Healthcare costs are likely to be one of our largest expenses during retirement, so it is no wonder that this issue consistently ranks high on the list of retirement concerns for many people.

To make matters worse, medical inflation has been rising at a much faster rate than consumer inflation.

For most people, one solution is to transfer some healthcare cost risks to insurers. Still, we have to brace ourselves and ensure that we set aside sufficient funds to afford rising insurance premiums.

In recent years, insurers offering private Integrated Shield Plans (IPs) - which enhance the basic hospitalisation cover from MediShield Life - have been grappling with thin profit margins, with some even incurring losses on such policies because of worsening health claims experience. In 2014 alone, IP insurers paid out claims amounting to $488 million. Last Thursday, the Life Insurance Association (LIA) released a study on health insurance cost in Singapore. Here are some of the highlights on IPs.

CLAIMS PAYABLE RISING FASTER THAN COST SAVINGS

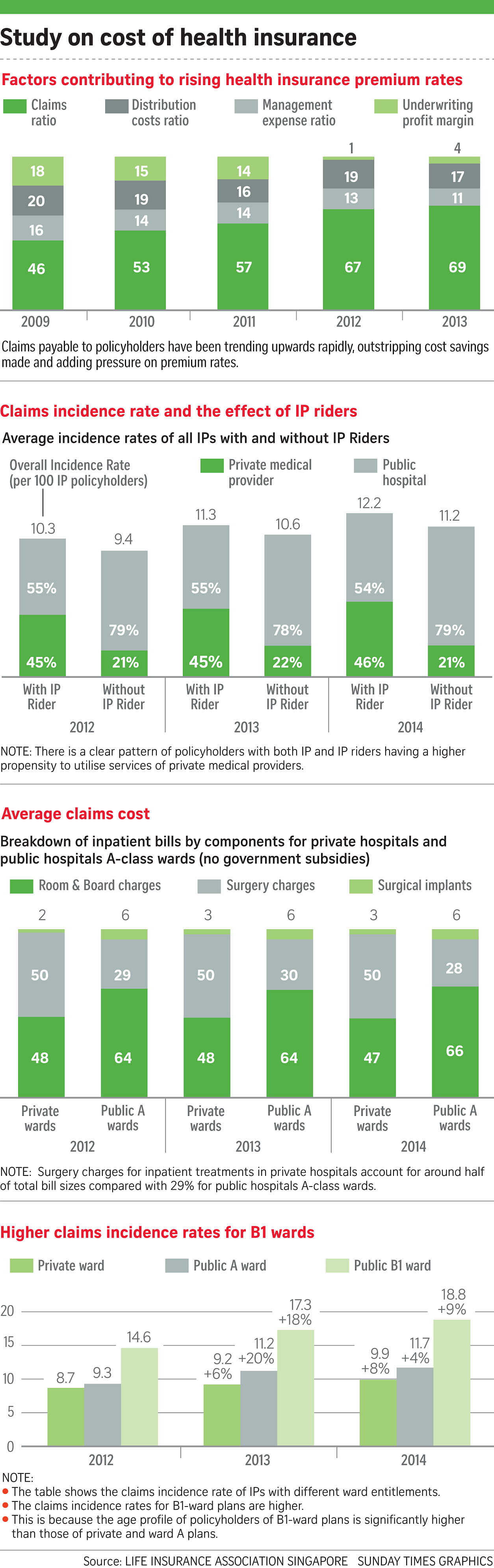

In the last few years, IP insurers have become more efficient but their cost savings were eroded by rising claims, according to the study. Since 2009, the share of management expenses and distribution costs as a proportion of total costs has declined. But the proportion of claims paid for hospitalisation and associated costs shot up from 46 per cent in 2009 to 69 per cent in 2013, outstripping the cost savings from management and distribution costs.

Profit margins have slid from 18 per cent in 2009 to around 4 per cent in 2013. In 2012, they were around 1 per cent. In fact, a recent report indicated that last year, the profit margin deteriorated further to minus 3.2 per cent - that is, the insurers lost money - on the back of the claims ratio rising to 79.4 per cent.

According to health insurance data, three out of five insurers - Aviva, Income and Prudential - incurred underwriting losses last year, while AIA and Great Eastern Life posted profits. French insurer Axa Life is the sixth IP provider. It entered the market in May.

RAPID INCREASE IN CLAIMS INCIDENCE RATE FOR IPs

The claims incidence rate is the rate with which policyholders make valid claims on their insurance plans.

The average IP claims incidence rate has been escalating at about 9 per cent a year, said the LIA. This includes policyholders who fall ill and require medical treatment in hospital or outpatient treatment for critical illnesses such as chemotherapy and kidney dialysis.

INFLATING AVERAGE BILL SIZES AT PRIVATE HOSPITALS

The study noted a sharp disparity between the inflation rate at private hospital wards and that at public hospitals between 2012 and 2014.

During the same period, the overall average bill incurred by IP insurers rose 8.7 per cent for private hospitals each year, compared with just 0.6 per cent for public hospitals. This covers inpatient bills, average day surgery and outpatient bills.

In terms of average inpatient bill sizes, private hospitals registered an 8 per cent rise per year compared with 2.7 per cent for public hospitals. For instance, for inpatient bills, the average private hospital bill was almost double at $12,105, compared with $5,955 in a public hospital, in 2014. For day surgery, the average private hospital bill was four times more.

IPs WITH IP RIDERS HAVE HIGHER CLAIMS INCIDENCE RATES

The study suggested that the design of a benefit influences the behaviour of policyholders and their propensity to spend on healthcare.

IPs with IP riders - some of which provide consumers with 100 per cent coverage - have slightly higher claims incidence rates compared with IPs without IP riders. And patients with riders run up bills that are 20 per cent to 25 per cent higher than those who have to bear a share of the cost.

According to the study, the figures may indicate that IP riders are giving the insured earlier access to medical treatment since out-of- pocket costs are no longer a concern. Policyholders with IPs and IP riders also have a higher tendency to visit private medical providers.

This is partly because with full-coverage riders, there is no guard against a potential "buffet" style of consumption by consumers and medical practitioners.

In a separate statement, the Ministry of Health said: "The absence of any co-payment may encourage overconsumption by some patients and over-servicing or overcharging by some healthcare providers, which will eventually increase healthcare costs and insurance premiums for all Singaporeans."

It is no wonder that one of the recommendations of the Health Insurance Task Force is for insurers to adopt co-insurance and/or deductible features so as to encourage consumers to play a more active role in managing their medical costs.

HIGHER SURGERY CHARGES IN PRIVATE HOSPITALS

In terms of the breakdown of inpatient claims costs, the average bills for three components - room and board charges, surgery charges and surgical implants - are higher in private hospitals than in public hospital A-class wards. In fact, surgery charges in private hospitals have the largest average inpatient bill component sizes.

From 2012 to 2014, surgery charges for inpatient treatment in private hospitals accounted for about half of bills, compared with 29 per cent for public hospital A-class wards. For public hospital A-class wards, room and board charges - which include the charge for room and board, daily treatment fees and miscellaneous fees such as for medical consumables - accounted for 66 per cent of inpatient bills, compared with 47 per cent in private wards in 2014.

HIGHER CLAIMS INCIDENCE RATES FOR B1 WARDS

On a positive note, there are higher claims incidence rates for class B1 wards. In 2014, class B1 wards had an incidence rate of 18.8 per 100 policyholders, compared with 11.7 for public hospital A-class wards, and 9.9 for private wards.

The study explains that the higher incidence rates are attributed to the age profile of policyholders of B1-ward plans being significantly higher than in the other plans.

This shows that B1-ward plans are a useful complement to the suite of IPs. They allow policyholders to downgrade their IPs as they get older and IP private-hospital plans get more costly.

The third instalment of The Sunday Times' legacy planning series will be published next Sunday.

WHAT THE TASK FORCE RECOMMENDS

The Health Insurance Task Force (HITF) last Thursday issued four recommendations aimed at reining in the rising claim rates of Integrated Shield Plans. Premiums have been rising as more people are making health insurance claims over time. Here are the recommendations to keep costs down:

Establishing a set of guidelines for medical fees, to improve transparency and so that people can get a better estimate of how much their treatments should cost.

Making clearer the process through which insurers can raise issues such as inappropriate or excessive treatment to the relevant authorities.

Improving insurance procedures and product features. This includes:

- Using panels of preferred healthcare providers to manage medical costs through agreements on fees.

- Making sure co-insurance and/or deductibles are included in the product design, so that some co-payment is still necessary. This is to prevent overconsumption.

- Getting insurers to approve claims for treatment and bills before the actual procedure is carried out, so that issues of inappropriate treatment and high charges can be addressed from the start.

Educating consumers on available options and the corresponding costs.

The 11-member task force comprises members from the Consumers Association of Singapore, the Life Insurance Association and the Singapore Medical Association, and is supported by the Ministry of Health and the Monetary Authority of Singapore. To summarise, the HITF highlighted the pressing need for closer collaboration among the stakeholders to ensure that healthcare and medical coverage remain affordable for all.