Greek banks are shut down and the people of Greece can withdraw only €60 (S$90) at ATM machines. The referendum on Sunday will decide whether Greece should say "yes" or "no" to bailout conditions imposed by the troika of the European Union, the European Central Bank and the International Monetary Fund.

What will be the consequences of the vote for Greece, Europe and the global economy? Will there be a geopolitical impact? How did Greece get into this quagmire? What lessons can we learn from the Greek tragedy?

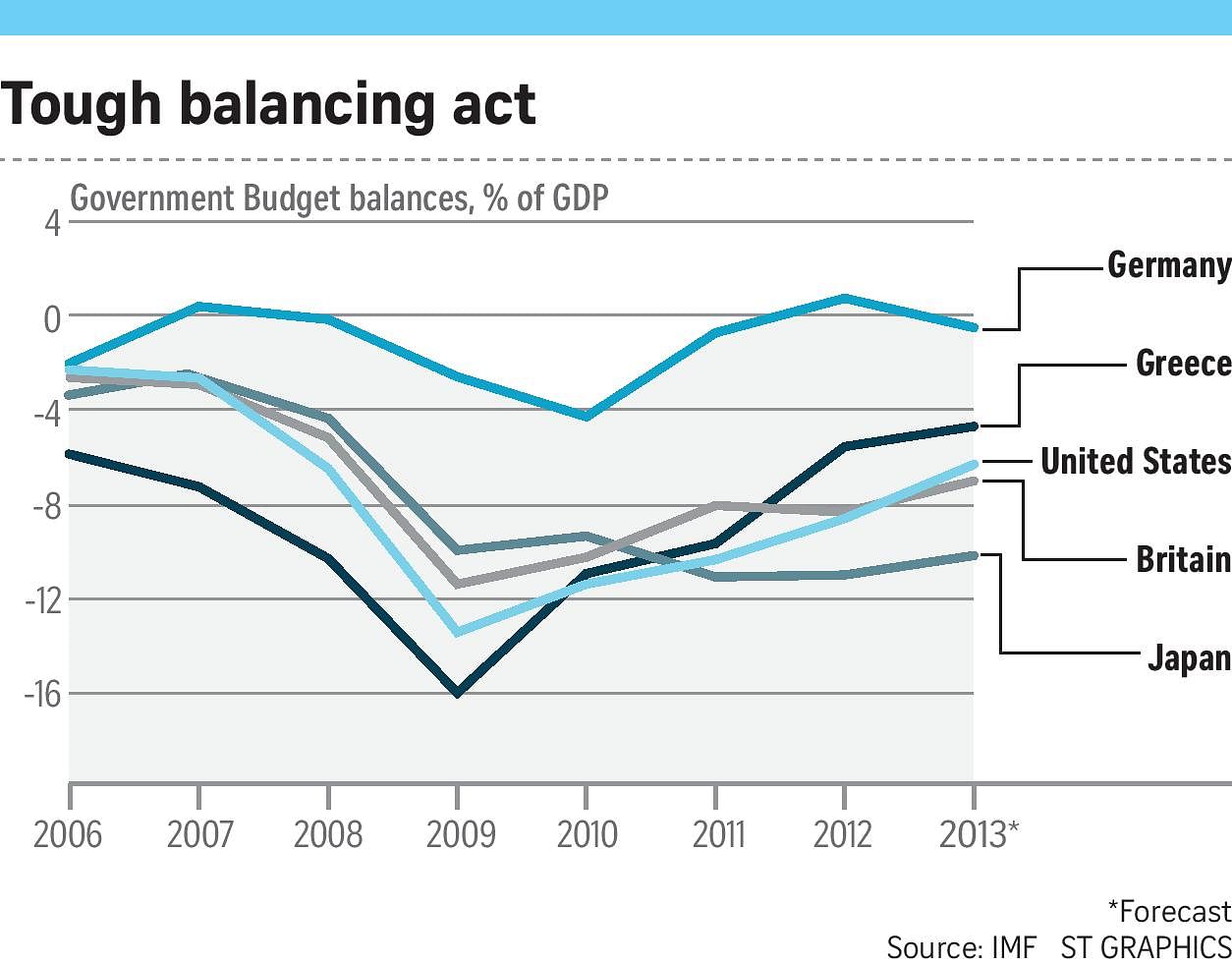

GENESIS OF CRISIS

Greece has been in a Great Depression since 2009, with gross domestic product falling 25 per cent and unemployment at 28 per cent. Youth unemployment is easily double the national average. The Depression is comparable to what the United States experienced in the 1930s.

In October 2009 when the Greek economic/financial crisis began, the Greek government had a budget deficit of 15.7 per cent of gross domestic product (greatly exceeding the 3 per cent allowed in the EU Stability and Growth Pact) and a debt-GDP ratio of nearly 130 per cent (more than twice allowed).

Externally, the current account deficit (foreign borrowing) had been rising to nearly 9 per cent of GDP, resulting in a cumulative debt of more than 70 per cent of GDP.

What were the root causes?

Firstly, entry into the euro zone was achieved at too favourable an exchange rate, causing Greece, which was already lagging behind in productivity, to become uncompetitive.

Secondly, Greece's higher wage increases and higher inflation, combined with low productivity, worsened its competitiveness: Greece's unit labour cost rose to nearly 30 percentage points higher than Germany's.

Thirdly, after joining the euro zone, Greece's borrowing costs fell substantially from nearly 25 per cent in 1991 to below 6 per cent. This must have encouraged a borrowing binge by the public and private sectors.

Fourthly, the financial crisis of 2007-2008 resulted in a sudden stoppage/reversal of external financing. Those who had borrowed at short term were the most vulnerable because of the maturity - and, in some cases, currency - mismatches.

Bad governance was also an issue.

Finances were fudged: To enter the euro zone, Greece lied about its public finances. Its deficits were well in excess of the Maastricht norm of 3 per cent of GDP and its public debt well above the limit of 60 per cent of GDP.

Profligacy: Successive governments promised more and more largesse in order to win votes. The result was ballooning Budget deficits that had to be financed by borrowing because Greece cannot print euros.

Bloated bureaucracy: After democracy was restored in 1974, successive populist governments padded the civil service. By 1980, over 500,000 were civil servants. Until recently, the number exceeded one million (out of a work force of over four million). Most of these employees cannot be fired. Generous perks, benefits, bonuses and pensions were the lure for government jobs.

Poor tax collection: Revenues lost to tax evasion are estimated to be 3 per cent to 4 per cent of GDP, enough to reduce the government deficit by half.

Ineffective governance and corruption: According to World Bank indices, Greece's indices for effectiveness of governance and corruption had fallen way below the rest of the EU/euro zone.

THE SCYLLA OF AUSTERITY

Despite the massive bailout funds extended by the troika and substantial haircuts on bond redemptions, Greece is in the throes of a Great Depression with high unemployment, heavy retrenchments, severe cuts in government expenditure, especially on pensions and entitlements, and an exploding debt-GDP ratio of 175 per cent.

The problem is Greece has to find the euros to pay its creditors but it cannot find enough. It needs more bailout and debt restructuring but the troika insists on onerous conditions which spell more austerity and painful reforms.

Greece is in the hapless death spiral described by the noted economist Irving Fisher in his article "The debt-deflation theory of Great Depressions", where austerity results in exploding debt-GDP ratios. The current government was elected by a disenchanted electorate who do not like austerity. Being a member of the euro zone means Greece has no control over the exchange rate and monetary policy, both of which are set by the ECB. It has to live with a euro too strong for its weak competitiveness. Staying with the euro means that the only way forward is to cut wages and prices - what economists call internal devaluation. In addition, of course, it has to produce a primary surplus in the Budget to pay its creditors. This entails further painful cuts in government expenditure and increases in taxes. Greek standards of living must fall further.

Without further bailout and haircuts, a Greek default was always likely. Already, its banks are in danger of collapsing as depositors withdraw funds massively. Politically, the Greek government is in a conundrum: It cannot give in to the troika's demands because it was voted in by an anti-austerity electorate. Hence the resort to Sunday's referendum.

THE CHARYBDIS OF GREXIT

What about leaving the euro zone or being expelled from it? This would mean reverting to its own currency, the drachma. Massive debt defaults are likely unless Greece can find another godfather, perhaps Russia. The immediate prospect would be a massive devaluation of at least 70 per cent. This would mean high inflation and masses of people pushed into poverty. The legal and financial repercussions are nightmarish to contemplate: Commercial contracts are denominated in euros and foreign liabilities are in euros. Drachmas would have to be printed in huge quantities, resulting in massive devaluation and inflation.

Recall the mayhem of the Asian currency crisis when tens of millions of people fell into poverty, businesses were bankrupted and banks fell like nine pins. Recall also the 2002 Argentinian devaluation when the peso was devalued from 1 peso to US$1 to nearly 4 pesos to US$1. Half the population fell below the poverty line as a result.

Greece's per capita income has already fallen from about 66 per cent to about 50 per cent of Germany's. It is certainly in danger of becoming a Third World country. Hence, whether Greece remains in or exits from the euro zone, what is certain is the further drastic lowering of living standards. Only massive bailouts and drastic reforms can alleviate the situation.

Outstanding Greek bonds held by foreign banks and institutions amount to €323 billion.

The direct impact would come from a Greek default. The troika will bear the brunt of any default to the extent of €246 billion. On Tuesday, Greece failed to make payment of US$1.7 billion (S$2.3 billion) to the IMF. Weaker banks might fail. More important could be the cascading effects, depending on the interconnectedness of financial institutions. Psychologically, asset markets are already retreating.

The economy of Greece is only about 2 per cent of the euro zone. Hence, the direct effect on exports of euro zone countries to Greece would not be serious. Nevertheless, the psychological impact of Grexit is yet unknown.

A big question mark hangs over euro zone countries such as Spain, Portugal, Cyprus and Ireland that are barely recovering from their own crises: Speculators are likely to look for chinks in their armour.

The euro zone itself would have to speed up the building of banking and fiscal union and pursue reforms to strengthen the group.

Commentators have noted that Russia may have an interest in a Grexit, which may be helpful to stave off painful EU sanctions. Certainly, a Grexit will drive Greece politically towards the Russian embrace, with consequences for the siting of Russian naval and other bases in Greece. It remains to be seen whether and how much Russia is willing and able to pay for a Greek ally. The possible consequences for Nato and Eastern Europe are already resulting in an arms race and the US is putting more military hardware close to Russian borders.

•The writer is practice professor of economics at Singapore Management University.