At the height of the global financial crisis in March 2009, global lender HSBC famously faced down the short-sellers who had sent its share price plummeting 24 per cent in a single day by sticking to its plan to launch an attractively priced rights issue to raise US$17.7 billion.

The move forced investors who had loaned their HSBC shares to short-sellers to recall them in order to subscribe to the rights issue or face a big dilution in their shareholdings.

It was a move which was repeated by Olam International four years later in 2013, when it launched a US$750 million bond-cum- warrants issue to defend itself from the assault launched by United States short-seller Muddy Waters, which had accused it of running a fiendishly complicated business with too much debt.

Now, it would appear that sub-sea contractor Ezra Holdings has also managed to steady its ship by adopting the same strategy.

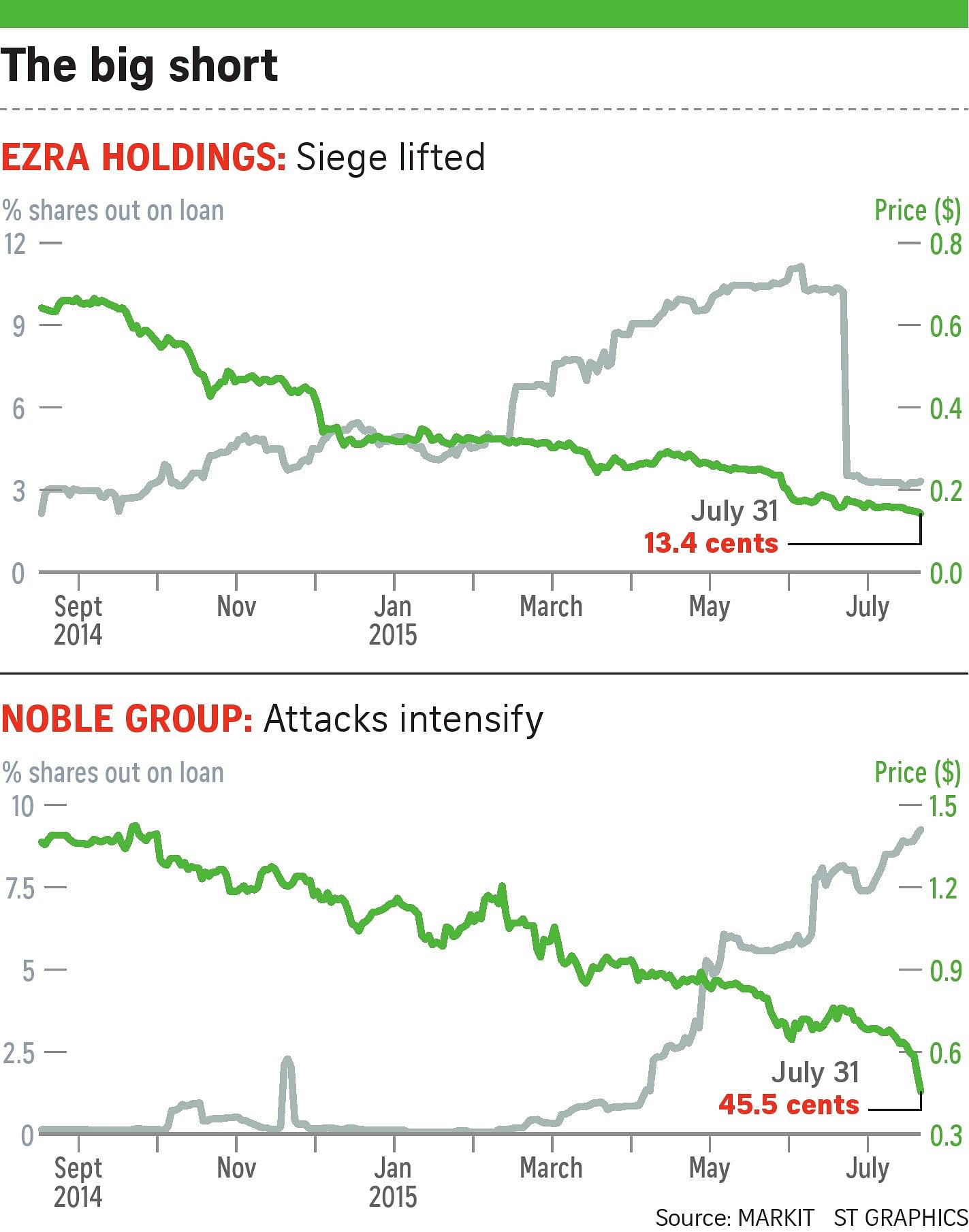

Data from information provider Markit showed that Ezra achieved the dubious distinction of being the most "shorted" counter on the Singapore Exchange (SGX) last month as the percentage of its shares out on loan - presumably to short-sellers - quadrupled to almost 12 per cent from 2.9 per cent a year earlier.

Worse, its stock price plummeted by another 32 per cent after it announced a cash call at the end of May to raise up to US$300 million (S$411.5 million) as the September deadline to repay a $225 million bond issue and a $150 million perpetual bond approached.

But like HSBC, Ezra did not flinch and pressed ahead with its cash call, backed by the decision of its founder, Mr Lee Kian Soo, and his son, Lionel, who is the company's chief executive, to take up their rights entitlements in full.

The company won hands down as short-sellers gave up besieging the stock, reckoning that its shareholders would give the company their full support and subscribe to the rights issue.

The outcome was an astonishing drop in the percentage of shares out on loan by two-thirds to just 3.5 per cent on June 26, the day when its share register closed for the rights issue.

For Ezra's long-suffering investors, however, victory carried a bitter price, given the 71.6 per cent plunge in stock price in the preceding 12 months.

Now, will the same strategy work for the beleaguered Noble Group, which has replaced Ezra as the most "shorted" counter on the SGX?

Since February, when the veracity of its accounts was challenged by an unknown blogger called Iceberg Research, whom the company claimed is a disgruntled former employee it had sacked, Noble's share price had plunged by 62 per cent, wiping out $4.9 billion of its market value.

At the centre of the fierce battle between Noble and Iceberg, now joined by Muddy Waters and former investment banker Michael Dee, is how the company reported its long-term commodity deals.

As a trading firm, Noble holds a huge number of contracts signed with commodity suppliers and customers. This means that a sizeable chunk of the profit

which it records may come from estimating the gains or losses made on these contracts using an accounting procedure known as "mark to market".

But it was the sheer size of the fair value gains - US$4.6 billion - which caused uneasiness since far bigger trading firms, such as Glencore, reported much smaller fair value gains of US$80 million.

To assuage these concerns, Noble said that it had hired giant accounting firm PwC to review its "(mark to market) models, valuations and governance framework" and that it would publish a summary of the work.

In the past six weeks, the company has spent a mind-boggling $131 million buying back its own shares to try to fend off the short-sellers attacking it.

But the ploy appears to have emboldened short-sellers into stepping up their ferocious attacks. The Markit data showed that when Noble started its share buyback on June 11, about 5.77 per cent of its shares were out on loan, presumably to short-sellers.

But the massive share buybacks might have given short-sellers an even bigger incentive to short the counter, given the temporary boost they gave to its share price.

Between June 11 - when the buyback commenced - and July 29, the number of shorted Noble shares rose sharply as the proportion of shares out on loan increased by three-fifths from 5.77 per cent to 9.24 per cent of the company's outstanding shares.

Worse, the attacks appeared to have accelerated as Noble entered a two-week blackout period before its second-quarter results on Aug 13, when the company and its senior management were barred from making further share purchases.

Last Thursday, the SGX slapped Noble with a "trade with caution" warning as its share price plummeted a further 11.9 per cent to a seven-year low of 52 cents on a heavy volume of 138.4 million shares traded.

For the week, the stock was down 18 cents, or 28.3 per cent, to 45.5 cents.

Given the massive selling pressure, it would seem that the company has to do a lot more to restore investor confidence than just a PwC review of its accounting practices.

Of course, following in the footsteps of Ezra and recapitalising its balance sheet with a rights issue will be a strong confidence booster, especially after ratings agency Standard & Poor's cut its rating outlook for the company from "stable" to "negative".

But some market pundits argue that what is right for Ezra may not work for Noble.

Ezra's problem is quite straightforward as it is caused by a big downturn in the offshore industry, which raises questions over the huge debts it ran up during the boom years. So getting money from its shareholders to boost its capital base had a calming effect.

But in Noble's case, one question to ask is whether its rank-and-file 30,000-odd shareholders will stand solidly behind the company if it ever has to resort to a cash call, given the fears triggered by the huge plunge in its share price.

Iceberg suggested that Noble should look for a white knight with deep pockets to come to its rescue. Even though it has been the cause of much of the company's grief, its advice should not be brushed off or taken lightly.