There was more red ink for global markets yesterday as fears over China's slowing economy sent investors into a state of near panic.

Shares were dumped in a frenzied sell-off from New York to Sydney that also extended to commodities and currencies.

Wall Street set the tone overnight with shares down 2.06 per cent - the biggest daily percentage drop since February last year.

Worse was to come when the gauge that measures China's manufacturing activities was released yesterday morning.

It showed a flash reading of 47.1 for August - close to a 61/2-year low, while the final reading for July was 47.8, also below the 50-point line dividing expansion and contraction.

Chinese investors, already on edge after last week's shock yuan devaluation, rushed for the exit.

The Shanghai Composite lost 4.27 per cent, capping a miserable week that left it down 11.5 per cent. Shenzhen pared 5.39 per cent, Hong Kong fell 1.53 per cent and Australian stocks retreated 1.4 per cent.

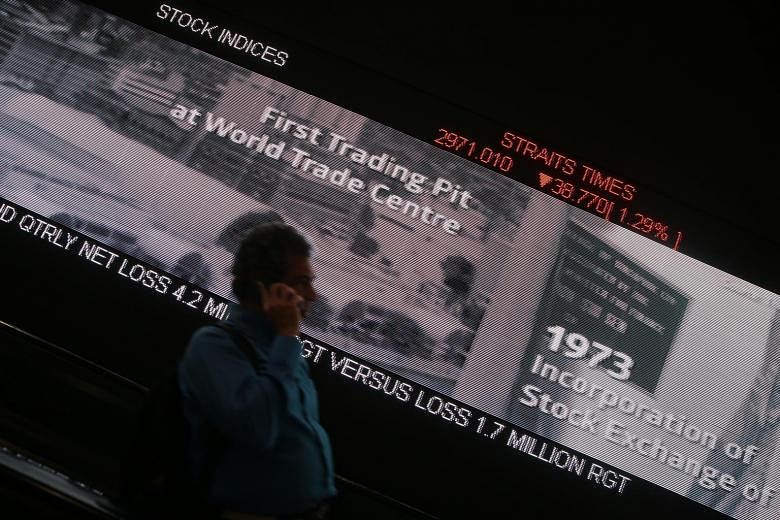

Singapore's benchmark Straits Times Index fared a little better, losing 1.29 per cent to close at 2,971.01 - another new low since February last year and down 4.6 per cent for the week.

Regional currencies took a hit too. The Singapore dollar weakened against the US dollar, alongside the still-tumbling Malaysia ringgit.

The greenback was trading at 1.4075 against the Singdollar late yesterday afternoon, up 0.24 per cent from Thursday.

It also rose against the ringgit, rising 0.78 per cent to 4.1593.

Concerns around China threatened demand for crude oil as well. Benchmark Brent futures went down 1.1 per cent to its lowest settlement since January, at US$46.62 a barrel.

Bank of Singapore chief economist Richard Jerram said: "To some extent, this sudden concern is puzzling as China has been struggling all year.

"However, perception can create its own reality and the flows out of emerging markets are sending currencies weaker and driving broader concern over systemic risk."

SEE BUSINESS