The other day, I was asked how banks can foster breakthrough innovation within the organisation. My answer: "You may get lucky with some, but the more likely course is iterate, experiment, fail, learn, pivot, repeat."

The same experimental journey was taken by many successful social media companies we see today. LinkedIn started as a dating network; Facebook as a site to rate the attractiveness of individuals. Both experimented and morphed over time. Companies such as Amazon, Facebook, Google, and Netflix are widely acknowledged as leaders in innovation.

What sets them apart is their ability to constantly experiment, automatically scale, and rapidly bring new features to market.

As DBS moves along in our journey in digital transformation, we are also embracing an innovation mindset. Such a paradigm breaks away from what bankers are used to: namely, the need to have all the answers upfront, or the need to have certainty of outcomes. Instead, uncomfortable though it is, we have been shifting to an environment where it is perfectly okay to not know if something will work.

What this translates to is fostering a culture of experimentation. The thinking is that if we are able to increase the surface area of ideas springing up within the organisation, there is higher probability that some of them will be the great success stories of tomorrow.

We also seek to cultivate a fintech-like culture among our 22,000 people. We believe that innovation is not just the mandate of our innovation group; but we are rewiring the core of the bank so that at every level, and across every department and team, people are energised and equipped to come up with new ideas and initiatives. Last year, we ran over 1,000 experiments across the bank, and in this way, a culture of innovation at DBS goes broader and runs deeper than at many organisations.

It is also against this backdrop that we are actively finding ways to mentor, partner and support fintechs, whom we see as more of an opportunity than a threat.

Players like Alibaba, Paytm, Fastacash, SeedInvest, WeCash, MoneyLover, Jitta and so on have come up across India, China and South-east Asia. They are disrupting financial services such as payments, remittances, crowdfunding, loans, brokerage, personal finance, investment and insurance.

The rapid spread of fintechs might indicate success, but the reality is that only a few have made it. There are three main reasons. Firstly, their solutions are unproven. Secondly, customer acquisition has remained a challenge - traditional banks are still seen as safer than online banks. And banks themselves have woken up to the threat of fintech and are rolling out online services for customers who might otherwise have moved to newer, nimbler players.

Traditional banks like DBS can leverage the best of both worlds. Banks still have existing advantages such as safety and trust, deep expertise in banking products, managing risks, processing capabilities and data pools.

Fintech companies are customer centric, nimble and agile, and are always innovating and experimenting. Banks that can marry the two, such as BBVA, Citi and ING, are showing the way forward.

For this reason, in Singapore and Hong Kong, we have been running a number of pre-accelerator programmes, which allow us to stay connected with new, emerging financial technology; to have a first shot at any opportunities for partnership, and to forge a banking relationship with start-ups.

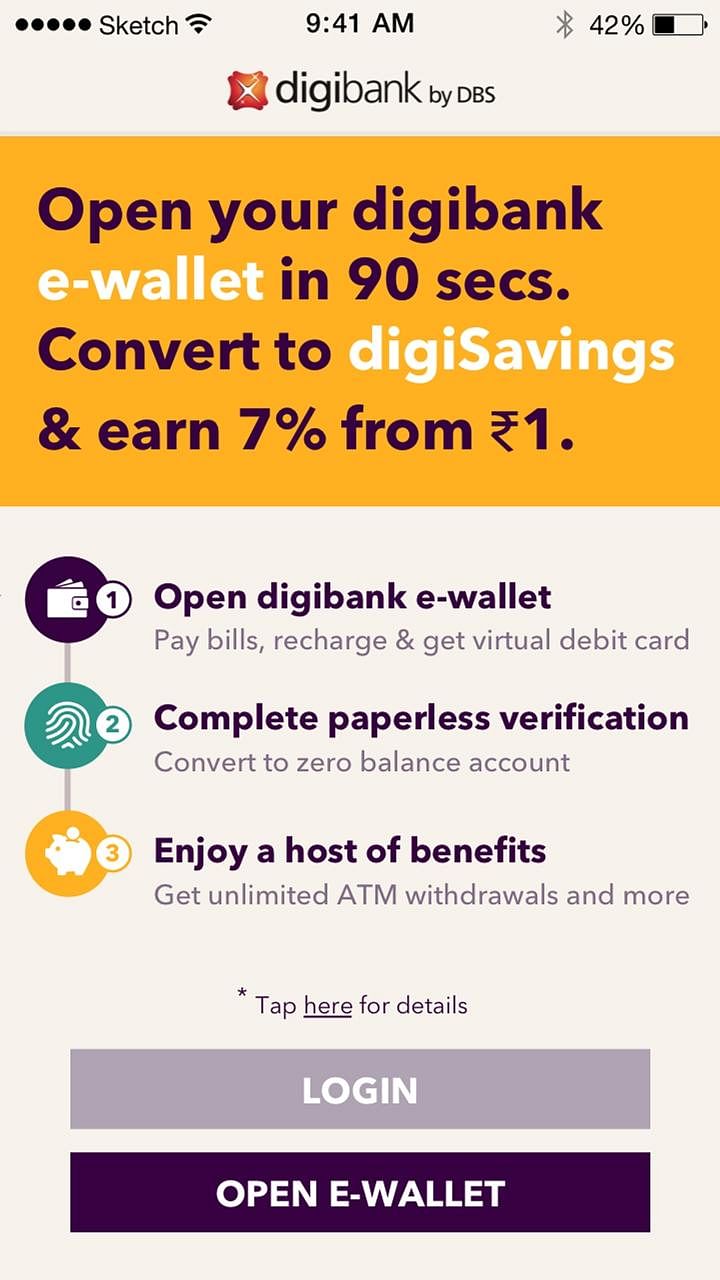

Where we can, we will also bring fintech into our platforms. In May this year, DBS launched digibank, India's first mobile-only bank.

The offering is groundbreaking in that it combines a set of new technologies including biometrics, artificial intelligence, an intuitive recommendation engine, and soft token technology. To bring this all together, the offering combined a few start-up products: the AI technology was from Kasisto, which is a spin-off from the company that created Siri in the United States. The recommendation engine and the virtual key were products of two Singapore start-ups, Moneythor and V-Key.

With the opening of our new innovation facility, DBS Asia X, to coincide with the inaugural Singapore Fintech Festival, we hope to foster greater collaboration with fintechs, while providing an innovative space for our people to embrace a new way of working; being open, collaborative, and experimental.

I firmly believe if banks can be pivoted to operate like start-ups, we can secure our future in the midst of digital disruption. Embracing fintechs, integrating them and cultivating a fintech mentality are central to winning.