It is a misconception that only the rich need to make plans for leaving wealth behind. In reality, we have a role to play in identifying, preserving and distributing our hard- earned assets, no matter how little there is.

After working hard to accumulate our nest egg for our golden years, many of us tend to overlook the legacy planning aspect.

But when we do undertake it, it's equally if not more important to be aware of the potential administrative costs when it comes to this part of financial planning.

Some people do not know that Central Provident Fund (CPF) savings cannot be distributed via a will and that the Public Trustee charges a fee for administering un-nominated CPF money.

Besides saving on distribution costs, a robust legacy plan will go a long way towards ensuring that we are able to pass on our unused financial resources to our loved ones efficiently.

In the first of a three-part series on legacy planning, The Sunday Times highlights how CPF money is distributed after a member dies.

Recently, some readers asked for greater clarity on CPF nomination. This came after articles highlighting recent enhancements to the CPF system.

The interest is hardly surprising, given that the CPF is an integral part of our retirement plans.

Here's what you need to know about making a CPF nomination and what it covers.

Q Can my nominees receive my CPF savings in cash or in their CPF accounts?

A You can choose the mode of nomination for each nominee. They can receive your CPF savings in one cash lump sum or in their CPF accounts.

The second option was not available before January 2011, which was when the Enhanced Nomination Scheme (ENS) was introduced. Previously, when a member died, the board would distribute his CPF savings to nominees as a cash lump sum according to the proportion indicated in the nomination form.

The ENS option now enables CPF members to transfer their CPF savings to their nominees' CPF accounts when they die. This allows you to help your nominees set aside more money for their retirement and healthcare needs.

Financial experts believe this option is particularly useful for members whose spouses have low or zero CPF balances as it will help ensure that they have a reliable income stream in retirement.

But note that if a nominee is under 18 and not the deceased's widow, the Public Trustee will hold the money until the person turns 18. But if the nominee is the deceased's widow and is under 18, the CPF will pay out immediately.

If there is no CPF nomination, the Public Trustee will hold the money until the beneficiaries (whom the Public Trustee has determined according to intestacy laws) turn 21.

Q How does the ENS work?

A There are two options under the ENS.

•You can choose to credit your CPF savings into your nominee's Special Account (SA) or Retirement Account (RA) first, up to the prevailing Full Retirement Sum (FRS) or Enhanced Retirement Sum (ERS). If there is an excess beyond the FRS or ERS, the funds will be credited to the nominee's Medisave Account (MA), up to the Basic Healthcare Sum (BHS) applicable to the nominee at the time of transfer.

•Another alternative is to credit your CPF savings into the nominee's MA first, up to the BHS applicable to the nominee at the time of transfer. Any excess beyond the BHS will then be credited into the nominee's SA or RA, up to the prevailing FRS or ERS.

Any balance after crediting into these respective accounts will be paid in cash to the nominee. All crediting and payment processes are subject to prevailing CPF rules.

Note that members are not given a choice to credit money to the nominees' Ordinary Account under the ENS. This is because it is meant to enable members to better provide for the retirement and healthcare needs of their dependants.

You are allowed to indicate a single mode of nomination, that is, either cash, ENS or Special Needs Savings Scheme, for the same nominee. Savings credited to a nominee's CPF accounts can only be used or withdrawn in accordance with CPF laws.

Q What will happen to the ENS nominee's share of the CPF monies if he or she dies before me?

A If you do not make a fresh nomination after one of your nominees dies, his or her share will be given to the remaining nominees in the same proportion as their specified shares.

If there are no surviving nominees, the CPF savings will be transferred to the Public Trustee's Office for distribution to family members under the intestacy/inheritance laws.

If the nominee has died after a deceased member and has yet to claim the nominated money, the nominated share of the funds will form part of the deceased nominee's estate.

For a nominee who lacks mental capacity, the deceased member's CPF money will be paid to the Donee or Deputy appointed to act on the nominee's behalf under the Mental Capacity Act. The court is also empowered to make or revoke CPF nominations on behalf of a member who lacks capacity.

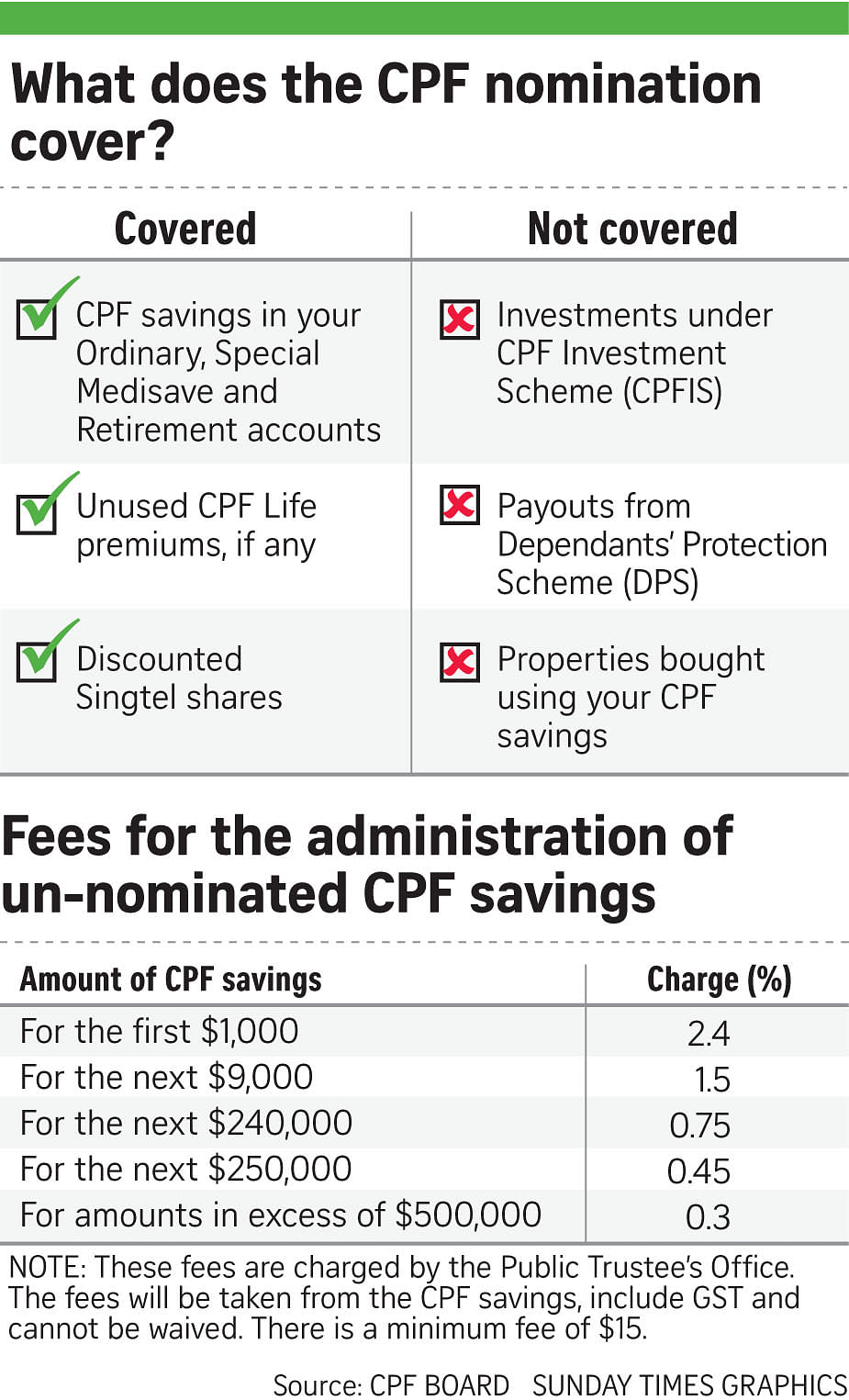

Q What is covered by CPF nomination?

A If you have a valid CPF nomination, the following will be distributed to your nominees in the proportion stated in your CPF nomination upon your death:

•Savings in the Ordinary, Special, Medisave and Retirement Accounts (including unused CPF Life premiums); and

• Discounted Singtel shares bought in 1993 when Singtel went public.

The following assets are not covered by CPF nomination:

•Cash and investments held under the CPF Investment Scheme (CPFIS);

•Dependants' Protection Scheme (DPS) claim proceeds; and

•Properties bought with CPF savings.

For the first item, you may wish to cover them under a will, otherwise they would be distributed according to intestacy laws.

Your DPS proceeds can also be covered under a will or you can nominate your beneficiaries through your DPS insurer, Great Eastern Life or NTUC Income.

In the case of properties, it depends on their holding status. If a property is held with the legal status of "joint tenancy", the deceased's share of it will pass to the remaining surviving owner(s). Otherwise, the share of the property will form part of the deceased's estate.

Q Can I indicate my nominee's share of my CPF funds as a fixed amount?

A The nominee's entitlement to the CPF money should be indicated as a percentage and the total of such entitlement must be 100 per cent.

This is because if there are several nominees and the CPF balance is insufficient at the time of death, the board would not be able to make payment based on the member's intention.

Q If I have already made a will, do I still need to make a CPF nomination?

A Your CPF savings are not covered under your will. They also do not form your estate and are protected from creditor claims on any outstanding debts. This arrangement protects your CPF savings and ensures that your nominees receive your CPF savings expeditiously.

Moreover, if CPF savings are distributed according to a will, any disputes arising from the existence and validity of the will may delay the receipt of the CPF funds by the dependants.

So it is in the interests of both members and their dependants for un-nominated CPF money to be distributed by the Public Trustee's Office in accordance with the intestacy laws (for non-Muslims) of Singapore or the inheritance certificate (for Muslims) to your family members.

You are encouraged to make a nomination if you want to distribute your CPF savings according to your wishes.

Q Are my CPF savings protected from creditors?

A The balance in your CPF is protected from creditors. But any CPF savings used for investments will not be protected from your creditors upon your death.

So if you have creditors, you may want to consider liquidating any CPF investments before death so that the funds are transferred back as your CPF balance and protected.

Q What happens if my spouse and I nominate only each other and we die at the same time?

A Under such circumstances, the older spouse is deemed to have died first. If you are the older spouse, your CPF savings will be paid to your spouse's estate.

If you are the younger spouse, you have no nominee since your spouse is considered to have died before you. Your CPF savings will be distributed according to intestacy laws.

Q When do I make a CPF nomination?

A You don't need to submit a CPF nomination if you have no qualms about your CPF savings being distributed to your family according to intestacy laws.

But if you want to distribute your savings differently, make a nomination. You can then decide who are your nominees, as well as the proportion of the savings you want them to receive upon your death.

Take note that you should make a new CPF nomination when one of your nominees dies; if you want to add a new child or relative to your nomination; when you marry or re-marry or upon divorce.

Getting married renders any earlier CPF nomination invalid. This means that if you do not make a fresh nomination, your CPF savings will be distributed to your family under intestacy laws.

Unlike marriage, divorce does not revoke your previous nomination. This is because you may still want to provide for your ex-spouse and children. But you may want to re-nominate when a divorce takes place.

Q What is the minimum age for making a CPF nomination?

A Once a CPF member reaches 16 years of age, he or she can make a nomination. This minimum age is in line with the minimum age to work and earn wages under the Employment Act.

Q How do I cancel a previous nomination?

A You can cancel by submitting a Notice of Revocation of Nomination. Bear in mind that once you do that, your CPF savings will be distributed according to intestacy laws unless you re-nominate someone else.

Q What is the Special Needs Savings Scheme?

A The scheme encourages parents of children with special needs to save for their long-term care needs. Parents can nominate their children to receive monthly disbursements from the parent's CPF savings after death.

This scheme is administered by the Special Needs Trust Co.