The prospect of retiring early at 55 prompted senior tax manager Terry Yeo to embark on financial planning about a decade ago, when he was just 26.

At that time, most of his peers were still ignorant of the benefits of starting this planning process early.

His current portfolio comprises insurance and various investments, and he owns a three-room freehold condominium in Serangoon.

"In my line of work, I can continue to be active in a consultative or advisory role after I retire," said Mr Yeo, 37.

He aims to have a monthly retirement sum of $5,000 for him and his wife, also 37, by the time they hit 55. By then, he hopes to stop working full-time to spend more time with his family, but put in a few days of part-time work per week.

-

Background Story

-

MONEY MATTERS

Money Matters is a new column helmed by Sunday Times Invest editor Lorna Tan on personal finance. Send us your burning questions and financial experts will provide practical tips on how to reach your financial goals. You must be willing to appear online and in the paper and be photographed.

If you would like to be considered, please answer these questions and send them to lornatan@sph.com.sg with the subject header Money Matters.

- Name and age.

- Telephone number and e-mail. (Details will be confidential.)

- Your personal finance questions. (For example, can I retire at 55 and still leave a legacy? Should I cash in my insurance policies? Should I keep my condo and HDB flat or sell one?)

- Your main financial goals. (Give as much detail as possible.)

- Your attitude to investment risk. (Are you a conservative, moderate or aggressive investor?)

Recognising that protection forms the basic block of a financial plan, Mr Yeo is mindful of having sufficient cover as part of his plan.

He tied the knot in 2003 and four years later, when his son was born, the importance of insurance planning grew. His daughter came a year later and he reviews his insurance needs regularly to ensure that they are adequately met.

"Insurance protection is important as it gives me peace of mind," said Mr Yeo. "If something happens to me, I know that my family will be well covered."

As Mr Yeo has a family history of certain medical conditions, he was concerned about covering himself against critical illness as he grew older. His father, a diabetic, died six years ago from a heart attack at 71.

Let's take a closer look at Mr Yeo's insurance policies.

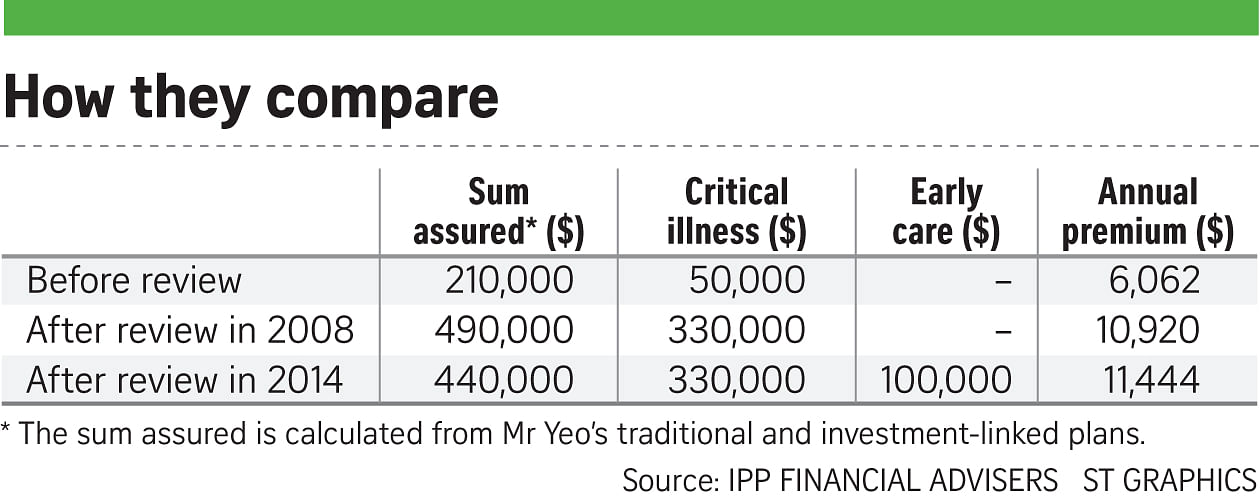

He started out with four policies - a whole life plan, two endowment plans and a regular premium, investment-linked insurance policy (ILP) - which amount to a total sum assured of $210,000 and a critical illness cover of $50,000.

His total annual premiums were about $6,000.

REVIEW IN 2008

In 2008, his financial adviser Loh Lee Theng from IPP Financial Advisers recommended that he boost his critical illness cover to $330,000 by adding two plans - a regular premium ILP and a whole life limited-pay 20-year plan - both of which offer critical illness protection. Mr Yeo also bought private integrated Shield plans for him and his family, which will help cover hospitalisation bills.

Back then, Mr Yeo was aware that he did not need to hold the ILP policy for his lifetime. With an annual premium of $2,400, the plan's sum assured was $180,000 and it came with a critical illness cover of an equivalent value.

At this point, his total sum assured and critical illness cover were $490,000 and $330,000, and the total annual premiums for his plans were about $11,000.

REVIEW LAST YEAR

Mr Yeo wanted to ensure that his critical illness insurance covers him for life without increasing his premiums significantly.

After evaluating his financial plan holistically with Ms Loh, he decided to restructure his insurance portfolio by surrendering his two ILPs and buying another whole life limited-pay policy. The latter requires premiums payments for 25 years and he enjoys a lifetime protection cover as long as he does not surrender the plan. The whole life plan has a sum assured of $230,000 and a critical illness cover of the same value, coupled with an early care cover which covers critical illnesses at different stages of severity.

After these changes, Mr Yeo's total death benefit was reduced marginally to $440,000 while his critical illness cover was maintained at $330,000 with an enhanced early care component of $100,000. His premiums amounted to $11,444.

Said Ms Loh: "Terry is concerned about protection against critical illness and his priority is that it should cover him during his lifetime. If he holds on to the ILPs which have non-guaranteed features such as mortality or protection charges, they will increase as he ages. As he is still healthy and insurable, Terry decided to purchase a new whole life limited-pay policy that has a critical illness cover with an early care feature."

Mr Yeo suffered a shortfall of about $10,000 when surrendering both ILPs as the cash values were lower than the premiums he had forked out through the years.

This could be seen as monies paid for the cost of mortality coverage and investments.

Ms Loh advised those restructuring their policies to avoid surrendering their existing plans till the new plan is under way and the waiting period is over, usually 90 days, as in Mr Yeo's case. This is to ensure that one does not lose protection because of unforeseen circumstances like a medical condition.

INVEST EDITOR SAYS

In 2005, I wrote that certain regular premium ILPs were unsuitable for older policyholders in their 50s and above. This is because they might be unable to continue with premium payments if they had a short investment horizon, as insurance charges would rise to outstrip the premiums and might also eat into the value of the investments.

When this happens, units would be deducted from the investment part of the policy to pay for the increasing non-guaranteed insurance charges when the annual premium becomes insufficient to cover these charges.

If the pool of units runs out, the policy would lapse.

This is especially so if the customer has opted for high protection and smaller investment.

Another category of disadvantaged people would be those who developed medical conditions after buying such plans. While the costs of their ILPs are escalating, they cannot switch to traditional policies as potential exclusions would likely be imposed or, worse still, they could be considered uninsurable. For these policyholders - like the older folk and the ill - they may have to surrender their policies and pay sky-high premiums for a new one or pay the very high cost of continuing with their existing plans.

The controversy surrounding regular premium ILPs resulted in a guide to ILPs issued by MoneySense, the Life Insurance Association and Consumers Association of Singapore in 2005. Some affected policyholders were compensated.

However, this does not mean that regular premium ILPs are a total write-off. It may be suitable for younger policyholders as they are paying a lower premium for protection when they are younger. When they get older, they should review their needs and circumstances to decide if the ILP is still suitable.

There are also some ILPs that are structured differently such that all the single and regular premiums are used entirely for investment.

In the case of Mr Yeo, he made a prudent decision to surrender his two regular premium ILPs, when he was in his late 30s and still healthy and insurable, and bought another policy which provides him with the protection he requires with enhanced critical illness cover. If he had stayed with the two regular premium ILPs, he would have faced the prospect of paying high mortality charges when he got older.

For those who have bought similar ILPs, it may be timely to check with your adviser on how your present cover can be changed to better manage the payment of future premiums as you grow older.

If you have developed illnesses, you may wish to consider lowering the death benefit portion while maintaining the critical illness component so that the overall mortality charge will be lowered.

Better still, do a holistic financial review. Besides age, other factors when looking at your financial plan include financial objectives and your needs, time horizon,budget and risk appetite.