From Nov 1, every Singaporean and permanent resident will be covered by MediShield Life.

The scheme will insure everyone, including the old and the sick, and provide lower co-payment of bills and unlimited lifetime claims.

Some people may still be unclear about how MediShield Life might affect them.

Senior Health Correspondent Salma Khalik answers questions posed by readers.

Q Why is the coverage from the time you are born? Does that mean my kids will be covered now though they have not paid any premiums?

A Yes, your children will be covered from Nov 1.

All Singaporeans born from Aug 26, 2012, are given a $3,000 grant by the Government which is put into their Medisave accounts. This money can be used to pay their MediShield Life premiums.

If your children were born before that date and have no Medisave, you, as their parent, are responsible for paying their premiums till they are 21 years old.

Q Can I pay my MediShield Life premiums with cash to conserve the money in my Medisave?

A As long as you have enough money in your Medisave account, it will be used to pay your MediShield Life premiums. You can, however, top up your Medisave Accounts via voluntary contribution with cash, subject to the relevant limit - which is $48,500 now, but will be $49,800 on Jan 1 next year. This amount will increase every year.

Q I paid my private Integrated Plan (IP) premium in July. If I drop my IP in November, will I get a proportional refund for the IP premium I have paid? Or do I need to wait till my next renewal date to make the change?

A No, you do not need to wait till your IP is due for renewal to switch to the basic MediShield Life. You can switch once the scheme starts on Nov 1.

And, yes, you should get a proportional refund for the unused portion of your IP premium.

Below are questions answered in the Aug 5 column

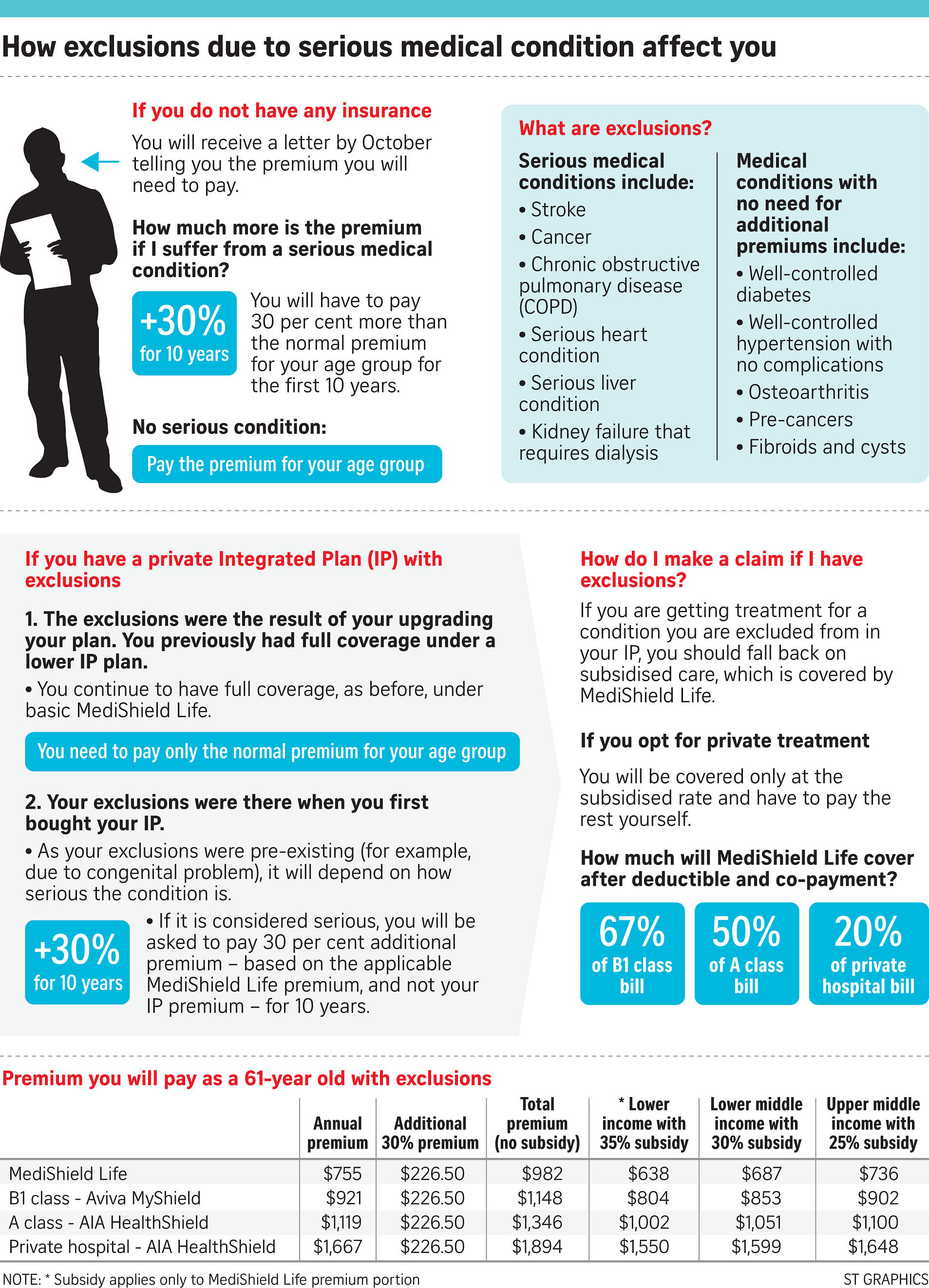

People who are uninsured, and those who are insured with exclusions, will receive letters telling them if they need to pay higher premiums to enjoy full coverage when MediShield Life starts on Nov 1. The additional premium is 30 per cent more for 10 years. This has led to some confusion, especially among people with private integrated plans (IPs).

Q I upgraded to a private hospital plan about five years ago. Because of the upgrade, I was excluded from coverage related to heart problems. Does that mean I now have to pay 30 per cent higher premiums for 10 years? Will that cover me for my heart condition in private hospitals?

A There are three parts to your question.

- Would you need to pay the additional 30 per cent premium? If you had been covered by MediShield (or an IP which incorporates MediShield) before your upgrade and exclusion, you would already be fully covered and do not need to pay the additional premium.

- If you had exclusions from the day you joined, whether you will need to pay the additional 30 per cent premium will depend on how serious your condition is. If it is considered serious you will need to pay the additional premium, and you will enjoy full coverage for subsidised care.

- The 30 per cent additional premium is based on your MediShield premium, and not your IP premium. It will therefore cover you only at public hospital subsidised rates - and not at private hospital rates.

Q I have a private Integrated Plan with exclusions. With MediShield Life, I will be covered for everything. If I am excluded for heart problems by my IP and am hospitalised in a private hospital for a fracture, but suffer from a heart attack while in hospital, will that be covered by the IP or by MediShield Life? How will the bill be divided?

A It is up to your IP insurer to assess whether treatment for your heart problem while in hospital for a fracture is claimable based on its policy conditions.

MediShield Life payout will be made regardless of whether the IP component will pay the claim.

But the amount covered by MediShield Life, after factoring in the deductible and your co-insurance, will be based on charges in a public hospital subsidised ward.

Q I am paying my mother's MediShield premium with my Medisave. With the Government's top-up for pioneers, how do I change the payer so that my mother pays her own premium?

A As your mother has the basic MediShield, she can request to change the payer online at www.cpf.gov.sg.

She needs to log in with her SingPass, go to "My Requests" on the left panel and select "Healthcare Matters", then select "Change payer of MediShield cover to myself".

If she has a private IP, her insurance agent can make the change for her.

Q I wish to cancel my IP and switch to just the MediShield Life plan. What should I do?

A The best thing to do is to wait till MediShield Life is launched on Nov 1. You will then only need to cancel your IP to be covered only by the basic MediShield Life insurance.

Q My father has been certified with Total Permanent Disability.

Will he still have to pay the MediShield Life premiums? He is in a nursing home. Will he be entitled to subsidies?

A Yes, your father will have to pay MediShield Life premiums, which will be based on the address in his identity card.

Though he is a nursing home resident, he may still require hospital care for infections or other illnesses. With MediShield Life, he will receive lifelong protection for large hospital bills.

If he is unable to pay the premiums even after all the subsidies and government top-ups, there is an Additional Premium Support to help needy Singaporean families on a case-by-case basis.

Below are questions answered in the July 16 column

With the launch of MediShield Life on November 1, 2015, many readers have asked for help to understand the complex issues involved. Below are some of the questions I was asked this week. E-mail me at salma@sph. com.sg with the header "Ask Salma" if you have more questions.

Q: If a patient has only MediShield Life but chooses a B1 or A ward in a public hospital, will MediShield Life pay the basic B2 cost while the patient pays the difference? If yes, what is the quantum or percentage that the patient has to pay?

A: Yes, MediShield Life will pay the subsidised rate for that treatment, no matter which ward the patient goes to. The amount the patient has to pay will vary according to the ward class.

As a guide, the Life Insurance Association of Singapore estimates that the basic insurance would cover the following portions of the bill:

•B1 class: 67 per cent

•A class: 50 per cent

•Private hospital: 20 per cent

Q: Do we need to be hospitalised to claim from MediShield Life? Does it cover day surgery such as for cataract?

A: No, MediShield Life will cover some outpatient treatments, such as cancer treatments, and all day surgery operations. The deductible - the amount you need to pay each year before insurance kicks in - for subsidised day surgery is $1,500, the same as for C class.

Q: There are many innovative cancer therapies that can be very expensive. Does MediShield Life cover them?

A: Many new cancer treatments are still experimental or have yet to be proven and accepted as first-line treatment, and so are not offered by all institutions or oncologists.

As long as the treatment is offered under public hospital subsidised care, MediShield Life will cover it.

Q: I wish to cancel my Integrated Plan (IP) and switch to MediShield Life. How do I do it?

A: It's best to wait till MediShield Life is launched later this year. You can then simply cancel your IP, as you will be covered automatically by MediShield Life.

Q: How does MediShield Life and IPs work for people covered by the Civil Service scheme?

A: Those who are on the Medisave cum Subsidised Outpatient (MSO) scheme have been receiving an additional 2 per cent of their salary, capped at $140 a month, since January this year, to help them pay for MediShield Life premiums.

The 15 per cent of civil servants and 40 per cent of pensioners on the Comprehensive Co-payment scheme will receive an additional

1 per cent in their Medisave account when MediShield Life starts.

As 60 per cent of pensioners now enjoy better benefits than provided by MediShield Life, there will be no change for them, and the Government will pay premiums for them.

Q: MediShield Life has an annual limit of $100,000. What type of diseases treated at B2 and C class will bust this limit? Could you give examples of large subsidised bill sizes?

A: People who have bust the current $70,000 MediShield annual limit usually did so because they needed several expensive treatments in that year. It is unlikely that one single bill in B2 or C class would bust the limit.

You can check the following website for an idea of actual bill sizes for different treatments in various ward classes: