How to ensure reliable income stream and preserve capital

Property executive Susan Tong's passion for real estate was ignited when she started to invest in the early 1990s after leaving a corporate sales job at Texas Instruments.

Her interest eventually led her to join the industry and become a property agent in 1999.

Ten years later, she set up her boutique property agency, ST Plus Properties, so it is no surprise that 70 per cent of her investments are in real estate, with the balance spread out among stocks, fixed income, unit trusts and fixed deposits.

She and her husband David Koh, both 57, plan to fund their retirement with passive income from their investment properties, Supplementary Retirement Scheme (SRS) money, Central Provident Fund (CPF) savings and dividends from their investments in stocks, bonds and unit trusts.

Ms Tong says: "We want to be financially free and be able to travel the world freely by age 62.

"By then, our youngest son would have graduated and the premiums for the kids' insurance plans would have been paid up."

She reckons that they would need at least $5,000 a month when they retire, but would rather aim for a higher monthly retirement stream of $10,000 so that they have enough set aside for holidays.

Mr Koh retired last year as managing director at an electronics firm and is now assisting her in the property business.

A year after buying their home - a two-storey corner terrace house with 3,100 sq ft of land in Yio Chu Kang - the Kohs used cash to fund their mortgage instalments instead of using their CPF savings, as the Ordinary Account offers a higher interest rate than the mortgage.

The house was bought for about $1.4 million in 2000 and is now valued at $3.5 million.

Besides, CPF members over 55 years old, such as the Kohs, get an additional 1 per cent interest on the first $30,000 of their CPF savings, making it 6 per cent interest a year. This is on top of the 1 per cent extra interest on the first $60,000 in CPF combined balances, which everyone enjoys.

This is one of the CPF enhancements that came into effect on Jan 1 to boost retirement savings.

While the Kohs make a conscious effort to save as much as possible, they do not hesitate to splurge on family holidays or their favourite cars or on fine dining to reward themselves. For instance, past family holidays to the United States, New Zealand, Australia and Britain have cost about $50,000 per trip.

The couple have three sons, Victor, 29; Lionel, who is married to Ms Han Hui Wing, both 28; and Edmund, 22.

The Kohs own a E200 Mercedes and a Toyota Altis, both paid up and both in their favourite colour, black.

FINANCIAL PROFILE

Ms Tong declined to give details of her total wealth, but said that she and her husband are prepared to set aside an investable amount - comprising cash and Ordinary Account - of $500,000. This is on top of an investment portfolio worth a six-digit sum comprising blue-chip stocks like DBS, OCBC, UOB, Keppel Corp and SGX; bonds such as Keppel Corp, Fraser Centrepoint, Perennial and Aspial; as well as unit trusts.

They are unsure how much they earn in dividends every year as they have never tabulated them.

The couple have an emergency fund of $200,000, which is in fixed deposits.

Their SRS amounts are $100,000 each and their Retirement Accounts have about $150,000 each, which translate to monthly payouts of about $1,100 per person when they reach 65.

They have no plans to top up their Retirement Accounts to the Enhanced Retirement Sum (ERS), which is $241,500 at present.

"We are not topping up to ERS because it's a one-way street. We're not comfortable with locking up (more of) our monies one-way, since you never know if you need money. We eat, breathe and sleep with property, so we prefer to park money in properties," says Ms Tong.

If they had topped up to ERS, their monthly payouts would be about $1,700.

They are also not going for the newly introduced CPF Life escalating payout plan as they have other sources of passive income and want to remain flexible.

The CPF Life escalating payouts are expected to increase at a rate of 2 per cent per year to cope with inflation. However, people opting for this plan will start with payouts that are about 20 per cent lower, compared with the current plans, unless they either top up their CPF Life premiums or delay the payout start age up to age 70.

Ms Tong declined to give details of her real estate portfolio but said that their investment properties are in Singapore. The rental income from these is more than sufficient to cover their mortgage. Their debt servicing ratio is 25 per cent.

The couple own a whole-life plan each with a combined sum assured of $1 million. About five years ago, they bought a limited-pay whole- life plan with a sum assured of $300,000 for each son, as a gift to them. The premiums would be paid up in five years.

All family members have hospitalisation cover and the couple have a critical illness cover of $250,000 each.

The annual cash premiums for their insurance policies amount to about $8,000 to $10,000 per child and $10,000 for the couple.

WHAT FINANCIAL EXPERT CHRISTOPHER TAN SAYS

CPF Advisory Panel member and Providend chief executive Christopher Tan said the Kohs have been prudent in setting aside $200,000 of emergency funds in cash and diversifying their investments to include investment properties as well as equities and bonds.

As such, their financial health is strong and they should be able to realise their retirement goals.

LOWERING INVESTMENT RISK

However, he noted that some of the bonds the Kohs hold are of higher risk.

He suggested that they consider restructuring their holdings to investment grade bonds if they want a more reliable income stream while preserving capital. This is because Mr Koh is already semi-retired and both are near retirement, so preservation is key.

Mr Tan said: "Doing so may cause them to receive lower coupons and, as a result, a lower reliable income stream. To compensate for that, they can top up their CPF Retirement Account to ERS to receive higher monthly CPF Life payouts."

Although the Kohs have indicated that they would prefer not to do that, he said this is an option to consider so they can lower the risk of their investment portfolio in retirement.

In addition, given that the Kohs are close to retirement, they can lower their investment risk by further diversifying their portfolio of shares with other asset classes such as bonds.

Mr Tan warned: "The management fees of unit trusts can be high and, as a result, eat into the returns. This is especially crucial in an environment where returns might be lower in the future. As such, they might want to restructure their unit trusts and shares to diversified and lower-cost funds."

As the Kohs are "accredited investors", Mr Tan says they can invest in funds from Dimensional Fund Advisors as well as Vanguard, which Providend uses for such clients.

These funds are not only of lower cost (average management fees of 0.3 per cent per annum), but they are also widely diversified and have a reputable track record due to their low-cost investing approach.

Accredited investors are those with net personal assets exceeding $2 million or whose income was not less than $300,000 in the preceding 12 months.

MEETING RETIREMENT OBJECTIVE

Based on a 3 per cent inflation rate, Mr Tan worked out that they would need a nest egg of about $1.9 million to achieve their retirement goal of $10,000 per month in future dollars ($11,593) at age 62 for the next 25 years.

While the Kohs have their eyes on a monthly retirement sum of $10,000, their "safe" retirement floor is $5,000 per month or $5,796 in future dollars.

Mr Tan says a retiree's risk profile is not measured in the same way as that of an individual who is still in the accumulation phase of his life to grow his wealth.

"A retiree's risk profile is measured based on his desired safe retirement income floor. As the Kohs desire an average 50 per cent safe retirement income floor ($5,000 out of $10,000 per month), their risk profile is moderate."

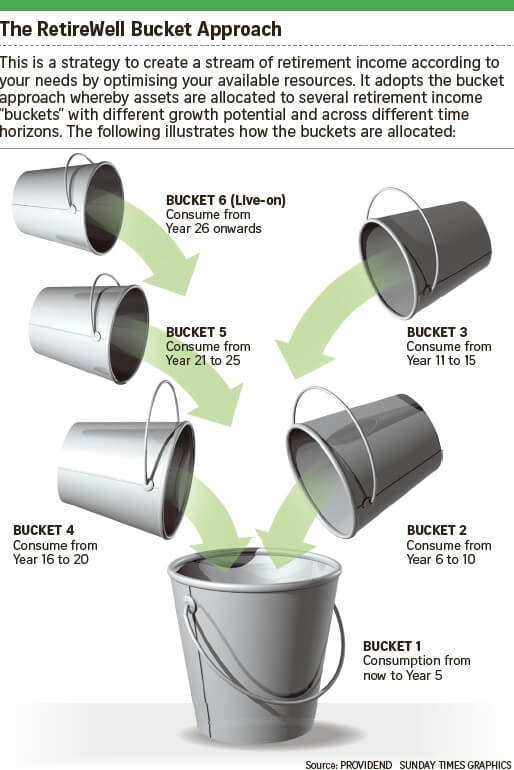

With this in mind, Mr Tan used his firm's Proprietary RetireWell System to optimise the resources that the couple have, so as to meet their retirement objective.

The RetireWell model efficiently allocates the Kohs' assets into six buckets when they are 62 years old. It works on the following grounds:

•Have a portion of your nest egg pay a reliable income stream for life that is almost risk-free;

•Money needed over the immediate five years in retirement should not be invested;

•Money not needed over the immediate five years is invested progressively from low to higher risks, with the holding period for each one increasing with higher levels of risk.

So, at retirement age 62, the Kohs place their accumulated nest egg in several retirement income segments or "buckets", each with a different growth potential due to varying asset allocations and time horizons. Each bucket is meant to provide income over progressive five-year periods.

In the case of the Kohs, the income bucket pays a reliable income stream - consisting of bond coupons, CPF Life payouts and rental income - for life. This is the reliable income stream portion.

The first bucket holds cash and near-cash assets that can be used for immediate income needs.

The remaining four buckets are invested in portfolios of different asset allocation with different risk-return characteristics over different time periods.

As each bucket nears the end of its investment horizon, the proceeds are transferred to bucket one (cash or near cash assets) for withdrawal.

The model showed that the Kohs can achieve a "safe" retirement income floor of at least $5,796 and total retirement income of $11,593 per month - both figures are adjusted for inflation - as well as leave behind a legacy of bond investments and properties and hedge against longevity risk.

At the end of the 25 years, they would still have their bond investments and properties, assuming they are left untouched. If the couple live on, they will continue to receive income from these assets as well as the CPF payouts to live on. When they die, they will leave behind their bond investments as well as their properties as legacy.

•The CPF Board is holding a CPF Retirement Planning Roadshow at Suntec City today from 11am to 6pm. It will outline the role of retirement planning and how the CPF helps establish a foundation for your golden years. There will be games with celebrity guests, an immersive 360° virtual reality experience and fun activities. The next roadshow will be at Toa Payoh HDB Hub on Sept 17 and 18. For more information, go to cpf.gov.sg/bigRchat.