-

One-third of SRS money lies idle as cash

-

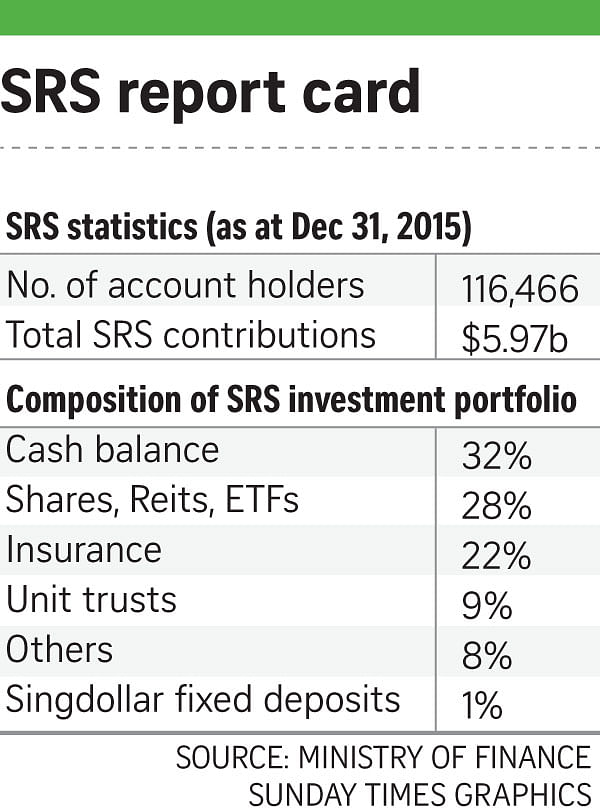

According to Ministry of Finance statistics, the number of Supplementary Retirement Scheme (SRS) accounts more than doubled to 116,466 last year from 53,656 in December 2009. The number was just 11,890 in the year of its inception in 2001. Total SRS contributions have surged to $5.97 billion since 2001.

Most SRS account holders are aged 36 to 55. This indicates that the scheme appears attractive mainly to middle- and high- income earners and those who are nearing retirement age. Another reason for the predominance of this age bracket is that most people typically do not plan for retirement till they are in their mid-30s or older.

You can make your SRS contributions work harder by buying into various investment instruments such as shares, exchange- traded funds (ETFs), real estate investment trusts (Reits), bonds, structured deposits, fixed deposits, single-premium insurance plans and unit trusts. Direct property investments are not allowed.

However, the statistics show that a significant proportion - 32 per cent or about $1.9 billion of SRS funds - is lying idle as cash. Among the SRS-approved instruments, shares, Reits and ETFs are the most popular, accounting for 28 per cent of an SRS portfolio, followed by 22 per cent parked in insurance plans.

Ms P'ing Lim, head of deposits and secured lending at DBS Bank, noted that its customers have been taking a proactive approach to the funds in their SRS portfolios. This shows that a large number of them are savvy enough to use their SRS accounts concurrently for tax savings and investments.

"Close to 70 per cent of the contributions are invested in equities, unit trusts, shares, bonds and insurance products. We are seeing more SRS account holders using their funds to purchase single-premium bancassurance (insurance sold via banking channels), unit trusts and equities," said Ms Lim.

"SRS is increasingly popular with our customers and we are seeing a growth rate of 20 per cent year on year. Over 70 per cent of new SRS accounts with DBS are opened via iBanking," she added.

DBS is the only bank here that allows customers to open and contribute to SRS accounts via online banking instantly. The other two SRS operators are OCBC Bank and United Overseas Bank.

For those taxing times, think SRS

The Supplementary Retirement Scheme allows one to build up nest egg and obtain some tax relief

Want to reap some tax savings on this year's assessable income?

You still have time - until the end of December - to park some cash in your Supplementary Retirement Scheme (SRS) account to do just that.

Introduced in 2001, the SRS complements the Central Provident Fund by providing wage earners with an avenue to build up their nest eggs and obtain some tax relief at the same time. A voluntary programme, SRS enables members to contribute varying amounts to it as often as they wish - subject to a yearly cap - before Dec 31 each year.

The annual contributions are capped at $15,300 for Singaporeans and permanent residents, and $35,700 for foreigners.

BENEFITS OF SRS

The main advantage of the scheme is that SRS account holders can enjoy dollar-for-dollar tax relief. Each dollar contributed to the SRS reduces one's taxable income by the same amount, said Ms Chung Shaw Bee, head of wealth management for Singapore and the region at UOB.

You should note that half of the withdrawals from an SRS account is taxable upon retirement. But with planning, it is possible for individuals to make withdrawals on a yearly basis without paying taxes after age 62, she added.

However, premature withdrawals, except in certain cases such as on medical grounds and death, are taxable in full. In addition, a 5 per cent penalty applies to discourage such premature withdrawals, said Mr BJ Ooi, head of private client services, tax, at KPMG in Singapore.

Mr Ling Seng Chuan, head of deposits at OCBC Bank, said SRS accounts are best suited to customers planning for their retirement.

"In using the SRS account as part of their retirement planning, customers can benefit from a reduced taxable income. In addition, customers can opt to utilise the funds in their SRS accounts to make investments to grow their retirement funds," he said.

At 62, you can choose to withdraw a lump sum or spread your SRS withdrawals over a period of 10 years. You can withdraw up to $40,000 each year from an SRS account without any tax, assuming you have no other taxable income. This amount can be increased by the amount of personal reliefs you can claim.

This is because 50 per cent of the withdrawal is tax exempt and up to the first $20,000 of chargeable income is currently tax-free, advised Ms Wu Soo Mee, partner at Ernst & Young Solutions.

SRS members may no longer contribute to SRS after they start withdrawing from their SRS accounts at or after the statutory retirement age that was prevailing when they made their first SRS contribution (currently 62) or on medical grounds, noted Ms Wu.

According to DBS Bank, close to half of the SRS accounts here are with the bank and it usually sees a rise in contributions in the lead-up to the Dec 31 deadline. DBS customers can look out for bank promotions during this period at www.dbs.com.sg/srspromo

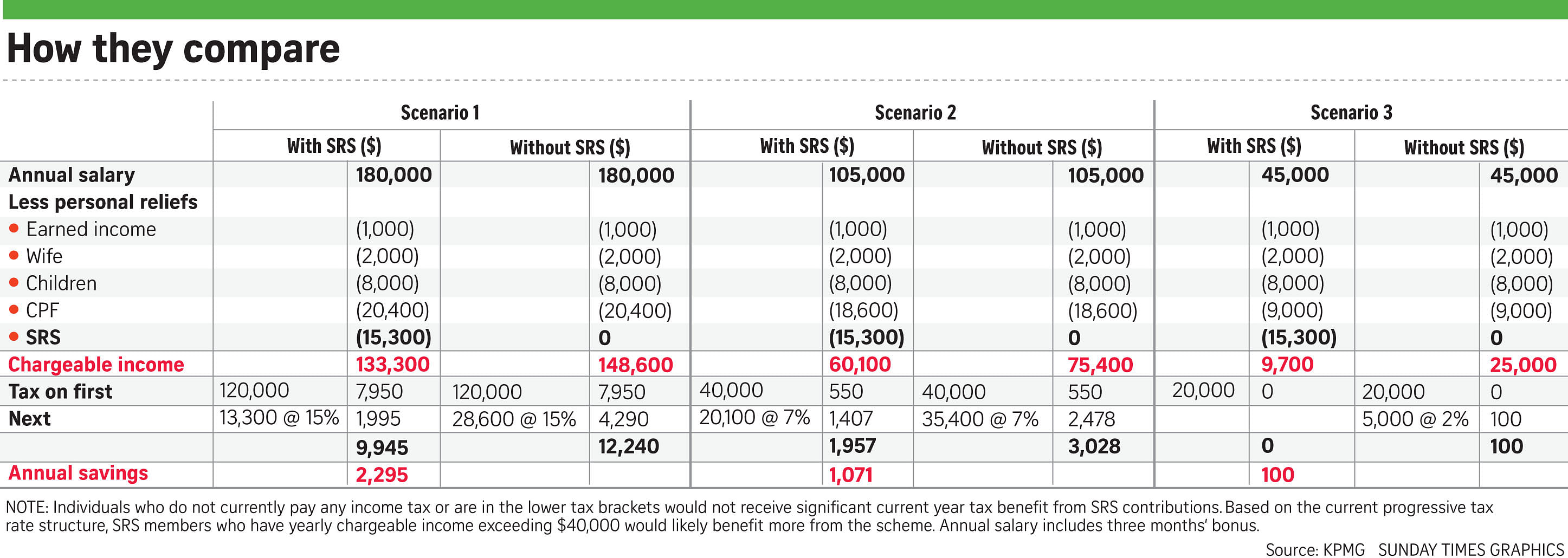

WHO BENEFITS MORE FROM SRS?

Mr Ooi pointed out that individuals who do not currently pay any income tax or are in the lower tax brackets would not receive significant current-year tax benefits from SRS contributions. "Based on the current progressive tax rate structure, SRS members who have a yearly chargeable income exceeding $40,000 would likely benefit more from the scheme," he said.

Investors who earn more than $40,000 annually pay 7 per cent income tax. Hence, the SRS would be more beneficial for them, as they would save a substantial amount in tax compared with investors earning less than $40,000, who pay a lower rate of income tax.

HOW MUCH TO PARK IN SRS?

One way of figuring out how much you should put into the SRS is to have an idea of how much you will need from the scheme during your golden years. The next step is to figure out how many years you want to contribute to it.

For example, if you require $150,000 from the SRS during your retirement, you could spread out annual contributions of $7,500 over 20 years - if you do not make any returns on the money.

But if you can make your money work harder by investing it, you can set aside $5,100 annually over 20 years, and end up with the same $150,000 figure, assuming a 4 per cent yield on your investments.

Ms Wu cautioned that an individual should consider his own financial situation before deciding the amount he can afford to set aside for the entire period up to retirement, when withdrawals can be made penalty-free and with the 50 per cent tax exemption.

One possible drawback of the SRS is that the money is pretty much locked up, as early withdrawal from an SRS account may incur a 5 per cent penalty and 100 per cent of the withdrawal sum will be subject to tax. This not only negates the tax savings but also adds cost for saving into the SRS.

While most contribute to SRS only towards the end of the year to save on their income taxes, Mr Ling and Ms Chung recommend regular monthly contributions instead.

By doing so, customers can include the more manageable amount in their monthly budgets. And separating the contribution amount into smaller sums will be less of a financial strain.

SRS members should note that a new personal relief cap of $80,000 per year of assessment will take effect from the Year of Assessment 2018. Ms Wu said this means there will be no tax relief available for individuals who are already hitting the personal relief cap (even before taking into account the SRS relief) for their contributions to the SRS.

WHAT SHOULD YOU INVEST IN?

Financial experts say it makes sense to invest your SRS funds. If you choose not to, your SRS operator will pay you the current paltry bank interest rate of 0.5 per cent. This means inflation will slowly erode the value of your SRS money over time.

It is also prudent to start investing as early as possible so that you get the most out of compounding the returns. "Having a long time horizon can help to smooth out the impact of market volatility on investment holdings. In drawing up one's retirement plan, the SRS should be used as one of the planning tools to supplement other investment options," said Ms Chung.

But do your homework first and consider the investment risks.

At UOB, the investor's risk-profile will be taken into consideration before any recommendations are made. "Investors should always understand that for higher returns, a higher amount of risk has to be taken. Hence, it depends on factors such as the investor's risk appetite, time horizon, comfort and level of understanding of the investment products," said Ms Chung.

Mr Vasu Menon, OCBC Bank's vice-president and senior investment strategist, said that as the SRS is intended for long-term needs like retirement, he recommends that it should ideally be invested with a long-term view. "For those with a strong risk appetite, stocks or equity-related unit trusts can be considered. These instruments may be more volatile, but if the customer can stomach the volatility, they may produce better returns than deposits in the long term."

"However, before investing, it is important to do one's homework, invest carefully and monitor investments regularly," advised Mr Ling. "Other kinds of unit trusts to consider are multi-asset funds and funds that invest in a diversified basket of income-yielding instruments that offer a regular and decent income payout, which may be appealing, given the low interest rates."

For those with a lower risk appetite, selected single-premium endowment products can be considered, some of which offer guaranteed returns, such as OCBC Bank's Single Premium Special 1.88 per cent five-year endowment plan, he said.

SRS members can opt to maximise their returns in the earlier years and consider shifting towards safer and more stable returns as they approach retirement. From July last year, SRS members have been able to withdraw an SRS investment by transferring the investment out of their SRS accounts, without having to liquidate their SRS investments, subject to certain conditions.

Join ST's Telegram channel and get the latest breaking news delivered to you.

A version of this article appeared in the print edition of The Sunday Times on November 06, 2016, with the headline For those taxing times, think SRS. Subscribe