After a talk on saving and planning for a child's education that I gave at the National Library last month, as part of the askST series, several parents came up to me to ask how they should invest for their kids.

Some wanted to know if they should put money in insurance products or buy unit trusts. Others asked about investing with a fund manager.

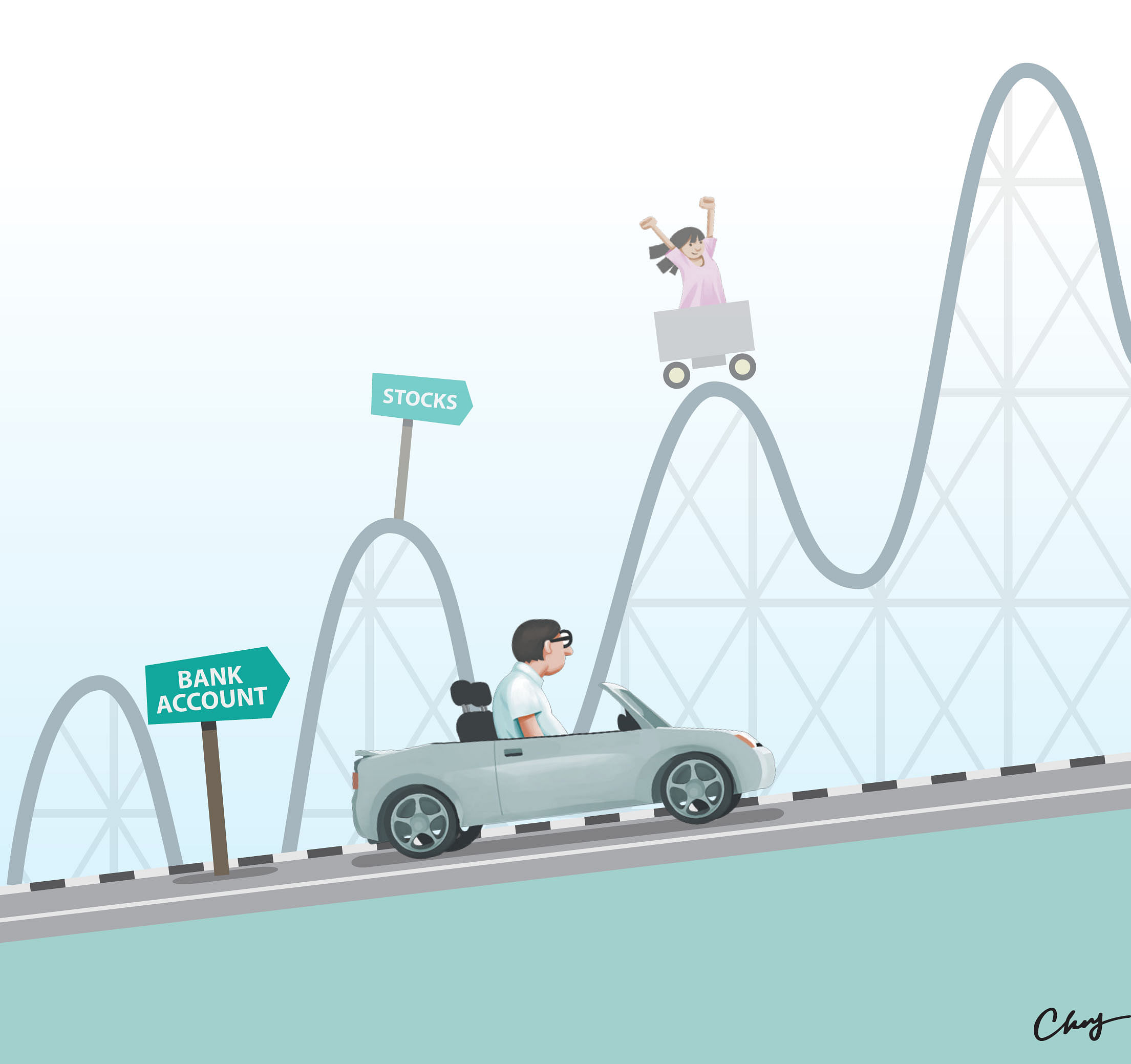

These suggestions are decent ones, and much better than simply leaving the money in a bank account earning next to nothing.

But for those who want a more direct approach to investing, one way of doing this more efficiently is to simply do it yourself.

Many Singaporeans I have met baulk at the idea, saying that the stock market is a scary place, like a casino. Several also say they have neither the experience nor the time to invest.

The solution? Use a disciplined approach to invest for a long term. I call this the No-Fuss strategy.

There are three elements to it: a commitment to investing for the long term, the discipline to set aside some money every month, and some knowledge of a product called Exchange-Traded Funds (ETFs).

The first thing about investing - not trading - that people need to come to terms with is that it is a long-term commitment. By this, I mean a time horizon of at least 10 years.

This means having to watch your stocks fall, which is not easy to stomach. Since the stock market is volatile, do expect to see your portfolio dip into the red. But take comfort in the historical fact that most stock markets end up higher over the long term.

Secondly, you need to consistently set aside money every month. It does not have to be big and the amount can be as little as $100 but the money has to be set aside consistently.

Over 10 years, the total sum invested, based on $100 a month, is about $12,000 - not a lot by any means.

Third, invest in ETFs, low-cost products that passively track an index of stocks.

An ETF has many benefits. One is that most of them are liquid, meaning you can sell them off in the market in a pinch if you need funds.

Another is that they offer diversification as most ETFs track many different companies at once. This mitigates your risk levels.

The STI ETF, for instance, tracks the Straits Times Index, the benchmark index for the local bourse and comprises the biggest blue-chip companies here.

ETFs also pay dividends, which is a major plus. STI ETFs have paid out between 2 per cent and 3 per cent every year since 2009.

The strategy? Every month you set aside a fixed amount, say $100, and invest in the STI ETF. Then watch your portfolio grow.

All the major stock brokers here offer monthly investment plans that allow investors to invest as little as $100 a month into stocks, which include the STI ETF.

This approach is also known as the dollar-cost averaging approach, a strategy first made popular in the 1980s.

To be fair, it has limitations.

A seminal paper in 1979 published by Washington University finance professor George Constantinides focused on the theoretical basis of dollar-cost averaging. It argued that the strategy was a sub-optimal one when it came to measuring risk.

A more recent empirical paper by mutual fund giant Vanguard in 2012 showed that an investor might be better off investing a lump sum, rather than spreading the funds out over fixed time periods.

It ran simulations of the dollar-cost averaging approach in three markets - the United States, Britain and Australia, investing $1 million in their respective currencies.

Taking a 60 per cent equity and 40 per cent bond portfolio, the money was invested in rolling bands of 10 years each, starting from as far back as the 1920s.

The result was clear: If you took the money and invested all of it at the start of each 10-year period, you would be better off than spreading it out in equal tranches over a fixed period of time.

The dollar-cost averaging approach involved spreading the funds with an interval of 12 months over a 10-year period. This resulted in an average ending portfolio value of US$2,395,824 in the US stock market simulation.

The lump sum approach beat this by 2.3 per cent with an average value of US$2,450,264.

In fact, the study showed that, across markets, the lump sum approach beat dollar-cost averaging approximately 67 per cent of the time.

The study, however, did go on to qualify that the simulation was to test whether dollar-cost averaging was superior to lump sum investing, in the case of having a big sum to invest at once.

The study was also useful in showing one simple fact: Investing in the stock market pays.

Sure, dollar-cost averaging may have yielded less than the lump sum approach by 2.3 per cent on average, but hey, it still grew US$1 million to about US$2.4 million over 10 years.

I did a similar test for the Singapore stock market using the Straits Times Index. If you had invested $1 million in June 2006, your returns would have grown to $1.48 million by June 2016. This includes a yearly dividend of about 2.3 per cent.

For dollar-cost averaging, using the same metrics, the final sum comes up to about $1.29 million.

Not bad for a decade which saw one of the worst market crashes in history.

So whether it's putting all of it at one go, or slowly trickling the money in, the answer to investing wisely for the future is this: Stay the course for the long term.

Since the stock market is volatile, do expect to see your portfolio dip into the red. But take comfort in the historical fact that most stock markets end up higher over the long term.