Long queues of well-heeled Chinese tourists outside certain high-end stores were a common sight here just a few years ago.

The shops are now quieter, a stark reminder that when China sneezes, the world really does catch a cold. Concerns over slowing growth in the world's second- largest economy are not new, but fresh worries are surfacing after a bloodbath in its stock markets in recent weeks.

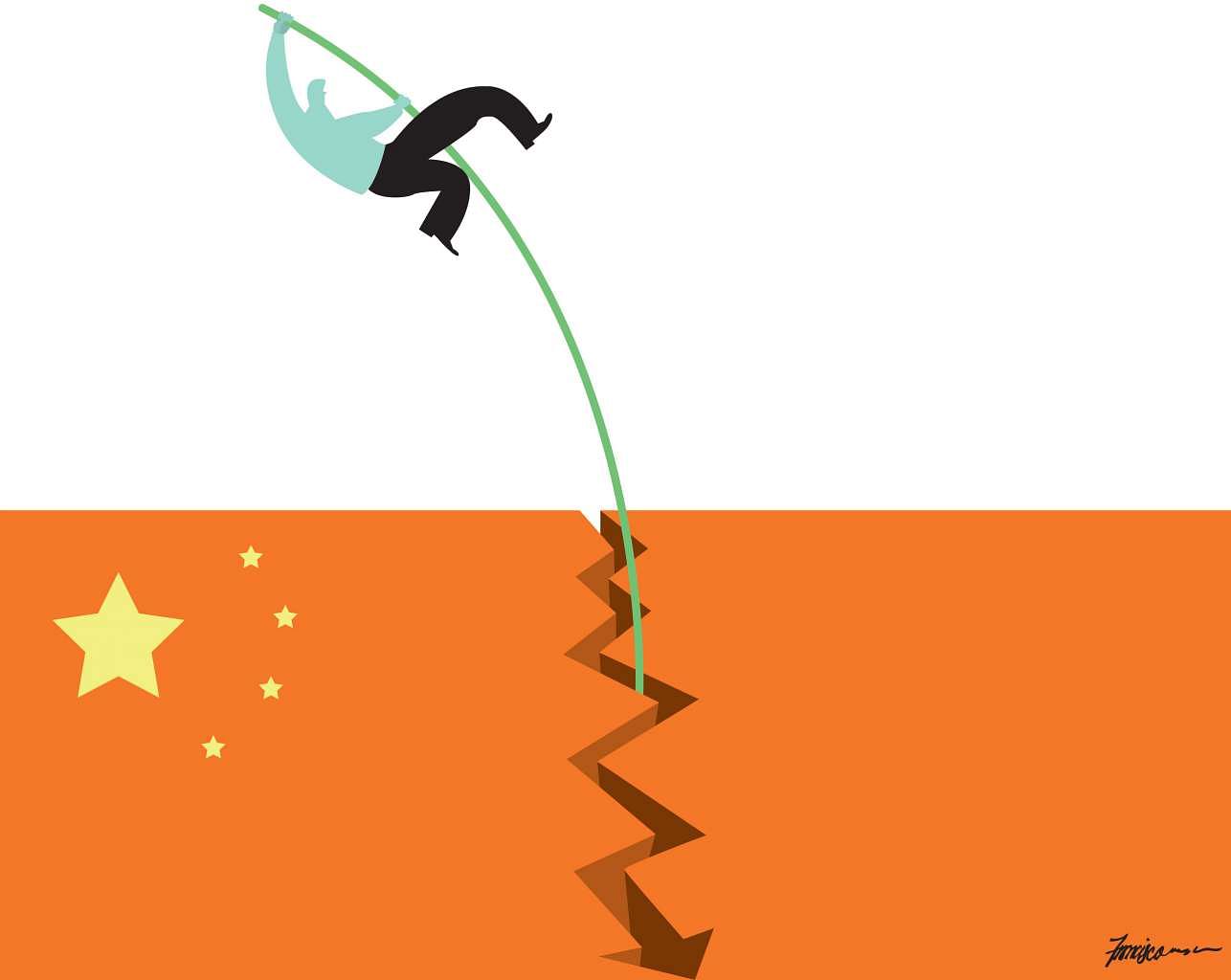

Earlier this month, the domestic Chinese equity market plunged 30 per cent from its June peak - erasing more than US$3 trillion (S$4.1 trillion) of notional wealth - after surging nearly 150 per cent over the preceding year.

The selldown has continued into this week, even after Chinese policymakers implemented unprecedented measures to stem the rout.

Market watchers are still debating whether this is a temporary correction or the beginning of a deeper malaise, and what impact it will have on the real economy.

Some analysts say the stock market rout is a belated symptom of China's economic woes. Decelerating growth in factory output, retail sales and domestic investment has been compounded by a slowing property market.

Officially, economic growth is expected to come in at 7 per cent this year, in line with the government's target, but many analysts say the official figures overestimate actual growth and it is in fact nearer 3 per cent.

Singapore is already feeling the impact of this, and it is becoming clear that the days of China growing at double-digit rates are over.

Given that China is the Republic's largest trading partner, what will this mean for Singapore in both the short and long term?

SLOWING GROWTH

Stock market gyrations aside, Singapore businesses with a presence in China have been feeling the effects of a slowdown for some time.

Mr Sam Chee Wah, general manager of precision engineering firm Feinmetall Singapore, said companies in his industry usually start to ramp up production for Christmas at this time of the year.

However, demand this year has been softer than usual, due in part to fewer orders from China, he said.

"The first month of the third quarter is usually very strong, but not this year... The orders are still coming in but they are slow and enough only to fulfil 'normal' consumption levels," Mr Sam added. "It might be because our customers are less optimistic about demand and are stocking up less... We're quite concerned."

Mr Joel Teo, head of law firm Lee & Lee's China practice, said Singapore companies with operations on the mainland are experiencing a slowdown in deal activity and expansion.

The downturn started when China embarked on property cooling measures a few years ago, since real estate drove a boom in the commodities market as well as other sectors such as services.

"Many companies are reassessing their exposure to China and pivoting their businesses towards defensive industries in the short run," Mr Teo said.

The business of financing China's trade is also shrinking, curbing what had been a fast-growing revenue stream for banks in Hong Kong and Singapore over the past decade.

Bloomberg reported that trade-related borrowings booked by banks in Hong Kong and Singapore fell in the three months through April to a two-year low of US$110.6 billion.

The figure rose to US$116 billion in May. Among the reasons for the fall in trade finance are China's slowing economy and lower commodity prices, analysts said.

ADJUSTING TO NEW NORMAL

Despite the short-term challenges, few predict Armageddon for the Chinese economy and, by extension, for Singapore.

When China's growth plunged from 9.5 per cent in 2011 to 7.7 per cent the following year, the rate of economic expansion here also nearly halved over the same period, from 6.2 per cent to 3.4 per cent.

However, such sharp adjustments are unlikely in the coming years even though Chinese growth continues to slow, said OCBC economist Selena Ling.

It is "not inconceivable" that China will be growing at a more sedate 6 per cent per year by 2020, but it will be a "slow grind" for Singapore and the region rather than a sharp decline.

"For Asean including Singapore, it would be an ongoing adjustment process as one of the major growth engines is slowing," she said.

Chinese policymakers have told the media that they remain sanguine about prospects for re-shaping the economy and transitioning to an era of slower expansion.

While annual growth is now relatively more sedate, the US$10 trillion economy is already several times larger and producing far more by virtue of scale, than when its pace of growth last slowed to 7 per cent or less. That was back in 1990, when China's growth dropped to 4.1 per cent due to international sanctions in the wake of the Tiananmen Square massacre. The economy bounced back quickly and logged growth of 9.5 per cent the following year.

The country also continues to offer rich opportunities for foreign investors in sectors such as consumer products and infrastructure development.

For instance, the "One Belt, One Road" initiative, proposed by Chinese President Xi Jinping in 2013, aims to spur development along a continental route and a maritime route that links 65 countries.

Experts and Singapore companies with a presence in China remain optimistic about the long-term prospects in the world's No. 2 economy.

With the recent massive stock selldown, many financial investors will pull out money from China in the shorter term but will return in the longer term, said Lee & Lee's Mr Teo.

"Most clients are still optimistic about the longer-term prospect of doing business in China," he added.

Mr Loy Suan Liang, chief financial officer of protective packaging manufacturer Fagerdala Group, said China's manufacturing sector "may be slowing but it is also transforming".

"The proliferation of automation and robotics in Chinese manufacturing will impact production wages, jobs and competition," he said.

In fact, while in the past Singapore largely focused on taking advantage of opportunities in China, the challenge is increasingly shifting towards being able to keep up with China, and interacting with it as a rising global power.

Singapore saw about 1.7 million tourist arrivals from China last year, about 24 per cent lower than in the year before. This was a small fraction of the 110 million outbound Chinese tourists.

Mr Edmund Chua, who runs tourism consultancy and training firm Singapore HuaDing, said the number of outbound Chinese tourists will continue to grow.

"The question is how Singapore will position itself to attract them... Chinese tourists are looking beyond Singapore, they're familiar with us but find us less exciting than other destinations like Korea or Japan."

He added: "We need to reinvent ourselves to stay relevant to China... What they wanted from us 10 years ago is different from what they want now."

China's economic transition has been striking and rapid and there remains little doubt that, in the long term, it will change the face of global economics and geopolitics.

For Singapore and the region, riding out the short- and medium-term changes of this tectonic shift will be challenging, but necessary.