Changes to rules governing Central Provident Fund (CPF) withdrawals can be political dynamite. They usually involve requiring workers to lock up more savings in the mandatory pensions scheme, and for longer, as life spans and costs of living go up.

Just over 30 years ago, when a straight-talking Cabinet minister by the name of Howe Yoon Chong set out the rationale for raising the CPF withdrawal age from 55 to 60, it provoked such anger and took such a toll on the People's Action Party (PAP) at the 1984 polls that his report was shelved.

Instead, three years later, in 1987, the Government introduced the CPF Minimum Sum scheme.

That helped to cushion the blow, but the aim was the same - to increase the sum that CPF members have to set aside in their retirement accounts before any lump sum withdrawal is allowed.

Such changes are good policy at the national level, but rankle at the personal level.

They arouse the greatest resentment perhaps among older, lower-income workers who may not have much spare cash and look forward to the day when they can take out a lump sum from their CPF, to realise long-held dreams or ambitions. That explains the crowds - a large proportion of them men in their 50s - who showed up at the Speakers' Corner last year to protest against hikes in the CPF Minimum Sum.

Now comes a controversial call for a policy change in the opposite direction. Yesterday, a government-appointed CPF Advisory Panel recommended that every CPF member be allowed to withdraw as a lump sum up to 20 per cent of his retirement balances - no matter how low.

The change will mean that even CPF members who fall far short of the Minimum Sum will be able to take out a chunk of their savings, further shrinking the already modest monthly payouts they will receive in old age.

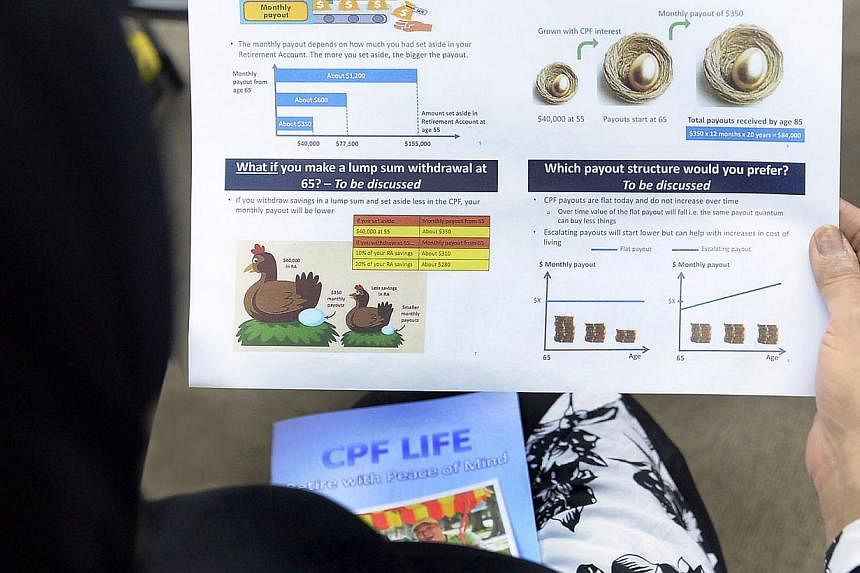

So, someone with $40,000 in his CPF Retirement Account at age 55 will be able to withdraw a lump sum of up to $7,700 when he turns 65. If he does so, his monthly CPF payouts in retirement will fall from $360 to $320.

Granting this flexibility seems to undermine the CPF's objective of ensuring people in the lower-income and lower-middle-income groups have an adequate stream of income for their needs, from the time they stop work until they die. For the people most likely to make lump sum withdrawals are the ones who can least afford to do so, that is, those with insufficient CPF savings to begin with.

So, what was the panel of 13 experts comprising academics, financial industry practitioners, and union and grassroots leaders thinking when they came up with this recommendation?

The cynics might say: Well, they were probably steered down this path to placate those who have been lobbying to get hold of some of their CPF savings, and sooner rather than later.

To be sure, the Government cannot afford to ignore ground sentiments on a political hot potato like the CPF.

But responding to ground sentiment is not just about caving in to populist pressure ahead of the polls. It is also about maintaining enough trust and support in the CPF system to ensure it remains a viable mandatory retirement savings scheme for the long term.

In crafting policy, national leaders must balance both the hard numbers of retirement adequacy and the soft sentiments of people nearing retirement age, who want to mark that milestone in their lives and need some cash to do so.

As Nanyang Technological University economist Walter Theseira noted in a commentary published in The Straits Times on Wednesday: "The reality is that many lower-income CPF members will face great difficulty maintaining an adequate standard of living in retirement from CPF savings alone. While flexibility may worsen their situation somewhat in the long run, refusing to grant flexibility, by itself, does not address their basic problem of inadequate lifetime savings."

Both he and the panel believe that this group of CPF members are best helped in other ways, with Dr Theseira mentioning other countries' practice of providing a minimum basic pension.

The panel also reported that, according to their study of how much current retirees spend, using figures from the Household Expenditure Survey, they project that a lower-middle-income worker who stops work in 10 years' time will need $650 to $700 a month.

Based on that, they have proposed a new Basic Retirement Sum of $80,500 which CPF members must set aside in their Retirement Accounts when they turn 55.

The share of active CPF members who can meet this Basic Retirement Sum will go up over time, from 55 per cent of the cohort who turned 55 in 2013 to 70 per cent of those who turn 55 in 2020. That means the problem of people not having enough in their CPF accounts for their retirement should shrink over time.

The older cohorts who tend to have lower CPF balances are also likely to have a significant asset in their homes, and schemes exist to help them monetise that asset.

For those reasons, a big overhaul is unlikely. Instead, the reforms will be refinements to enhance the CPF's relevance and continued acceptability, given the panel's conclusion that the "CPF system is fundamentally sound".