If you are looking at retirement planning, then the national annuity CPF Life (Lifelong Income For the Elderly) scheme is as good a starting point as any.

After all, as life expectancies continue to increase, having an income throughout our old age that can help support a basic level of retirement is more important than ever.

Launched in 2008, the CPF Life scheme offered 12 different plans back then but these were pared to four and again to just two - the Standard and Basic Plans.

A recent change to the scheme gives the option to choose our CPF Life plans only when we wish to start our monthly payouts. We can do so any time between age 65 (payout eligibility age) and 70. This applies to CPF members who turned 55 on or after July 1 this year.

Before this change, the decision on the Life plan had to be made at age 55 for those born on or after 1958 until June 30 this year.

To recap, each Life plan provides different trade-offs between the monthly payout amounts and the bequest you would leave your beneficiaries. Simply put, the Standard Plan provides a higher monthly payout and a lower bequest; it's the reverse for the Basic Plan.

Currently, you will be put on CPF Life if you have at least $40,000 in your Retirement Account when you reach 55 or $60,000 when you hit 65.

The Retirement Account is created at age 55 using the savings in your Special and Ordinary Accounts. If you are not placed on the CPF Life scheme, you can choose to join it any time before age 80.

CPF Life starts paying your monthly payouts on your eligibility start age, currently age 65 although this changes in January.

You will then have the option to start the payouts later, up to age 70. For every year of deferred payouts, your monthly payouts will grow by about 6 per cent to 7 per cent.

Note that cash top-ups beyond the current Full Retirement Sum ($161,000) will not attract tax relief.

The CPF Board says more than 140,000 people have joined the CPF Life scheme, 62,000 of those since 2013. That was the year it became compulsory for Singaporeans or permanent residents who reached 55.

About 70 per cent of this 62,000 are on the Standard Plan while the rest are on the Basic Plan. The Standard Plan is the default if you do not opt for either one.

About 60,000 people will turn 55 each year.

Let's see how the two plans work.

CPF LIFE STANDARD PLAN

Members who join this plan at age 55 will have the Retirement Account deducted for their CPF Life annuity premiums in two instalments - at age 55 and near 65.

The first deduction is up to the current Basic Retirement Sum of $80,500. The premium goes into the Lifelong Income Fund.

Two months before you reach 65, the balance Retirement Account savings will be deducted as the second instalment of your annuity premium and channelled into the Lifelong Income Fund. This will include any new money, including interest earned or refunds from sale of property or investments that you have built up between your 55th birthday and 65.

For members who join the Standard Plan on their payout eligibility age or after, there will be only one annuity premium deduction, which is all the sum in their Retirement Account,made at the time of joining.

You will get monthly payouts from the Lifelong Income Fund for the rest of your life once you reach the eligible age.

CPF LIFE BASIC PLAN

For those who join this plan at age 55, there will be two instalments deducted as annuity premiums - like the Standard Plan - but the percentage of deductions differs.

At 55, the first deduction is about 10 per cent of the Retirement Account savings, to be paid into the Lifelong Income Fund. The exact amount will be made known to you when your CPF Basic Plan is issued.

The rest - about 90 per cent - of the Retirement Account savings is untouched and can continue to grow and compound with interest.

Two months before you reach 65, there will be a second deduction. This time, it will be approximately 10 per cent of the new money that has built up between your 55th and 65th birthday. The rest of your Retirement Account savings will stay put until your payout eligibility age.

For members who sign up for the Basic Plan at their payout eligibility age or after, there will be only one annuity premium deduction at the point of joining the scheme.

You will receive monthly payouts from your Retirement Account savings until one month before you reach 90. By then, the Retirement Account money would have been depleted and your monthly payouts will be from the Lifelong Income Fund for as long as you live.

MONTHLY PAYOUT AND BEQUEST

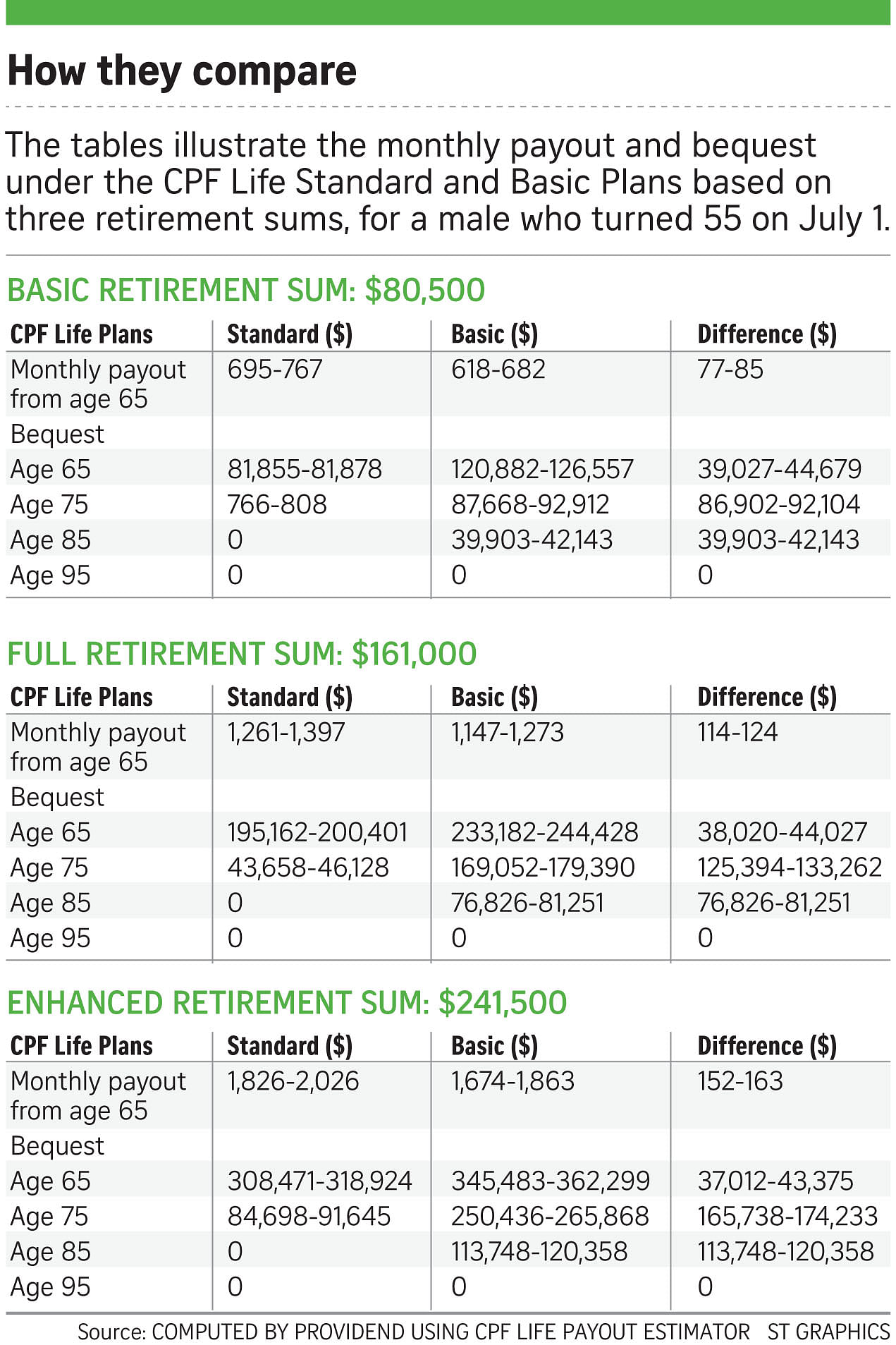

Financial advisory firm Providend computed three tables using the CPF Life Payout Estimator (available on the CPF website) to illustrate the estimated monthly payout and bequest under the two plans based on three different retirement sums (Basic, Full and Enhanced).

The figures are based on a male who turned 55 on July 1 this year.

It shows that while the difference in estimated monthly payouts between the two plans is in a narrow range, from $77 to $163, the bequest left for beneficiaries differs significantly, up to about $174,000, depending on the age that death occurs.

Both plans offer zero bequest for those who live beyond 95.

CHOICE OF CPF LIFE PLANS

Ms Catherine Lee, 56

Based on her projected retirement needs, Ms Lee selected the Standard Plan in July last year when she turned 55. Her rationale was that she wanted a higher monthly payout than what the Basic Plan offers. She is not too concerned about leaving a larger bequest for her two sons as they should be self-sufficient financially.

Mr Patrick Tan, 56

When Mr Tan (not his real name), turned 55 last November, he asked the CPF Board about the two plans. He realised the difference in monthly payouts between the plans is about $100 but the bequest amounts differ substantially.

"The monthly payout difference is small, something I could stomach. I would rather keep the higher bequest for my family. At age 75, if I were to kick the bucket, the difference in bequest is a lot.

"I want to contribute as little to the pool (Lifelong Income Fund) as possible," he adds. He finally selected the Basic Plan but is now considering deferring his CPF Life plan.

Mr Jimmy Tan, 62

Although it was not compulsory for Mr Jimmy Tan - as he was born before 1958 and hence could opt in any time between age 55 and 80 - to be placed on the CPF Life, he opted for the CPF Life Plus Plan in December 2010 when he was 57.

He believed it would be financially beneficial to opt in early. The CPF Life Plus Plan, which will provide him with a higher monthly payout than the Standard Plan but will leave less for his beneficiaries, is no longer on offer.

It was only last year, after Mr Tan retired, that he visited CPF Board for more information. He was disappointed at what he learnt.

"If I pass away before my payout eligibility age (64), only the amount deducted from my Retirement Account savings as annuity premium into the Lifelong Income Fund will be returned to my beneficiaries. The interest earned (on the premium) will remain in the pool, so I'm subsidising the rest.

"Based on my Retirement Account savings of $110,000, I calculated that the interest I could potentially lose is more than $30,000 (in that scenario)."

He also did not know that the difference in bequest would be significant if he does not live past 90.

"People say you may not need to leave a large bequest for your children, but if the amount is substantial, why wouldn't I leave it?"

Mr Tan wished that CPF Board had proactively given enough information or invited members to provide face-to-face advice.

CPF Board says

For CPF members already included under CPF Life - whether they were auto-included or had opted in - there is no need for them to take any action.

However, if they wish to change or defer their plan selection, they can write to the CPF Board before they reach their payout age, and their requests will be reviewed.

For successful requests, only the unused annuity premiums (that is, without interest) will be refunded to the Retirement Account. This ensures the payouts of other members who have committed to CPF Life are not affected, as the interest earned on premiums is pooled.

Mr Christopher Tan, member of CPF Advisory Panel, says

Financial advisory firm Providend's chief executive, Mr Christopher Tan, says CPF members can choose the Basic Plan if the difference in monthly payout is not going to materially affect their lifestyle, as the bequest amount is significantly more.

"But for the lower-income individual, which the CPF Basic Retirement Sum is 'sized' for, they should consider opting for the Standard Plan. This is because it is likely that the difference of about $100 is going to make a material difference to their lifestyle.

"When you buy an annuity, the focus should be on the payout and not on the bequest."

As for himself, he would choose the Basic Plan since the difference in monthly payout is not going to affect him significantly.

Mr Tan encourages CPF members to top up the CPF accounts of lower-balance or non-working family members once the members have savings above what they require for the Basic Retirement Sum. By doing so, it ensures that the spouse will have his or her own CPF Life payouts when the member dies.

This is one of nine recommendations from the CPF Advisory Panel that will be made available some time soon.

Invest editor says

If you are not on CPF Life yet, joining later makes more sense as you would be clearer about your financial situation by the ages of 65 to 70. This will help you decide which CPF Life plan to take based on your retirement needs.

And if you wish to delay pooling the interest on your annuity premiums in the Lifelong Income Fund, it is another reason for joining the scheme later. So if you die before your payout start age and you still haven't joined the scheme, your entire Retirement Account savings would be refunded to your estate or beneficiaries.

However, if you have already joined the CPF Life scheme and wish to change or defer plans, you should do your sums carefully.

As the interest (on your annuity premiums) will not be refunded to your Retirement Account, it may not make sense to leave your current CPF Life plan now because you may be entitled to a lower monthly payout and bequest when you rejoin later.

Last month, the CPF Board launched a pilot project where it invited some individuals turning 55 for a face-to-face meeting. This is indeed a welcome move to enhance understanding of their options.

You can also take an active interest in your own retirement savings and find out more from the CPF Board at any time.

As the saying goes, failing to plan is as good as planning to fail.