For borrowers with interest-bearing unsecured debt exceeding 18 times their monthly income for three months in a row, the days of living on credit will come to an end if they do nothing.

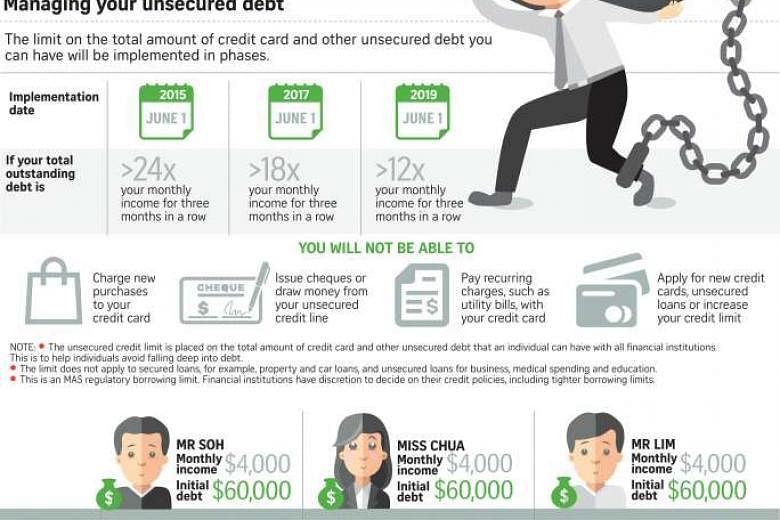

If you are caught in this unfortunate predicament, you will be unable to charge new or recurring purchases to your credit card. These include utility bills and even issuing cheques or drawing cash from your unsecured line.

You will also be unable to apply for new credit cards, unsecured loans or increase your credit limit.

The Monetary Authority of Singapore has set a limit on how much outstanding debt you can owe on credit cards and unsecured loans across all financial institutions. The aim is to help borrowers avoid falling deep into debt.

The borrowing limit is being phased in over four years, from 2015, to give indebted borrowers time to gradually cut their debts.

Since June 1, the limit on how much outstanding interest-bearing debt you can owe on credit cards and unsecured loans across all financial institutions has been cut to 18 times your monthly income for three straight months.

This will be further reduced to 12 times monthly income by June 2019 - which will be half the limit of 24 times monthly income in 2015.

Unsecured debts are those with no collateral, such as red ink run-up on credit cards, personal loans or an overdraft. This limit applies to interest-bearing balances on personal unsecured credit facilities. It excludes secured loans such as property and car loans as well as unsecured loans for business, medical and education spending.

Mr Vinod Nair, chief executive of MoneySmart.sg, said most people should not be affected by the reduced limit as there are initiatives like the Debt Consolidation Plan - rolled out in January by 14 financial institutions - that targets debtors with more than 12 months' outstanding unsecured debt.

In March, there were 32,000 borrowers with interest-bearing unsecured debt of more than 18 times their monthly income, which accounts for 2 per cent of total unsecured credit users in Singapore. Collectively, they owed $4 billion, which is 0.2 per cent of total banking assets.

This is down from 51,000 borrowers who had a similar debt threshold, owing an aggregate of $5.5 billion in February 2015. Borrowers with annual income of at least $120,000 or those with net personal assets exceeding $2 million are exempted from the industry-wide borrowing limit.

IMPACT ON AFFECTED BORROWERS

If a borrower had been using his unsecured credit to pay for some of his living expenses or to fund his lifestyle, he may no longer be able to do so with the reduced unsecured debt limit, said Credit Counselling Singapore's (CCS) general manager, Ms Tan Huey Min.

Painting a bleak picture, she said: "He will have to live with only his monthly income while at the same time pay down his unsecured debts. This means he is likely to be cash-strapped and may turn to alternative lenders, for example, licensed moneylenders.

"But borrowing to make repayment or borrowing to pay for living costs (especially from a more expensive lender) will lead only to bigger debts and hence bigger problems. It would be worse if he were to turn to unlicensed moneylenders. The debt collection actions will cause pressures and distress to the borrower."

Ms Tan added that this could lead to low productivity at work, embarrassment and even job loss if the collectors keep calling or even visiting the debtor's office. And it could create tensions at home owing to money shortage and unpaid bills.

"Should the borrower lose his job and/or become depressed, this implies potential family/social problems, as the family could break down or he could become suicidal," she added.

On a brighter note, Mr Matthias Dekan, head of customer value management, HSBC Bank (Singapore), said that despite the initial disruption faced by affected borrowers, he believed they would be able to work out the appropriate repayment plans or give their latest income records.

HELP FOR BORROWERS

Borrowers who exceed the 18 times borrowing limit can expect to get warning letters or text messages from their financial institutions every month for three straight months, starting from June 1 this year. Their unsecured credit facilities will be suspended by Aug 31 if their unsecured debt remains above 18 times monthly income. Here are some steps borrowers can take:

•Update your latest income records with the financial institutions. Mr Desmond Tan, head of lifestyle financing, OCBC Bank, advises bank customers to have a habit of updating their latest income records to avoid any inadvertent suspension of their credit cards and unsecured loan accounts arising from outdated income information.

•Debt Consolidation Plan (DCP) This offers the convenience of bringing together all unsecured outstanding balances from multiple accounts with all the banks, and consolidating them into one monthly instalment repayment plan at an affordable interest rate. Mr Anthony Seow, head of cards and unsecured loans at DBS Bank, said: "In most scenarios, you would also have a lower monthly instalment amount to repay compared to managing different accounts individually. For example, someone without DCP would likely be paying around 3 per cent of their total outstanding on a monthly basis at an effective interest rate in excess of 20 per cent per annum. "With DCP, the monthly repayment would be around 2 per cent of their total outstanding and at an effective interest rate in excess of 10 per cent a year onwards."

•Other solutions. Ms Tan said CCS offers free talks to explain various other solutions, including the dos and don'ts for handling a debt situation and the common collection actions taken by creditors.

Debtors who do not qualify for DCP and/or are clueless about drawing up and living within a budget should get information on debt management as well as advice.

Ms Tan advised these borrowers to visit the CCS website (www.ccs.org.sg) to register online and attend a free talk on debt management to learn how to manage a debt problem.

They can also have a one-to-one session with CCS to discuss their finances, work out a monthly living budget and explore suitable solutions to address their debt problems.

To request a one-to-one debt advising session, a debtor first needs to have attended the free info talk and submitted their counselling request package to CCS.

Where applicable, they would be assisted in working out a monthly instalment debt repayment plan via CCS' debt management programme. This programme will make provisions for his monthly living expenses and, at the same time, set aside sufficient money to make monthly instalment repayment to gradually discharge his debt obligations.

In other words, he would be on the debt recovery journey and become debt-free one day.