Local banks face a challenging year, but their robust capital reserves will stand them in good stead, analysts say. Those challenges range from vulnerable credit quality to slow loans growth, which will combine to put pressure on earnings as they did last year.

DBS Group Holdings, OCBC Bank and United Overseas Bank (UOB) all recorded lower profits in the first nine months last year after having to fork out massive allowances to cover potentially bad loans.

DEBT ISSUES LOOM

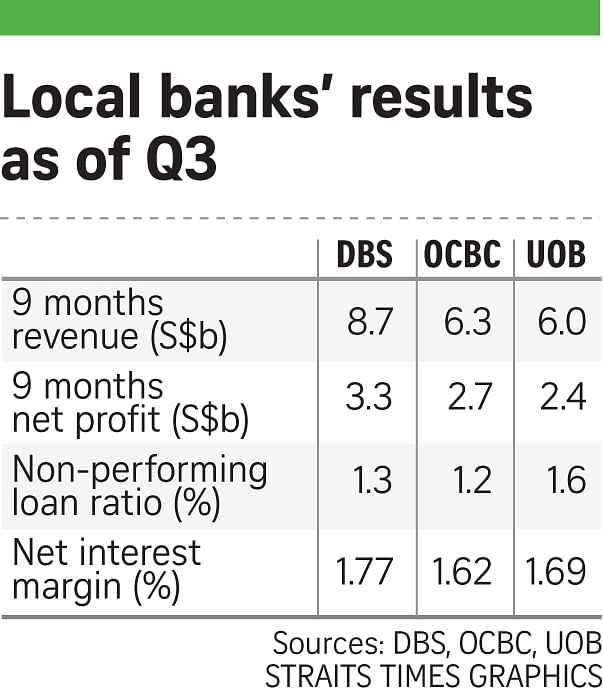

DBS' net profit for the period was down 4 per cent year on year to $3.3 billion, after accounting for a one-off gain in 2015. But it did not help that allowances jumped 96 per cent to $972 million, due partly to Swiber Holdings' implosion.

OCBC's nine-month net profit was down 9 per cent to $2.7 billion, with allowances surging 43 per cent to $421 million.

Earnings at UOB were down 2.6 per cent to $2.4 billion in the same period, with specific allowances for loans rising by $265 million. These were mainly from non-performing accounts in the oil and gas and shipping industries, it said last October.

The bank bosses told third-quarter briefings that their oil and gas portfolios have probably seen the worst.

"I think we've seen the bulk of the pain. There will be some more but it's not dramatic," DBS chief executive Piyush Gupta said. OCBC chief executive Samuel Tsien said that the problem may persist but will not spread.

Moody's backed these cautiously optimistic notions. The ratings agency had earlier moved to downgrade Singapore banks' baseline credit assessment ratings, but said further downgrades are unlikely in the next 12 to 18 months, as new problem loans will not pile up at the pace seen last year.

PAIN INCREASING

Nomura analyst Marcus Chua warned recently that there may be more pain to come in terms of asset quality, not just due to the still-struggling oil and gas sector but also the broader economic slowdown in the region.

"We expect this asset deterioration cycle to last longer than in the global financial crisis, as this time round, issues are more structural than cyclical," Mr Chua said.

Gross domestic product growth for Asia excluding Japan has been stuck at around 6 per cent for the past five years, held back by stagnant exports and ageing demographics. "Therefore, on top of the oil and gas sector, we are as concerned about the broader economy going into 2017," Mr Chua said, adding that manufacturing and general commerce may be the next problem sectors for the local banks.

INTEREST RATE UNCERTAINTY

There is also no consensus yet on what rising interest rates ahead actually mean for the banks.

The United States Federal Reserve plans to hike rates several times a year until 2019, with local rates expected to follow in tandem.

This will help improve banks' net interest margins - the difference between interest income from loans and the interest a bank pays depositors, but Maybank Kim Eng research associate Ng Li Hiang sees a limit to the upside.

"We think some of these benefits will likely be partly offset by competitive pressures in loan pricing, especially for large corporate and consumer loans," she said.

"We are negative on banks as we think the overall outlook will remain challenging. We expect loan growth to remain lacklustre from weak loan demand and also, banks are now careful in their lending and unwilling to take on higher risks."

Nomura's Mr Chua said the swap offer rate, one of the local interest rate benchmarks, is tied closely to the US dollar. That could weaken and erode local banks' net interest income if US President Donald Trump adopts a weaker greenback policy, he added.

GROWTH ENGINE INTACT

Despite the numerous risks, Singapore banks are still robust, pan-regional institutions with strong business-line synergies and various opportunities for growth. One of the more bullish areas is wealth management, which has been thriving at the three banks in recent times.

It now provides nearly one-third of fee and commission income for DBS and OCBC, DBS Vickers analyst Lim Sue Lin said.

"The strong growth registered across the banks has been attributed to their consumer franchise network, relationships with SME owners, as well as bancassurance products," Ms Lim said.

DBS agreed last October to acquire ANZ's wealth management and retail banking in five regional markets. At OCBC, its acquisition of Barclays' wealth and investment management business in Singapore and Hong Kong was completed last November.

"As more and more foreign banks look to sell their businesses in Asia, it is likely that acquisitions and the hunt for new assets (under management) and customer networks will continue," said Ms Lim.

The three banks will announce their fourth-quarter results in the coming weeks.