(BLOOMBERG) - Hong Kong property companies, whose shares have been beaten down amid this year's protests, are missing an opportunity to unlock value for shareholders. More should consider packaging their trophy assets into real estate investment trusts to release capital and improve the market's view of their prospects.

The Hang Seng Properties Index has slumped more than 17 per cent from an April high as the unrest disrupted business, deterred home buyers and caused tourists and shoppers to stay away. The broader Hang Seng Index has lost 11 per cent. Many real estate companies are trading at a steep discount to the value of their underlying assets.

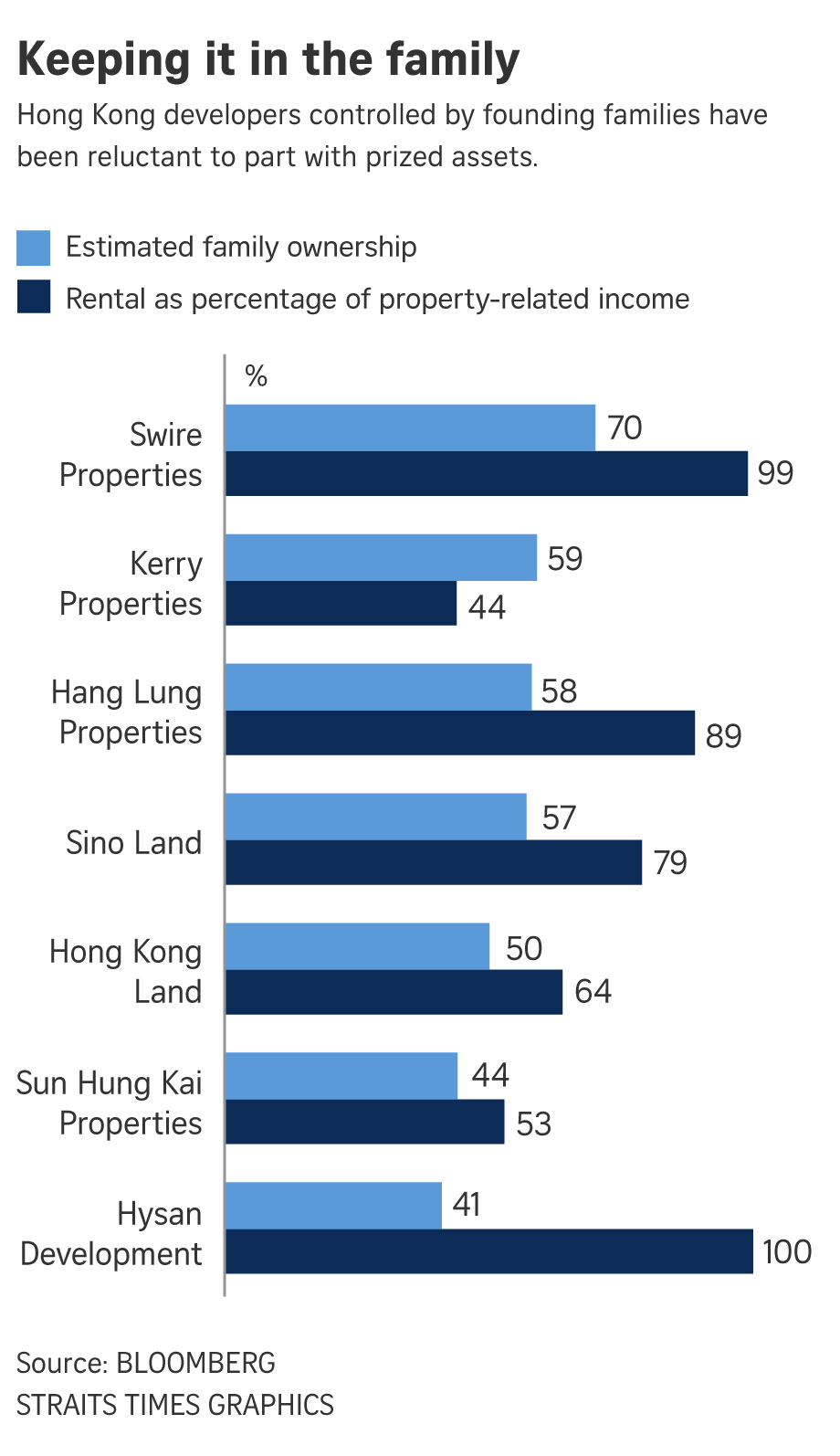

To understand why developers are trading at a discount, look at the ownership structure. Many are controlled by founding families, who are reluctant to part with their most prized properties. Take Hang Lung Properties, for example. Chairman Ronnie Chan owns more than half the company, which trades at a price-to-book ratio of 0.52 times.

As a result of the reluctance to divest, companies end up acting essentially as landlords rather than developers, stunting the potential for growth. In effect, investors are participating in a bond-like structure by collecting rental income instead of achieving an equity-like return via property development and sales.

Concern that Hong Kong is at the peak of a property cycle has also helped to depress valuations, with investors discounting developer shares to reflect the risk of a decline. Hang Lung's price-to-book ratio has dropped from a peak of more than 1.8 times over the past decade as Hong Kong real estate prices surged.

Spinning off rental properties into trusts, or Reits, could help to narrow the discount to net asset value. Such a manoeuvre would enable family-owned entities to retain control while generating capital from Reit offerings that could be redeployed into better-yielding projects. That in turn would raise return on equity, benefiting owners and investors. The parent company would enjoy higher growth prospects through a relatively asset light model while the Reit provides a steady income stream.

Income taxes are the primary obstacle to the expansion of Hong Kong's Reit market. At the moment, Hong Kong property trusts are taxed like corporations at 16.5 per cent. Singapore, by contrast, grants a tax exemption to Reits holding both domestic and foreign properties as long as they pay out 90 per cent of their income in dividends. In 2014, Hong Kong's Financial Services Development Council urged the city's authorities to stimulate the Reit market by introducing a tax break, so far to no avail.

That discrepancy has helped Singapore to maintain its lead over Hong Kong as a centre for Reits. Singapore, which issued its first property trust in 2002, has 43 now with total assets of US$112 billion (S$153 billion). Hong Kong's first listing was Link Reit in 2015. Nine more have followed since, bringing total assets to US$67 billion. No new Reits have been issued in Hong Kong since 2013; by contrast, Singapore has seen 11 listings in the past five years.

Share performance has also been superior in the South-east Asian city-state. The S&P Singapore Reit index has returned 25 per cent this year, compared with less than 4 per cent for its Hong Kong equivalent. The valuation gap is stark: Singapore Reits trade at about 1.1 times book, versus 0.6 times for Hong Kong.

Ronald W Chan is the founder and chief investment officer of investment management firm Chartwell Capital in Hong Kong.