Property tycoon Kwek Leng Beng once observed that human nature is such that the higher real estate prices go, the more a person wants to buy a property, but the lower they go, the more scared the would-be buyer becomes.

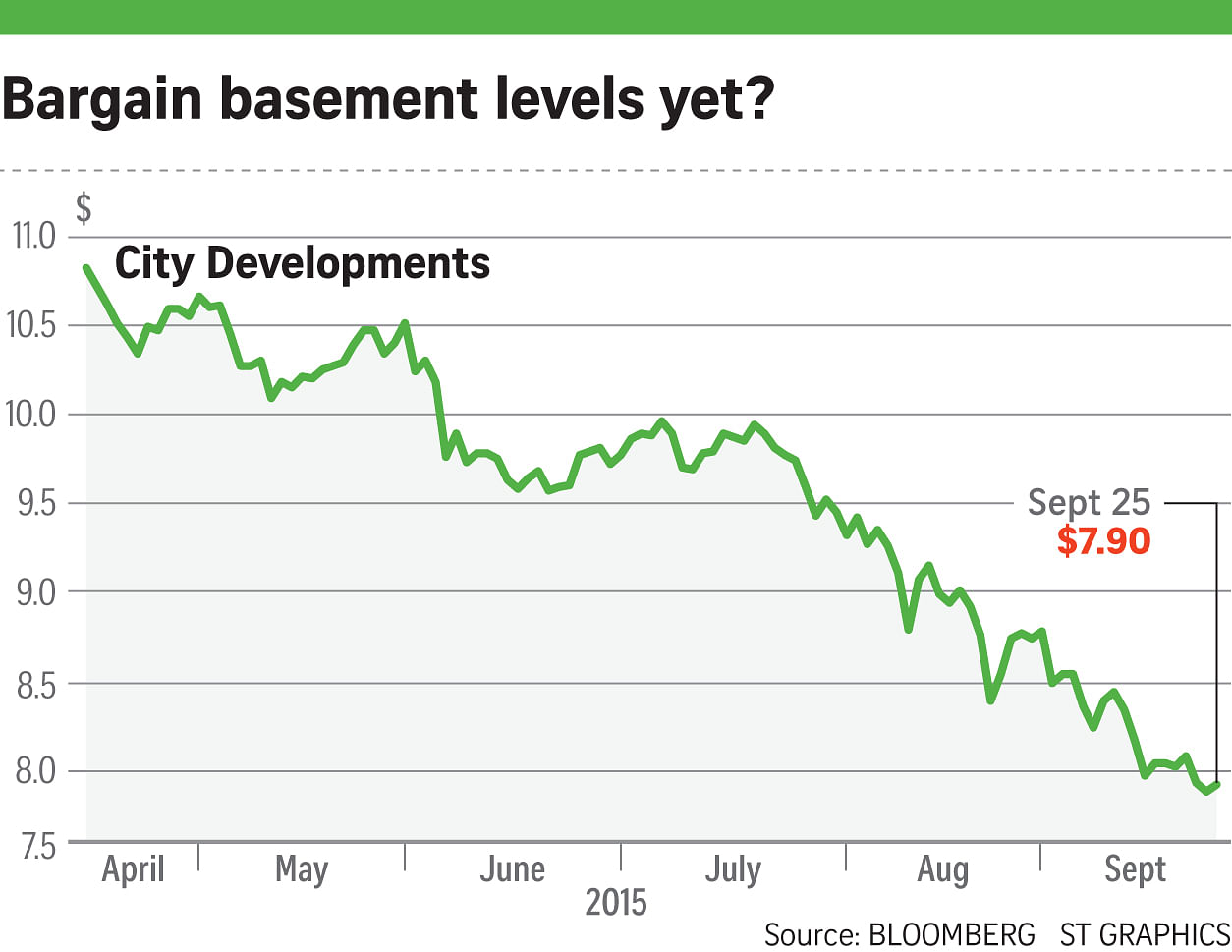

His observations about the residential market may well apply to trading of property counters as well. Private residential prices have fallen only about 6.7 per cent from the peak hit in the third quarter of 2013, yet the shares in City Developments (CDL), the property giant controlled by Mr Kwek and his family, have fallen 21 per cent to a seven-year low of $7.90 in two months.

This drop is steeper than the 15 per cent decline registered by the Straits Times Index in the same period.

Yet while CDL's share price works out to an attractive 38 per cent discount to revalued net asset value (RNAV), according to US investment bank Morgan Stanley, there appear to be few bargain-hunters nibbling at the counter.

CDL is not the only property counter facing this dilemma.

For UOL Group, even its elevation to the STI has failed to boost its share price. Unlike Yangzijiang and Sats - both of which made sharp gains after the announcement of their additions to the index three weeks ago - UOL shares have scarcely budged.

One question to ask is whether investors should be gung-ho enough to load up on property counters now that they are trading at big discounts to their RNAVs.

Some would recall that in 2011, when the STI was languishing at around 2,850 like now, there were analysts who stuck out their necks to make "buy" calls on property counters. The prevailing argument was that some real estate bosses might take advantage of their companies' depressed stock to buy out the remaining minority shareholders.

Those who made the right wagers then were rewarded handsomely when counters such as SC Global and Singapore Land were subsequently taken private while beverage-cum-property giant Fraser & Neave became the subject of a $13.8 billion takeover by Thai billionaire Charoen Sirivadhanabhakdi - the largest takeover in Singapore's history.

But the wave of privatisations and takeovers between 2012 and early last year occurred amid cheap funding, thanks to the United States Federal Reserve flooding the world's financial system with as much as US$85 billion of fresh money each month.

The circumstances have changed dramatically.

Investors are on edge as they wait for the Fed to decide when it plans to hike interest rates - its first such move in nearly a decade - as it tightens the screws on the loose monetary policy it had unleashed following the global financial crisis seven years ago.

Research houses have also been more circumspect on their calls on property counters, as they work out the various scenarios that may surface as interest costs shoot up and factors such as a slowdown in the region's economic powerhouse, China, kick in.

There were even dire warnings from brokerage Maybank Kim Eng that, in a worst-case scenario of falling revenues, rising interest costs and a 10 per cent drop in the value of the Singapore dollar, one or two major developers may not even have sufficient cashflow to cover interest payments.

Investors, hoping for a turnaround in property counters, are pinning their hopes on the Government tweaking the various anti-speculation measures put in place between 2008 and 2013 to cool the then sizzling residential markets.

These would include adjusting the additional buyer's stamp duty and removing the seller's stamp duty to encourage more residential purchases.

But would these tweaks - if they materialise - be sufficient to stir interest in property counters?

Some economists have noted that US studies suggest that while curbs on loan-to-value ratios and stamp duties were effective as tightening tools, loosening them tended to have less of an impact.

So merely tweaking the anti-speculation measures may not lure property buyers back to the market. Worse, buyers may still want to take a wait-and-see attitude, given concerns over a glut in the private residential market and that rents have been declining for the past 2 ½ years.

This sentiment may worsen, given the large number of units coming on-stream.

Around 12,000 units came on-stream each year between 2010 and 2013, but there were 19,941 units completed last year and another 42,000 homes are slated for completion this year and next.

Hence, it is not surprising to find Morgan Stanley arguing in a recent report that investors should not be focusing on the "cheap" 38 per cent discount to RNAV which they would get from even a conservatively-run developer such as CDL at its current depressed share price.

Instead, it said that, given the likelihood of a stagnant earnings environment, a more relevant yardstick would be to focus on CDL's price-earnings multiple.

Based on such a measure, it comes up with a target price of only $8.30 for the stock. This is well below the 12-month average target price of $10.45 set by analysts, according to Bloomberg.

Is Morgan Stanley right? With precious few catalysts to move the market, the question an investor should consider seriously before buying a property stock - or for that matter, any counter - is whether attractive valuations alone suffice as a reason to purchase.