How the times have changed.

Four years ago, engineering and property development firm United Engineers (UE) was riding high after launching an audacious but ultimately successful bid for WBL, emboldened by the support it had received from its biggest shareholders.

Its acquisition was a company then larger than it was by market value, which it then delisted from the Singapore Exchange.

However, in an unusual twist of fortune, those same shareholders have now put their stake in UE on the block and picked a consortium led by a far younger property firm, Perennial, for final talks to buy it.

Not that there is anything wrong with that move. If UE's biggest shareholders - OCBC Bank, its insurance unit Great Eastern and the bank's founding Lee family - feel that they are better off selling their respective UE stakes and putting the money to better use elsewhere, they should do so.

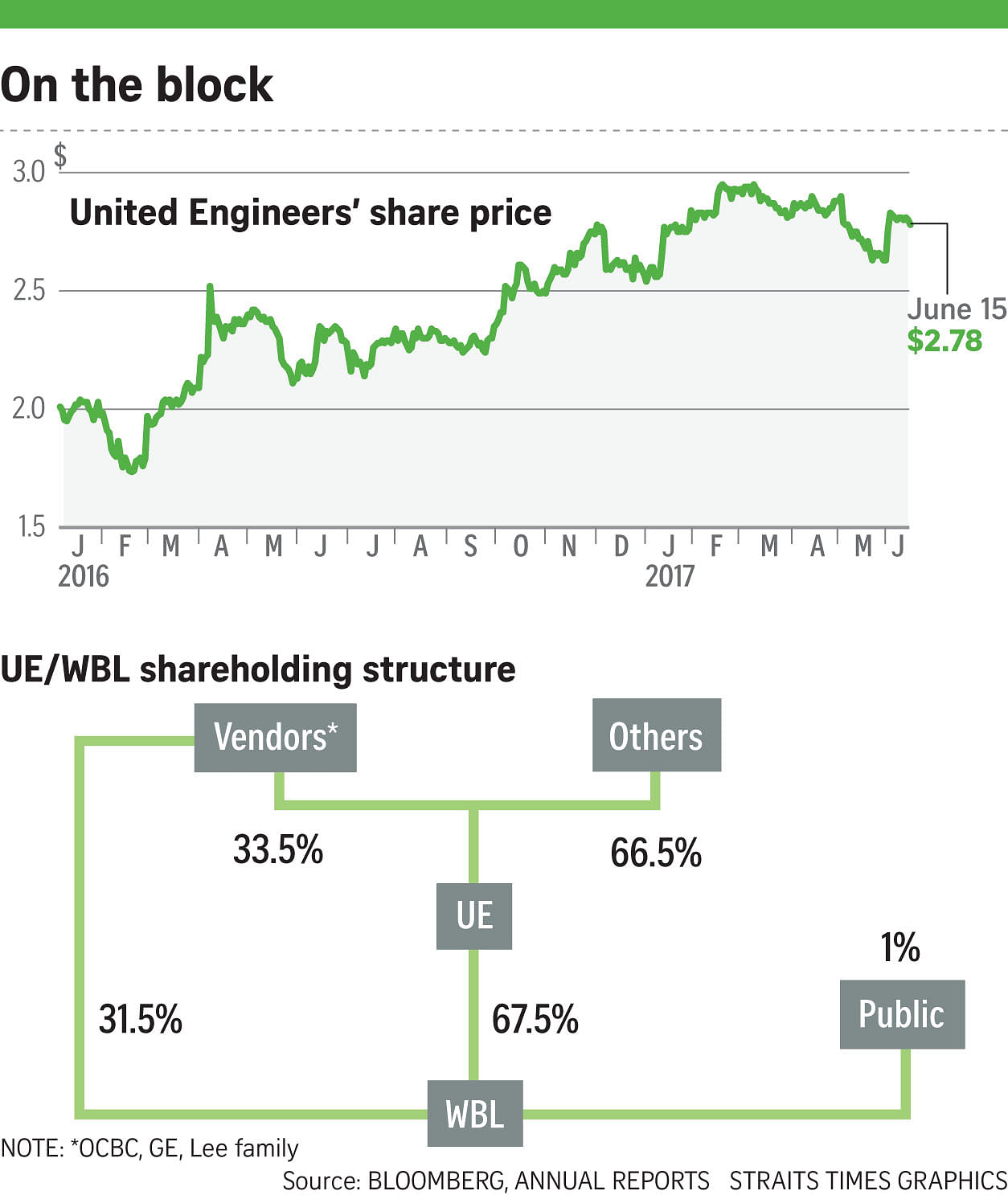

Since the news broke in January of a possible sale, the price of UE had surged by about 8 per cent. Last Friday, it ended one cent higher at $2.78, with 1.58 million shares traded. Yet, any attempt by the shareholders to sell their UE stakes may not be a straightforward exercise, as they also want to offload their WBL stake. That may, in turn, have an impact on the options which a UE shareholder has in the event a takeover on UE materialises.

Before delving further, it is useful to recount what transpired during UE's takeover of WBL four years ago.

Prior to that takeover, WBL had also shared the same group of major shareholders as UE - that is, OCBC, GE and the Lee family.

But that all changed when Straits Trading - also previously affiliated to OCBC - made a takeover bid for the rest of WBL when it mopped up stakes in the then listed property-cum-motor group belonging to fund managers.

UE then entered the takeover tussle for WBL with the support of its major shareholders.

It emerged as victor with about 67.5 per cent of WBL shares after Straits Trading threw in the towel, while most of the rest of WBL shares continued to be held by OCBC, GE and the Lees.

Since it took over WBL, UE has been remaking itself into a property play, selling off non-core assets, such as Singapore luxury car distributor Wearnes and Nasdaq-listed unit MFlex, which had come with the WBL purchase.

It property portfolio, worth about $1.8 billion, includes UE BizHub City, UE BizHub West, one-north mixed developments, as well as property development projects in China.

The story then took another twist in January this year when OCBC and GE said that they were reviewing their stakes in UE and WBL - a euphemism to flag that they wanted to sell out.

Under Singapore's takeover rules, any party which acquires more than 30 per cent of a company must make an offer to buy up the rest of its shares. This rule applies to both listed and unlisted firms.

In this case, the stakes which OCBC, GE and the Lees own in UE and WBL are well above the 30 per cent takeover threshold. As such, if they sell their UE and WBL stakes to a single buyer, that buyer would have to make simultaneous offers to buy up the rest of UE and WBL shares. At current market prices, UE is worth about $1.72 billion, while WBL was valued at as much as $1.25 billion when UE took it private four years ago. Therefore, a buyer will have to prepare as much as $3 billion to mount both takeovers simultaneously.

That would be a big strain on his financial resources, no matter how attractive UE's assets may be.

This may explain why Perennial is said to be seeking clarification from Singapore regulators on the procedures for a simultaneous purchase of the three parties' holdings in UE and WBL.

According to market sources, in order to lessen the financial burden, one possible pathway for the buyer is to first purchase the stakes in UE belonging to OCBC, GE and the Lees.

In doing so, he would trigger a takeover order on UE.

As for buying up the three parties' stake in WBL, that will be taken care of if the UE takeover turns mandatory after crossing the 50 per cent level, which gives the buyer undisputed control over UE.

Owing to a rule on chain listing, this change of ownership in UE will require the buyer to make an offer for WBL.

But, here, the situation gets a little tricky: With this takeover offer on WBL, OCBC, GE and the Lees will be able to offload their WBL stakes to the buyer. But in order to reduce his cash outlay, the buyer may want UE to undertake that it will not accept the takeover offer to sell its 67.5 per cent stake in WBL.

This raises governance concerns.

For the UE's board of directors to give such an undertaking on behalf of the company, it must satisfy itself that the shareholders are better off if UE does not cash out of WBL.

But some UE shareholders may be reluctant to accept the offer made by the buyer for their UE shares. They may also prefer to hold on to the UE shares in the hope of collecting any special dividend payout, which the company would be in the position to make if it sells out of its WBL stake.

There is also the awkward question as to why UE should lock itself up with an undertaking not to sell its WBL stake, when other WBL shareholders can keep their options open as to what to do with their shares.

Then there is the regulatory aspect to consider. The Securities Industry Council, which administers the takeover code, may want the UE board to give a written confirmation that the company has not received any form of "inducements" for undertaking that it would not be selling its 67.5 per cent stake in WBL to the buyer.

Suffice to say, the various issues that may arise are likely to put the UE board between a rock and a hard place.

But my take is that if push ever comes to shove and the scenario which I describe does indeed pan out, the best recourse for UE is to hold an extraordinary general meeting in order to allow its shareholders to decide what they want to do with the WBL stake.

After all, as shareholders, they deserve to be given an opportunity to exercise their rights with regard to any takeover offer on WBL.

That can only be good corporate governance.