Break-ups can come as a surprise: The United Kingdom's vote to exit the European Union after 43 years was shocking, unleashing a risk-off tsunami that sent investors scrambling for the exit.

About US$2 trillion (S$2.7 trillion) was wiped off share markets worldwide on the first trading day following the referendum, making it the largest one-day sell-off on record.

The British pound sank to its lowest level against the US dollar in 31 years. And safe havens including gold and the yen have soared.

The carnage to asset prices has lessened, however, as pledges by global central banks to maintain the proper functioning of financial systems has calmed nerves. Markets like the US and Asia, while not spared from the initial shockwaves, are poised to weather the economic storm better than Britain and Europe.

The Brexit rout has opened up new opportunities and closed others, so investors must be selective and focus on quality.

GLOBAL IMPLICATIONS

For Britain, sharply lower growth, a large drop in the pound and further easing from the Bank of England (BoE) are just a few of the notable implications from the Brexit vote.

With the Britain-EU trading relationship and domestic political parties in flux, protracted uncertainty is expected to cloud Britain's economic sentiment for some time.

Economic growth will decelerate to around zero for the second half of the year at best, likely triggering the BoE to cut policy rates twice to zero and make further asset purchases - it has already earmarked an additional £250 billion (S$446 billion) of liquidity to cushion the blow.

In the next three to six months, the sterling could head towards $1.30 against the US dollar.

A weaker pound is an earnings tailwind for the more internationally exposed FTSE 100, which should outperform the FTSE 250; small and mid-cap stocks will likely bear the brunt of the negative growth shock. And BoE easing should continue to keep gilt yields low in the immediate term.

The impact on the EU will largely depend on the amicability of exit negotiations and the bloc's ability to further integrate in the face of populist movements bubbling across Europe.

Economic contagion should be largely contained, thanks to the European Central Bank's (ECB) firm commitment to maintaining order.

The ECB's easing stance and low credit default rates should continue to support European high-yield credit, and positive returns are expected in the coming months. The euro will follow the sterling lower against the dollar, likely reaching US$1.08 in three months.

While US equities were largely sold off in the aftermath of the vote, they have since started to recover as investors regain confidence amid a tightening labour market, which supports consumption.

The US also has limited export exposure to Britain (3 per cent), but the ensuing US dollar strength is a potential headwind to earnings. The explosion of uncertainty will also likely deter the US Federal Reserve from tightening its monetary policy too soon; instead of two hikes this year, we now expect only one in December.

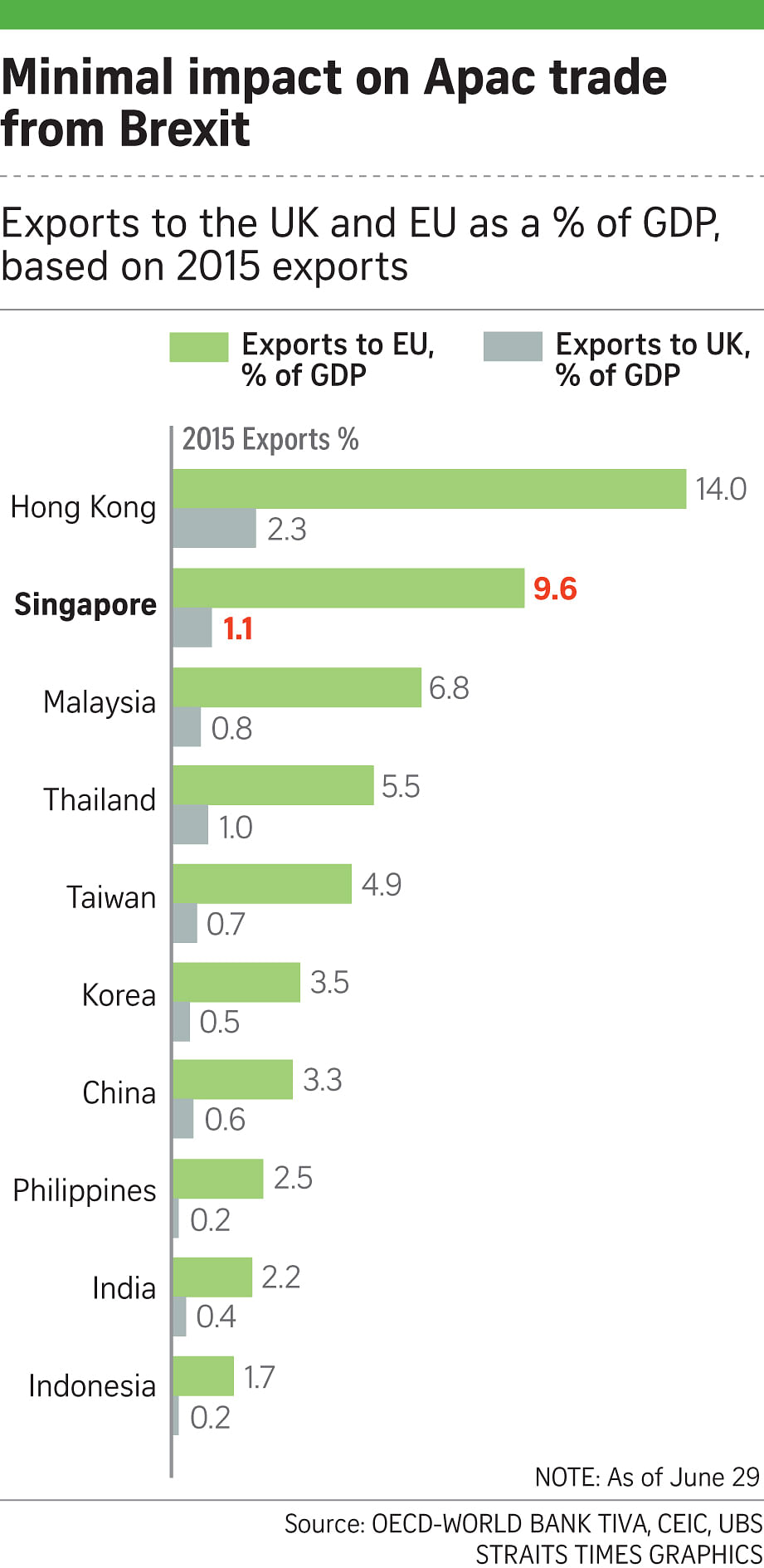

IMPACT ON ASIA

Two factors in particular should help Asia withstand a Brexit thrashing: limited direct exposure to Britain and hardy corporate fundamentals.

The impact to the region's economic prospects will be largely mitigated by strong monetary policy support from Asian central banks and the small share of Britain-bound exports (2 per cent) from Asia ex-Japan (AxJ).

While the EU is the larger trading partner (15 per cent of AxJ exports), the drag to Asian gross domestic product growth should be contained at no more than 0.5 per cent, according to our estimates, if Europe's economy deteriorates more severely.

Corporate balance sheets and cash-flow generation in Asia are also far superior now, compared with previous crises in 2008 and 1997, and revenue exposure to Britain across most Asian markets is only in the low single digits. So any undue sell-offs should be used as an opportunity to invest in Asian quality growth companies such as Chinese Internet and new economy stocks, and defensive equities with attractive yield such as telcos.

But within Asia, Taiwan and Korean equities and sectors more exposed to Britain, such as Hong Kong utilities, Indian steel and autos, and regional tech and airlines, should be avoided.

In Asian investment-grade credit, we prefer Asian bank Tier-2 subordinated debt, non-bank financials and shorter-dated China state-owned enterprise bonds. In high yield, the China new- economy sectors still provide compelling returns.

The region's currencies will likely feel the brunt of the heat from Brexit. The US dollar is expected to strengthen about 3 per cent to 5 per cent versus Asia-Pacific currencies in the near term, against a backdrop of heightened market uncertainty and fragile risk sentiment.

Within the region, the Chinese yuan, Indonesian rupiah and Indian rupee should outperform relatively. The Chinese yuan continues to be managed closely against a trade-weighted basket of currencies - which implies modest weakening against a strengthening US dollar - while the Indian rupee and Indonesian rupiah are relatively shielded from Brexit's negative global trade implications.

On the other hand, we expect the Singapore dollar, Korean won and Taiwan dollar to underperform on sluggish growth and subdued inflationary pressures, which could prompt further monetary stimulus later this year.

We now expect the Singdollar to trade to US$1.41 over the next 12 months and the three-month Sibor (Singapore interbank offered rate) to rise to 1.5 per cent from 0.9 per cent now over this same period.

OPPORTUNITIES EMERGING

While uncertainties and volatilities will remain elevated, Brexit is unlikely to result in another global financial crisis - not when global central banks are standing ready to contain the financial fallout.

There is also sufficient momentum among consumers in the United States, Europe and key parts of Asia to help avert a global recession.

Tactically, there are sufficient areas of resilience to support a modest risk-on position. Over the next six months, we think risk assets, including US equities, US investment-grade corporate bonds and European high-yield bonds, will likely end the year higher from current levels.

Thematically, euro-zone dividend stocks could outperform euro-zone equities, while British real estate stocks also appear better positioned versus their European real estate peers.

- The writer is the Apac regional head at the chief investment office of UBS Wealth Management.