NEW DELHI (NYTIMES) - Nirav Modi brightened Kate Winslet's earlobes and made Taraji P. Henson's collarbone glitter.

A jeweller to the stars, Modi attained wealth and fame at home in India in a few short years. He socialised with British royalty and rubbed elbows with Donald Trump Jr. He opened an opulent outlet on Madison Avenue in New York.

In January, he met with Mr Narendra Modi, India's Prime Minister and no relation, at the annual gathering of the world's elite in Davos, Switzerland.

Today, he is on the run.

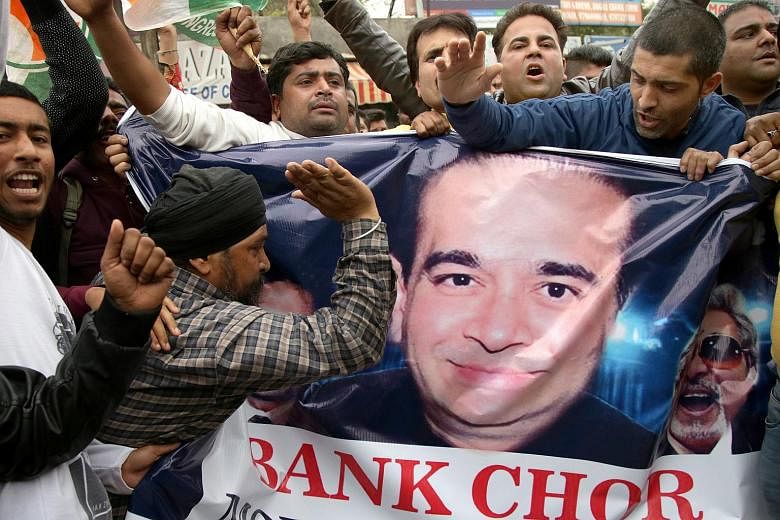

About a week after Modi grinned for the cameras with the Prime Minister, a state-run Indian bank told regulators that it had found nearly US$1.8 billion (S$2.36 billion) in fraudulent transactions linked to the jeweller's account.

Indian officials now accuse Modi, his family and business associates of assembling a global empire with nearly US$3 billion in money obtained illegally, mostly from government-run banks. He denies wrongdoing.

The chase has enraged and captivated India at a time when the public increasingly believes the country's debt-laden government banks are enriching its flashiest, most corrupt business tycoons.

Parliament sessions have deteriorated into screaming matches, with political opponents exchanging accusations of collusion with the jeweller.

Finding Modi has become something of a national pastime. Reporters in New York camped outside a luxury hotel, the JW Marriott Essex House, where they believed Modi was staying.

One who rang the bell outside what they believed to be his room found only a servant and a fluffy white dog.

For many Indians, the allegations against Modi further cement the notion that taxpayer-owned banks are footing the bill for the lavish lifestyles of a rising elite. That idea has particular resonance in a country where stark poverty - India is home to a third of the world's poorest people - remains dire.

Before Modi, India watched as Vijay Mallya, an airlines-and-liquor magnate known as the King of Good Times, fled to Britain as banks tried to collect US$1.4 billion. Many of the banks left on the hook were state-owned. He has denied wrongdoing.

The state-owned Bank of Baroda has drawn news media attention over its business with the three Gupta brothers, who left India in 1993 and built a sprawling corporate empire in South Africa. They have been caught up in a political scandal there that led to the resignation of South Africa's president, Jacob Zuma.

Bank of Baroda denied wrongdoing in a written response to questions, asserting that it acted in good faith and that many of the transactions it handled for the Gupta brothers were received from other banks.

In February, the Indian authorities arrested Vikram Kothari, a ballpoint pen magnate, saying he had diverted loans given to his company by seven government-owned lenders. He also denied wrongdoing.

The allegations against Modi have only strengthened people's wariness of the state banks. Indian officials have publicly accused him of working with tellers at a single branch of one of them, Punjab National Bank, to obtain US$1.8 billion from branches of other banks.

So far, five Indian banks have been swindled in the scandal, four of them government-owned, the authorities in New Delhi say.

Just a decade ago, during the global financial crisis, Indian lenders were held up as a bastion of stability. Today, they are considered more vulnerable than those in other leading emerging markets, mostly because state-controlled lenders dominate the sector, according to the International Monetary Fund.

Of the US$6.5 billion in fraudulent loans that have hit the industry over the past two years, the most egregious cases were at government-owned banks, according to figures released by Parliament.

Executives at those lenders are more likely to be appointed for their political connections than for their talent, financial analysts say.

"For every Nirav Modi in this country, there's 10 more, and they are emboldened when they see the government failing to take action or pursue the right protocols," said Mr Vineet Dhanda, a lawyer who is urging the Indian government to tighten up the banking sector.

Mr Dhanda questioned how major business figures like Modi could raise billions from banks without providing collateral, yet the average farmer struggles to get a few hundred dollars for a loan.

"The money they are stealing is from the poor people of this country," he said. "If this money is swindled away, then it comes from the taxpayers to fix the banks."

Modi's lawyer, Mr Vijay Aggarwal, denies his client defrauded banks and says there is only a misunderstanding over a much smaller loan worth about US$40 million.

He accused the banks and government authorities of damaging his client's reputation and the Nirav Modi brand's value, making it harder for the company to settle its debts.

"This was a case of civil transaction which the authorities have converted into a criminal one unnecessarily," Mr Aggarwal said in an interview.

Diamond traders and jewellers have long marvelled at Modi's rise. Nicknamed NiMo in the press, from the first syllables of his name, Modi was known for wearing custom-made cuff links with the fish from Finding Nemo.

Born in Antwerp, Belgium, to a relatively small diamond trading family, Modi attended the prestigious Wharton School of Business before dropping out at 19 to join the family business in Mumbai.

He first rose to international prominence in 2010, when he designed a necklace featuring a 12.29-carat diamond set with smaller pink diamonds. It was auctioned by Christie's in Hong Kong for US$3.56 million, nearly US$1 million more than its asking price.

The bidding war landed Modi on the cover of the Christie's catalogue, the first Indian to be featured so prominently by the auction house.

He formed his Nirav Modi brand later that year and announced plans to open 100 stores around the world by 2025.

In 2015, Modi opened his flagship store on Madison Avenue, a few blocks from the luxury giants Cartier, Saks and Dior.

Donald Trump Jr was there, taking a break from his father's presidential campaign, as were actors and models: Naomi Watts and Coco Rocha posed for photos on the red carpet in front of the Nirav Modi logo.

The next year, Modi designed 100 carats' worth of diamonds that Winslet wore to the Oscars.

His rapid ascent puzzled some in the diamond industry, who say building a luxury brand takes both time and money.

"Using models and actresses that are world-renowned to consumers - that makes a brand seem solid," said Mr Karma El Khalil, a jeweller based in New York. "But it's incredibly expensive."

His lifestyle rose with his fame, according to interviews with colleagues and friends and local news reports that tracked his purchases.

He bought a Rolls-Royce for family use. He had an aquarium built that covered an entire wall of his office. He bought an apartment in an exclusive, seaside high-rise called Sea Palace that is home to some of Mumbai's wealthiest people, including one of the founders of the information technology giant Infosys.

But the authorities in New Delhi say he projected an image of success built on bank loans and fraudulent letters of understanding, part of a strategy to expand his business in the hope that profits would eventually outstrip debts.

"The arms of the law are long," said Mr Abhishek Dayal, a spokesman for the Central Bureau of Investigation, the main government body investigating the case. "We will get them."

Modi's flight has shaken diamond traders in Antwerp and Mumbai.

Until the allegations surfaced, he seemed to fit well in an international industry that often works based on trust and personal relationships.

For example, a trader will often mail a diamond to another and give the other person a window of up to four months to evaluate the gem before expecting payment.

Modi quickly won a reputation as someone who could be trusted, say diamond traders. He often paid within days after receiving diamonds.

Now diamond traders are wondering whether the industry trusted him too quickly, and what the fallout on the international diamond trade will be.

A diamond dealer in Antwerp said he and his colleagues became anxious last month when the Indian government banned its banks from issuing letters of credit to finance trade abroad, making it harder for Indian diamond traders - some of the biggest players in the industry - to buy stones.

"Your reputation is based on today," said Mr Sabyasachi Roy, the executive director of India's Gem and Jewellery Export Promotion Council, sponsored by the Ministry of Commerce.

"Today you're great until you're not. Today you have actresses wearing your designs; tomorrow, no one will look at you. But everyone was surprised by his quick rise."