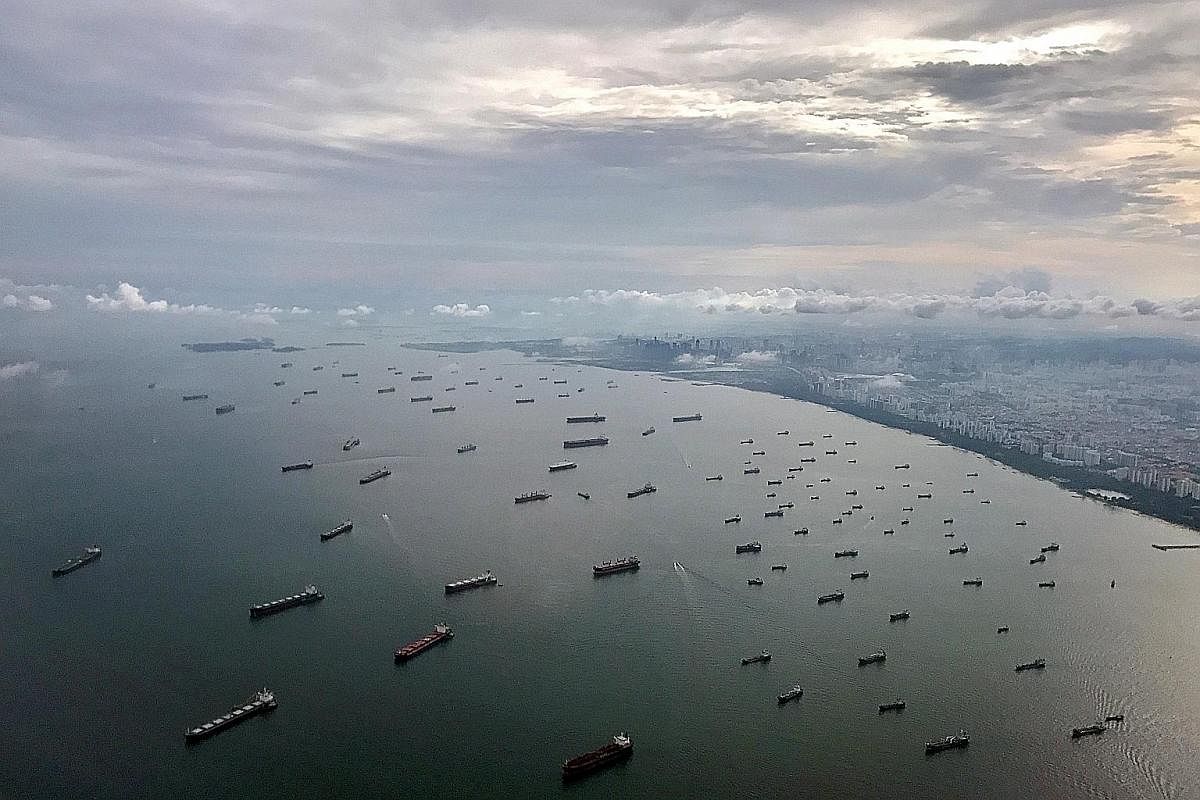

2017 Yearender: Shipping sector

12 months of calm seas, but...

Shipping market has improved this year, but overcapacity and price wars continue to roil sector

PHOTO: REUTERS

After years of blood-letting and a never-ending race to the bottom, global shipping lines have enjoyed a calmer 12 months but as all good sailors know, storms can come at any time.

Industry observers are fully aware that the toxic issues that have been roiling the sector - price wars and overcapacity - are lurking just over the horizon, ready to wreak more havoc.

Mr Andy Lane, a partner at shipping consultancy CTI Consultancy, reckons "2018 looks tricky to navigate and to predict, so a major recovery appears a little unrealistic".

"Without explosive growth, we are unlikely to see the gap between supply and demand close materially, until 2020 at least - and even that is based on the assumption that there is 'sensible' new ship ordering, which is never a given."

Mr Lane acknowledges the market this year has "vastly improved" over 2016 - the year that saw the collapse of South Korea's once-mighty Hanjin Shipping Co. "We see many of the shipping lines talking up the industry. Some of this is to gain investor confidence, some is wishful thinking, and some is hype. There is little anecdotal evidence, however, that this bubble will be able to stand the test of time."

SHIP GLUT

The cut-throat race for a bigger slice of the market has not died down, even with the unprecedented wave of consolidation over the past two years.

Ocean Shipping Consultants director Jason Chiang said major players have unveiled plans to build new ships in recent months - "at a time when demand has barely kept up with supply".

Mediterranean Shipping Co, the world's No.2 carrier, for instance, announced plans in September for 11 new giant ships to be delivered from 2019, each to come with a staggering capacity of 22,000 twenty-foot equivalent units (TEUs). CMA CGM has also confirmed a US$1.2 billion (S$1.6 billion) order for nine such ships from 2020. It also has other vessel deliveries before then.

The 22,000 TEU ships weigh in as the largest vessels on order today.

"This does not bode well for 2018 and 2019. It could result in a decline in freight rates when the ships are deployed," says Mr Chiang.

At the same time, vessel scrapping has also slowed, despite a huge number of container demolition sales seen at the end of last year and the start of this year.

One reason is that charter rates for vessels have risen, says Mr Toby Yeabsley, head analyst of shipping data firm VesselsValue.

He believes more vessels need to be scrapped so the market can find a better balance, but points out that 2018 is set to be a "bumper year" for container vessel deliveries, with 224 ships scheduled to hit the water compared with 68 in 2019.

CTI's Mr Lane adds: "So the overall supply will continue to outstrip demand. This will mean that the carriers will need to attract the additional volumes needed to fill their assets, and this is usually achieved by aggressive pricing.

"It takes only one or two itchy fingers to drop rates, and unless you are prepared to lose market share, the rest will follow, eventually."

NEW PRICE WAR BREWING

For sure, sea freight rates - a key bellwether for sentiment in the market - perked up in a significant way this year compared with last year.

This came after Hanjin filed for bankruptcy in August last year, putting a halt to an aggressive price war that had broken out. Shippers were forced to switch to carriers that could provide service reliability, and this allowed players to charge higher rates, Mr Chiang says.

He adds that the alliances that came into effect in April also helped to sustain freight rates, as shippers now have fewer options.

But in a market that is still plagued by a capacity glut, carriers will "jostle for share", says Alphaliner executive consultant Tan Hua Joo.

Rate-cutting, in fact, has already begun. Spot rates from Shanghai to Los Angeles, for example, are now US$1,078 per 40-foot container compared with $2,211 in January.

"Cosco, in particular, is expected to move aggressively to increase its market share as its operational capacity will increase from 1.8 million TEUs currently to three million TEUs by the end of 2018," Mr Tan says.

That said, this time round, freight rates may not sink to the record lows seen early last year. A long-awaited recovery is indeed in place, albeit more sluggish than expected.

"We expect 2018 to be somewhat comparable to 2017 in terms of profitability, instead of being the banner year we had anticipated earlier," says Mr Nilesh Tiwary, an equity analyst at Drewry Maritime Financial Research. "There are chances that carriers may not fully realise the benefits in 2018 due to pricing ill-discipline and a desire to protect market share. As a result, 'paradise' may be pushed back further than we previously thought."

Meanwhile, the major lines themselves have a much more buoyant outlook.

Mr Vincent Clerc, chief operating officer of Maersk Line, the world's top container shipper, said recently that the order book for the industry as a whole today is "the lowest it has been for a long time", adding that fundamentals look "quite favourable" for the years to come.

CMA CGM chairman and chief executive Rodolphe Saade voices similar sentiments. "Now that consolidation has played an important role by taking out the small-to medium-sized companies and making the others stronger and more profitable, I believe the industry is sound," he says.

"I believe that we should be heading towards better days."

Amid the slew of changes sweeping the broader industry, the Singapore port has held steady to emerge as a winner among trans-shipment hubs in the region this year.

Box traffic amounted to 27.7 million TEUs in the first 10 months of this year, up 8.5 per cent from the same period a year earlier, as a result of the major reshuffling in alliances.

Both CMA CGM and Cosco have moved a large chunk of their volumes from Malaysia's Port Klang to Singapore, notes Alphaliner's Mr Tan, who expects total container throughput here to hit 33.5 million TEUs this year, topping the 30.9 million TEUs last year. Port Klang's throughput, on the other hand, is forecast to fall to 11.7 million TEUs from 13.2 million TEUs last year.

RISKS PSA FACES

"PSA will need to protect its market share gains in 2018, especially since Port Klang will try to regain part of its lost volumes by targeting some of PSA's existing customers," he says.

Drewry lead ports analyst Victor Wai says the growth in volumes here is unlikely to persist at the same rate in 2018 now that the alliances are set to stay intact for the next few years.

The expansion of gateway ports in the region - including Kalibaru Port in Jakarta, Laem Chabang in Thailand, Manila in the Philippines and Hai Phong in Vietnam - means they are now better equipped to serve direct calls, which bypasses the need for trans-shipment.

"With a pickup in trade between these Asean countries and the rest of the world, it may be more commercially viable to make direct calls at these ports," says Mr Wai.

"Singapore may find it hard to compete when the containerised trade volumes between these Asean countries and the rest of the world expand.

"From a shipping line perspective, the network cost of making a direct call might then be lower than using a trans-shipment hub."

SEE BUSINESS

Join ST's Telegram channel and get the latest breaking news delivered to you.

A version of this article appeared in the print edition of The Straits Times on December 27, 2017, with the headline 12 months of calm seas, but.... Subscribe