After years of blistering growth, emerging markets (EM) sunk into a disappointing rut following the global financial crisis. Stock markets in these economies were pummelled by weak commodity prices, sluggish export growth and political disruptions.

Since mid-2011, the MSCI Emerging Markets Index, a representation of mid and large caps across 23 emerging markets, has returned minus 11 per cent, a far cry from the 49 per cent upswing of developed markets.

But as the world reels from the shocking Brexit vote, the zeal for emerging market equities has been rekindled. The MSCI Emerging Markets Index has rallied 10 per cent since June 27, outperforming developed markets by 3.1 per cent.

We are now overweight in emerging market equities within our global tactical asset allocation strategy for the first time since April 2013. Our confidence in the emergence of this bloc as a source of equity performance is based on several global forces shifting in its favour. We also see attractive risk-reward in emerging market US dollar-denominated high-yield corporate and sovereign bonds.

SOURCES OF GROWTH ARE STEADYING

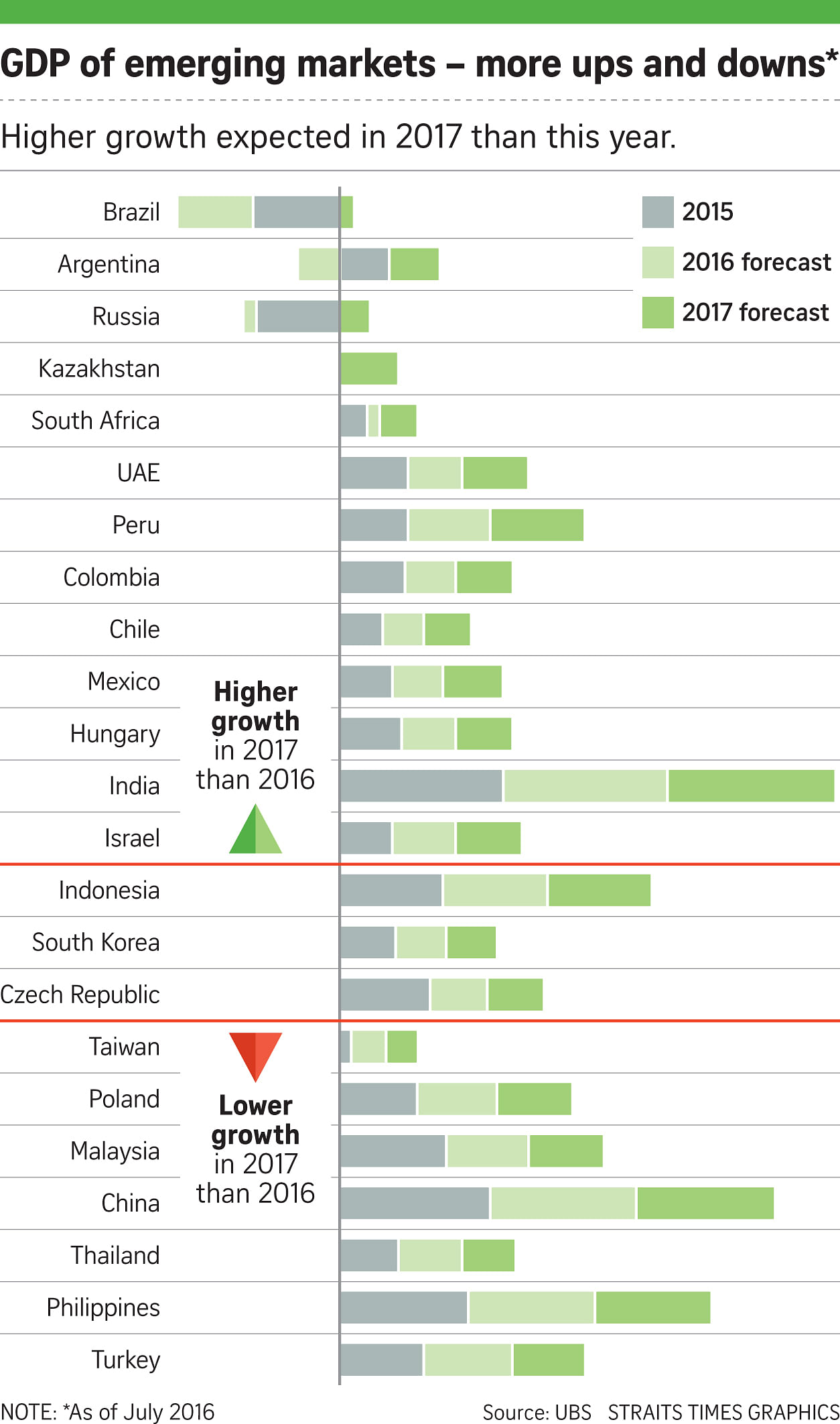

Emerging markets have been hit hard by China's economic slowdown. Their fortunes soared as China's insatiable hunger gobbled up their resources and goods at favourable prices. With a US$11 trillion (S$14.74 trillion) gross domestic product (GDP), China is roughly equal in size to the next 10 largest emerging markets combined. So as the whirl of the world's growth engine began to slow, so did the prospects of many emerging markets.

But China's 6.7 per cent GDP expansion in the second quarter suggests that government stimulus is stabilising activity. Rising consumer spending is partly offsetting ongoing weakness in the "old economy" industrial sector.

And most importantly, nascent signs of corporate earnings stabilisation have emerged: MSCI China companies are forecast to deliver flat to 2 per cent year-on-year earnings growth for 2016, and earnings upgrades are likely as we head into the first-half earnings season.

As mentioned, the commodity cycle is key to the emerging market investment case. While raw material prices are neither too hot nor too cold, a 20 per cent rise in the Bloomberg Commodity Spot Index since the January lows has removed a headwind to economic growth and profits in commodity-exporting emerging markets, especially in Latin America. But prices have not climbed so high as to impair the outlook for global inflation or the Asian commodity importers.

Last year, emerging market economies grew just 3 percentage points faster than developed nations, down from 6 percentage points in 2009. This growth advantage is likely to expand again in the coming years, particularly as the economies of Brazil and Russia stabilise after deep recessions. Purchasing managers' indices have improved, with Asian and emerging European gauges back above the 50 level that separates expansion from contraction.

STABILISING EARNINGS, DOVISH FED PROMPT UPSIDE POTENTIAL

Earnings per share of emerging markets have started to stabilise. That has helped drive the recent emerging market stocks rally. While valuations are now close to the average for the past decade, there is room for further price appreciation if profits improve as we expect.

Meanwhile, the US Federal Reserve is likely to keep rates lower for longer due to the uncertainty created by the UK referendum vote. A more dovish Fed stance than at the turn of the year has boosted emerging market currencies, up 3 per cent against the US dollar since then. Stronger emerging market currencies contribute to lower inflation rates, reducing the need for growth-suppressing interest rate rises. This should keep the cost of funding low for businesses and support EM equities going forward.

The same factors are also supportive of having a diversified portfolio of select emerging market bonds. Despite the rally, the yield pick-up offered by US dollar-denominated high-yield sovereign and corporate bonds provides an attractive reward for adding them to an emerging market portfolio. Moreover, we expect default rates to decline slightly in the next six to 12 months and the downward pressure on credit ratings to ease, in line with an improving business cycle.

POSITIVE ON INDIA, CHINA AND BRAZIL EQUITY MARKETS

Within EM equities, we are overweight in India, China and Brazil, and underweight in Mexico, Taiwan, the Philippines and Malaysia. Many investors in the region are familiar with China's attractive valuations and the long-term potential of its new economy sectors, and India's compelling growth story where we expect profit growth in the solid mid-teens over the next 12 months. But what about Brazil?

With a price tag of well over US$10 billion, investors shouldn't count on the Rio Olympics to boost economic activity in Brazil in the coming months, although, there is potential for a moderate long-term increase in tourism flows to Rio. What we expect is improvement in economic activity and consumer confidence in the second half due to a vast improvement in government policy settings since Acting President Michel Temer took office in May. Lower interest and inflation rates should also reduce the cost of equity and allow earnings to bottom out.

We are neutral on Singaporean equities within the region. As Singapore continues to restructure its economy, the nation's economic growth will enter a new, lower norm. We expect GDP growth to moderate from the past 10 years' average of 5.2 per cent to low single digits over the next few years. But opportunities remain for yield stocks in select real estate investment trusts and telecommunications sectors in an environment of low-interest rates.

Still, there are risks to monitor. A lasting rally will require the stabilisation of earnings to turn into a full rebound. And the failed coup in Turkey is a reminder that political risks can stoke market volatility. But on balance, the outlook for emerging markets is bright and better placed to remain in the black.

•The writer is the Apac regional head at the chief investment office of UBS Wealth Management.