficit to the tune of US$5.3 trillion (S$7.6 trillion), not something Congress is totally prepared to tolerate. His policies could face significant pushback, even by the unified government," Mr Ward said, referring to the fact that the Republicans control both houses of Congress.

DARK CLOUDS OVER EUROPE

Across the Atlantic, Brexit will almost certainly bite even if the impact has yet to be fully felt.

"It was always going to take some time before the full impact was felt and spread to companies' capital expenditure, employment and households," said senior European economist and strategist Azad Zangana.

With this in mind, some recent positive headline figures offer scarcely any comfort. They certainly did not impress British finance minister Philip Hammond, who in his Autumn Statement forecast massive growth in borrowings and budget deficits over the coming years.

Mr Zangana said: "Real disposable household income growth in Britain has been coming down in recent quarters, to just around 2.9 per cent year-on-year in the second quarter. If inflation hits above 3 per cent, as we forecast, this will drop to around zero next year. The economy will almost certainly slow, putting more pressure on the sterling next year."

An even greater threat might be looming, with Europe facing multiple elections next year where far-right leaders - including Ms Marine Le Pen in France and Ms Frauke Petry in Germany - could ride to power on a global wave of anti-establishment movements.

These outcomes, while regarded as unlikely, would surely trigger more exit referendums and seal the end of the EU, Mr Wade warned.

OPPORTUNITIES STILL ABOUND

Even so, such complications would not kill the markets. Schroders still sees plenty of opportunities, even if it will take greater skill and a more selective approach to navigate the uneven landscape.

For Wall Street, Mr Ward's team remains keen on the banking, consumer and technology sectors, as fundamentals of the US recovery look intact despite macro uncertainties.

"We've been adding financials, as the net margin story is looking better with the better bond-yield environment. Trump might actually create an environment with less of a regulatory burden, in which case it'll be good for credit growth,'' he said.

The 10-year US Treasury bond yield - commonly seen as an indicator for sentiment over the US economy and inflation - is now close to 2.4 per cent. A yield of 2.5 per cent could be on the cards, and the figure could go up to 3 per cent over the course of the year as the Federal Reserve has virtually locked in an interest rate hike.

A higher US Treasury yield typically means bond prices are falling as people move money into riskier assets such as equities. The yield could also go up if the Fed hikes interest rates or is expected to do so.

"We also see huge opportunities in consumer discretionary, and the stomping grounds are far and wide - e-commerce, retail, auto parts, home improvements. Disruptive technology continues to stand out from the modest growth backdrop," Mr Ward added.

OTHER NICHES TO GROW INCOME

To balance off uncertainties in the US and Europe, emerging market assets are also a key theme for income growth propositions at Schroders.

But a very selective approach and dynamic allocation will be needed, as emerging markets show wide dispersion in returns across asset classes, said Mr Aymeric Forest, Schroders' multi-asset investments head for Europe.

For instance, Indonesian equities have been the outperformer, with rolling 12-month returns of nearly 40 per cent as at Sept 30, but the rupiah offered fairly middling returns of just over 10 per cent for the same period.

Schroders' ISF emerging multi-asset income fund has pared its exposure to Indonesia in a move to take profit, while Brazil and Russia have moved up in allocation priorities.

In contrast, Singapore stocks look rather less appetising.

"Singapore as a trade hub has seen weak growth, with slowing global exchanges of goods and services. Earnings growth has been close to zero, tracking GDP growth, and the Singapore dollar is managed against the US dollar so it's been at a high level, adding to the headwinds," Mr Forest told The Sunday Times.