The New Year market meltdown has understandably unnerved many retail investors but it is not a time to hide behind the sofa and hope it all goes away.

Financial experts say there is no need to wait for clear skies before starting to invest again but they advise you not to put all your eggs into one basket. Instead, spread your investments across asset classes like equities and bonds.

Our new year-long Save & Invest Portfolio Series campaign, which will feature the simulated portfolios of real people - a young working adult, a married couple with two young children and a retiree - aims to encourage investors to invest prudently.

It will guide retail investors in basic investment techniques and how to build a portfolio in accordance with their investment goals and risk tolerance.

This initiative involves the Singapore Exchange (SGX) collaborating with CFA Society Singapore (CFAS) and MoneySense, the national financial education programme.

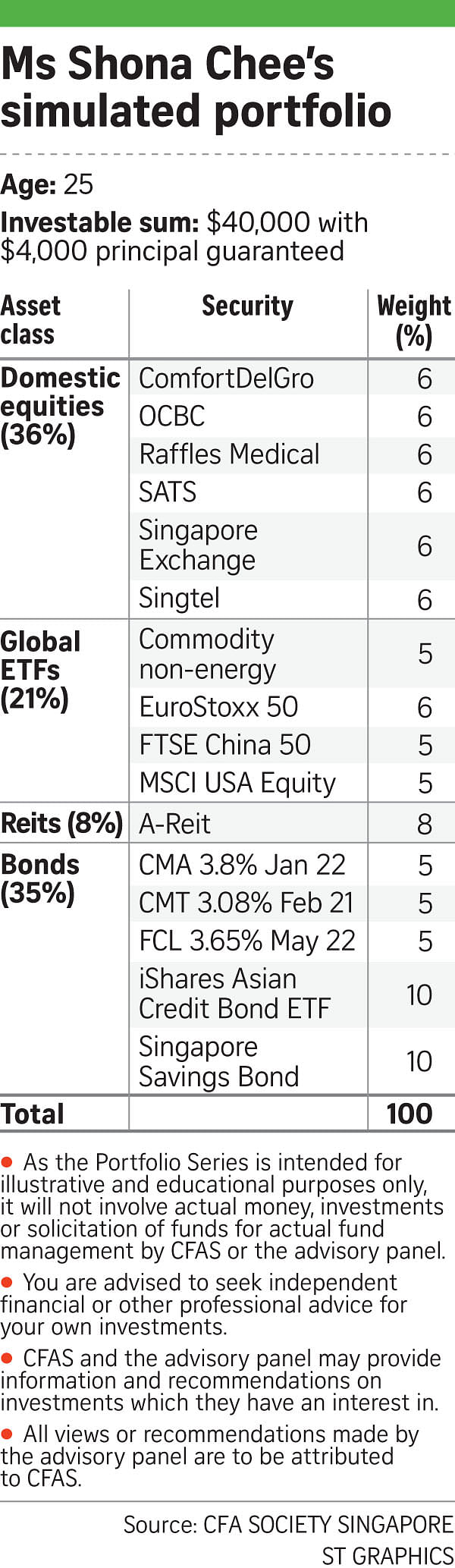

We kick off the series today with a look at one of our retail investors and her customised investment portfolio that has been built by an advisory panel of four CFA professionals.

All three portfolios will go live from tomorrow and The Sunday Times will track them on a monthly basis until the end of the year.

As the Portfolio Series is intended for illustrative and educational purposes only, it will not involve actual money.

There will be similarities in the three portfolio holdings as professional investors typically have a buy-list of preferred securities. The difference, however, is in the allocation for each profile depending on the individual's risk-return objectives.

The simulated portfolios are constructed for an ideal investment time horizon of five to 10 years.

WHAT SHONA CHEE WANTS

Technical account manager Shona Chee, 25, who works in a Fortune 500 tech firm, wants to be financially independent by 40. By then, she plans to enjoy passive income from two rental properties here or overseas.

Ms Chee is aware that many people do not have a financial plan so she would like to buck the trend and start early. After all, time is on her side and she should take advantage of that to leverage the power of compounding.

Ms Chee told The Sunday Times that except for fixed deposits, she has no experience in investments such as stocks or unit trusts.

"I understand the need to invest to make money work harder. I'm wondering what to do with my savings... Recently, I opened a CDP account," she says.

Despite her lack of financial understanding, what places her in good stead is that she is a saver, putting away more than half of her monthly pay and most of her annual bonuses.

It helps that she has minimal financial obligations as she is single, and staying with her parents and two older brothers in a terrace house in the Thomson area. Her parents are still paying the premiums of her insurance plans comprising a critical illness and whole-life plans.

In addition, her employer provides a transport allowance and reimburses her mobile phone bills, so most of her expenses are for meals, entertainment, gym membership and a monthly allowance she gives her parents.

She uses credit cards to chalk up reward points when she dines and shops but diligently pays her bills promptly to avoid the high interest rates imposed on late payments.

After setting aside emergency funds to last 12 months and some cash in fixed deposits, Ms Chee has investable funds of $40,000, of which she would like at least $4,000 to be placed in an instrument that is principal guaranteed.

In the next few years, she might need to liquidate a big portion of her investment portfolio to buy a property.

WHAT FINANCIAL EXPERTS SAY

Given Ms Chee's age, she can afford to ride the market ups and downs and put more of her savings into riskier assets such as equities.

A risk-profiling exercise suggests that she has a balanced risk profile but Ms Chee asked to have a more conservative portfolio to start with until she is more confident and knowledgeable about investing.

The asset allocation of Ms Chee's customised portfolio reflects that of a moderate risk profile with 36 per cent in domestic equities, 21 per cent in global exchange-traded funds (ETFs), 8 per cent in Reits and the balance in bonds.

The CFAS advisory panel said: "Given her young age and needs for principal guarantee, the risk profile of Ms Chee should be moderate. As such, there is a balanced allocation between bonds and equities."

Each domestic equity is kept at 5 per cent to 10 per cent to diversify concentration risk.

The panel added: "Reits give excellent yield and are a natural hedge against inflation, and global ETFs will give an excellent diversification from the domestic market."

The portfolio is limited to Singapore Exchange-listed instruments to keep it easy to monitor, simple and accessible, except for Singapore Savings Bonds, which can be bought via ATMs.

During a meeting where Ms Chee met with the advisory panel to understand how her portfolio was constructed, she expressed her preference for some exposure to the healthcare sector due to the greying population and rapid expansion for medical tourism.

The panellists selected the six stocks for Ms Chee's simulated portfolio as these companies have excellent business fundamentals with capable management and strong balance sheets to weather downturns.

One plus point is that their dividend yields are between 4 per cent and 6 per cent a year. Furthermore, they are generally defensive stocks, which augurs well in a depressed market environment and are not over priced.

Panellist Jack Wang said: "Most of them are consumer staples, meaning that even if the markets are not doing well, you will still need them."

He added that typically, a portfolio should have five to 20 stocks. Too few and it introduces concentrated risks. Exposure to any company should not exceed 20 per cent. If you are more conservative, the exposure should be capped at 10 per cent per stock so that a drop in one share will not affect the entire portfolio.

The portfolio is constructed to deliver "decent" but not tremendous growth. The aim is not to risk your principal and to achieve a reasonable rate of return via thorough analysis of the instruments.

For Ms Chee's simulated portfolio, the panel is looking at annualised returns of 5 per cent to 7 per cent per annum.

The panellists will track the portfolios fortnightly and may consider rebalancing them if the allocation is out by 5 per cent, subject to the dollar value.

Mr Wang encourages Ms Chee to use this opportunity to understand her own investing psychology, for example, to monitor how often she checks on her portfolio.

The rationale for stocks selection is covered in this article, while the other instruments will be covered in greater detail over the next two Sundays.

Meanwhile, you can check out SGX StockFacts (www.sgx.com/ stockfacts) as a tool to analyse SGX-listed stocks. And do look out for details of the first seminar on the Save & Invest Portfolio Series on Feb 20 from 9am to noon at SGX, which would be available soon on www.sgx.com/academy.

Please send your queries on this series to lornatan@sph.com.sg.