Of late, global financial markets have been unusually calm - in fact, too calm for some of us.

That stock prices should stay in top form at this time in the market cycle is an amazing feat, coming as it does a full eight years into an ageing bull market.

At a similar point in the market cycle 20 years ago, we were already starting to experience stomach-churning wild swings in our market as the Thai baht plunged against the greenback and precipitated a financial crisis which engulfed much of Asia.

Another stark example: The global financial crisis erupted at around this time 10 years ago when the gyrations on Wall Street sent shock waves across financial markets worldwide, as tottering US banks struggled to cope with the toxic sub-prime mortgages that poisoned their balance sheets.

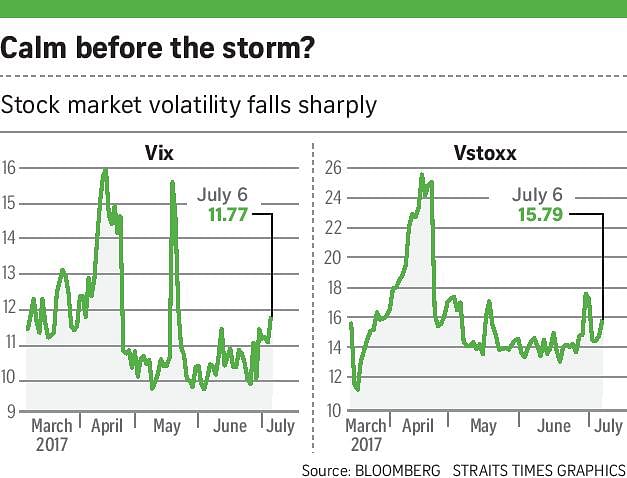

In the United States, the Vix, which tracks the volatility of stocks in the widely watched S&P 500 Index, has halved to 11 points - or just above its lowest level on record - since the election of Mr Donald Trump as President last November.

That trend has run counter to the conventional market wisdom that Mr Trump's controversial policies ranging from trade to immigration would trigger turmoil in the stock market.

In the same eight months, the Vstoxx index, which provides a similar measure of volatility for the Euro Stox 50 Index that tracks euro zone blue chips, has tumbled about 40 per cent to near record lows.

Even the notoriously volatile China stock market, dominated by millions of retail investors whose trading decisions are strongly influenced by rumours and speculation, is enjoying an uncharacteristic period of stability. The last time the Shanghai Shenzhen CSI 300 Index has moved more than 2 per cent in one day was in December last year.

Here, in Singapore, the same phenomenon can be seen. The benchmark Straits Times Index hasn't moved by more than 2 per cent in a single session since March last year.

This is despite a spate of fear factors that were supposed to rock investor confidence, such as the renewed weakness in oil prices and the escalating tensions over North Korea's missile programme.

On the flip side, however, one reason for the uncharacteristic calm is the brightening economic outlook globally and this may have caused investors to shrug off the political worries.

In a bullish report on global markets, Mr Robert Buckland, chief global equity strategist at Citi Research, noted major economies and big companies are making a "synchronous recovery" - the first time such a simultaneous recovery has unfolded across the globe in years.

Citi analysts are anticipating global GDP growth of 3.1 per cent for this year and 3.3 per cent for next year. This makes Mr Buckland confident that while the eight-year-old global bull market is looking aged, it is by no means finished.

Another reason for the calm could be the huge amount of liquidity sloshing about in the banking system as major central banks continue to flood their economies with cash to try and boost tepid growth.

In the case of the US, local brokerage UOB Kay Hian noted that since the global financial crisis 10 years ago, the US central bank's balance sheet has swelled fivefold to US$4.5 trillion (S$6.2 trillion), or about 25 per cent of the country's GDP.

And even though the Federal Reserve has flagged its intention to shrink its balance sheet, the likelihood is that the sea of liquidity is unlikely to dry up completely, with the brokerage noting that former Fed chief Ben Bernanke had estimated the US central bank may still hold as much as US$4 trillion on its balance sheet - representing a shrinkage of only 11 per cent from its highest level.

That is not including the enormous amount of liquidity the European Central Bank is still pouring into the financial system as it maintains its monthly asset purchases of €50 billion (S$79 billion) until December this year.

Even the moribund Tokyo stock market is enjoying an extended rally, boosted by purchases from the Bank of Japan which has a goal of buying as much as six trillion yen (S$73 billion) a year of exchange-traded funds tracking Japanese stocks.

To complete the loop, the Chinese have hopped onto the bandwagon as the world spotlight falls on China with the 20th anniversary of Hong Kong's transfer back to Chinese rule and the upcoming leadership reshuffle in Beijing.

Some have credited purchases by the so-called "national team" - a group of Chinese state-owned companies instructed by Beijing to support share prices - with underpinning China share prices.

Still, the current beguiling market calm has raised plenty of concerns. A low volatility reading is usually seen as a sign of investor complacency.

The great investor John Templeton once observed that bull markets are born on pessimism, grow on scepticism, mature on optimism and die on euphoria.

If the low stock market volatility is any guide, the phase in which investors displayed any form of pessimistic or sceptical behaviour is long over, as they pour copious sums into stocks.

Optimism is certainly the most apt description of current behaviour, as these investors are clearly anticipating further upside in their stock purchases. Of euphoria, there are few signs as yet, even though the giddy run-up in the tech-heavy Nasdaq Index would have reminded some of the dot.com bubble at the end of the last millennium.

But even though those betting on a "black swan" event derailing the current rally are finding their wagers blowing up in their faces, it behoves investors to tread with care in the market.

As one strategist noted, those who bought when stock market volatility was high in 2011, 2012 and January last year all went on to enjoy decent returns, while those who bought during low volatility in May 2013, July 2014 or June 2015 all subsequently suffered losses.

The Asian financial crisis has also taught investors a rude lesson about the capricious manner in which "hot" money can be suddenly sucked out of a market, leaving highly indebted companies with a nasty hangover and, in some cases, fighting for their very survival.

Since that crisis, when the currencies of Malaysia, Thailand, Indonesia and South Korea went into free fall, South-east Asian nations have built up war chests of foreign reserves to ward off speculative attacks.

These steps enabled their economies to dodge the bullets fired by the global financial crisis 10 years later, even though their stock markets suffered a knee-jerk meltdown as Wall Street crashed.

Asian markets received another grim reminder four years ago as the US Fed hinted that it was scaling back its massive monetary stimulus programme.

The resulting "taper tantrum" caused a stampede out of then hot markets such as India and Indonesia.

No doubt, the global economy and corporate profits are rebounding, and there is nary a storm cloud on the horizon to dampen investor enthusiasm. But just before the onslaught of the financial storms in 1997 and 2007, didn't we experience a similar beguiling calm?

The market may be much too quiet for its own good.