Q What are Singapore Savings Bonds?

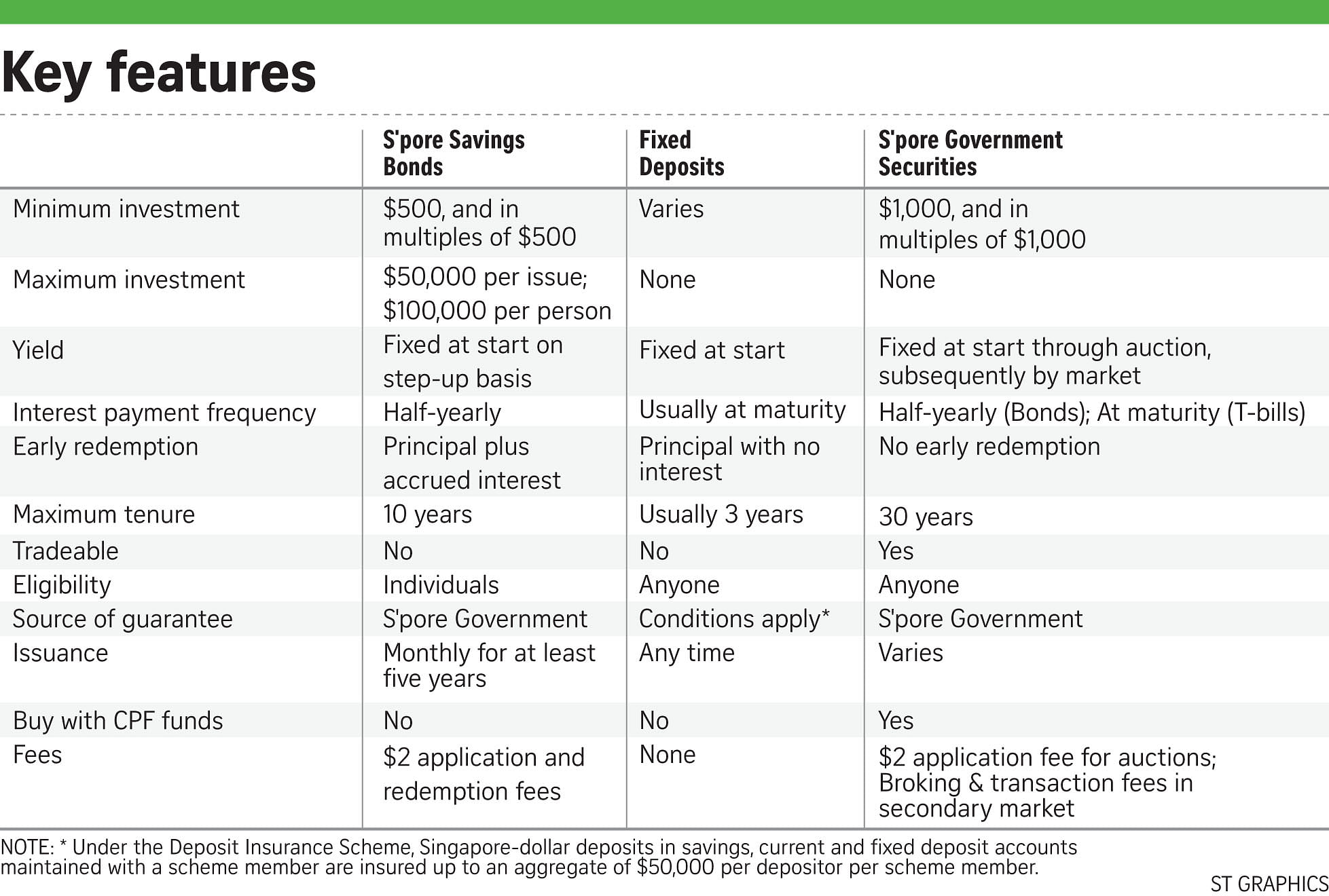

A The bonds are a special type of Singapore Government Securities (SGS) that offer a long-term, risk-free and flexible investment option for individuals.

They are in a unique class that combines the features of a fixed deposit and a regular government bond. Some of these features are the flexibility to redeem monthly with no penalty, the step-up interest rate, principal-guaranteed and the long tenure.

You will need at least $500 to invest in these bonds, lower than that of conventional SGS, which require $1,000, and retail bonds, which typically start at $2,000. Corporate bonds usually require $250,000. You can invest up to $50,000 in a Savings Bonds issue and hold up to $100,000 at a time.

Q When can you start buying Savings Bonds?

-

What finance experts say

-

Finance experts generally agree the bonds are suitable for most investors' investment portfolios as they are safe and very liquid.

Promiseland Independent managing partner Patrick Lim recommends them for retirees and risk-averse investors and as part of a diversified portfolio.

Mr Marc Lansonneur, DBS Bank's managing director and head of investment products (Singapore), believes they would be a good option for novice investors or those thinking of investing in such instruments.

However, he highlights the fact that the bonds cannot be pledged as collateral for loans or credit lines with financial institutions. Furthermore, holders of these bonds can redeem them only monthly while conventional bonds can be sold daily.

Mr Dennis Khoo, UOB's head of personal finance services (Singapore), said that as a savings tool, it would be better if the Savings Bonds' interest payments could be compounded but that is not the case. He recommends the bonds for consumers with low-risk appetites and a long-term horizon. "If investors have a short-term horizon, they should consider fixed deposits which provide better returns than Savings Bonds," he added.

As the interest rates are locked in at the start, that may place investors in a "disadvantageous" position in a rising interest rate environment. This is because future rates could turn out to be higher than the ones you get from your Savings Bonds.

In such a situation, you have the option of redeeming your bonds for the principal with no penalty and apply for new Savings Bond issues with higher interest ratesif you find the latter more attractive.

However, do consider whether a new Savings Bonds issue with lower initial interest payments outweighs the stepped-up interest payments you would be receiving on an issue that you may have held for some years.

-

NEXT WEEK: How to apply for and redeem the bonds, and how they will be allotted.

A The MAS will announce details of the upcoming issue on the first business day of each month. The application period for each issue will open at 6pm on that day, and close at 9pm on the fourth-last business day of the month.

After the opening day, applications can be submitted from 7am to 9pm, Mondays to Saturdays, excluding public holidays.

Application dates for each issue will be published on the Savings Bonds website (www.sgs.gov.sg /savingsbonds) and in newspapers one month before the bonds are issued.

Applications for the first tranche open at 6pm on Sept 1 and close on Sept 25. If your application is successful, you will receive your bonds on Oct 1.

The money will be deducted from your bank account upon application. If your application is unsuccessful or partially filled, any excess money will be refunded by the end of the second-last business day of the month.

Q What are the interest rates?

A The return for holding Savings Bonds until the 10-year maturity will match the average 10-year SGS yield, which has been between 2 per cent and 3 per cent.

The MAS will announce the interest rates as well as the returns over different holding periods when applications for each issue open.

Information for the first issue will be published on the Savings Bonds website after 4.30pm on Sept 1 and in newspapers the following day. There is also a hotline: 6221 -3682.

Interest is paid half-yearly on the first business day of the month. So for the first issuance, successful applicants can expect their interest on April 1 next year. Interest will be automatically credited into the bank account linked to your individual Central Depository (CDP) securities account. Your interest payments will be reflected in the CDP statement for the month that the interest is paid.

Q How does the step-up interest work?

A Unlike fixed deposits and conventional SGS, which pay the same interest rate annually, Savings Bonds pay interest that grows over time to give you an average rate linked to SGS yields.

This means the longer you hold your Savings Bonds, the higher the effective interest will be.

You will receive less interest at the start, but the amount "steps up" or increases over time. This is to compensate individuals for the longer investment period.

Let's say you invest $1,000 in a Savings Bond offering 0.9 per cent for the first year or $9, 1.5 per cent for the second year and so on. And the interest in the 10th year is 3.3 per cent.

In the second year, you will earn a higher interest compared with the first year so that on average over the two years, you would have received 1.2 per cent per annum.

Upon maturity, the average interest on your investment over 10 years would be 2.4 per cent a year. So if you have a shorter time horizon for your savings, say up to two years, you may be better off placing your cash in fixed deposits or operating savings accounts that offer higher interest rates.

When working out the returns on your Savings Bonds, do take into account the $2 non-refundable transaction fee for each application and redemption.

Send your views and questions about Singapore Savings Bonds to lornatan@sph.com.sg