Economic cycles are an investing reality. Financial markets rise, peak, decline, bottom and start all over again. Sometimes this occurs in the span of five to seven years, while at other times, like the secular global bond bull market, the upswing has lasted for over 30 years. For investors, a right call on the cyclical positioning of markets can make all the difference to portfolio returns.

So where are we in the current cycle? After a tumultuous start to 2016, Asian markets have been powering ahead since February. The MSCI Asia ex-Japan Index is up about 15 per cent so far this year alone, led most recently by positive surprises in global and Chinese activity data and fading concerns over Sino-US tensions and an overtly hawkish US Federal Reserve. Macro indicators worldwide are pointing to a synchronised upswing, and Asia is poised to benefit from the recovery in global trade and the region's easy monetary policy.

It is clear recent economic data has surprised markets to the upside, but economists remain divided on the pace and sustainability of this recovery. We think Asia is currently in the early- to mid-innings of the economic cycle, which support further upside in asset prices. And as the recovery broadens out into an expansion, your best bet is with cyclicals.

ASIA'S EXPANSION STILL HAS ROOM TO RUN

Globally, financial markets have been riding the tide of good news: the Dutch snubbed populism, the Fed hiked again in the light of its positive view of US and global economic conditions, and President Donald Trump has lately avoided anti-China, anti-trade rhetoric. Meanwhile, macro indicators have soared - US consumer confidence is at a 15-year high, US small-business optimism is near its best reading in 43 years, and European PMIs have shot up to six-year highs.

Asia's export growth too has recovered from its trough in the first quarter of 2016, when it shrank, to rise 5 per cent year on year in February. The strong trade momentum is likely to continue and result in export growth of about 10 per cent this year, roughly half of which will be volume-driven and the other half from the recovery in producer pricing. This is particularly important in Singapore, given its open and trade-dependent economy; the Straits Times Index's 8 per cent year-to-date rally has exceeded expectations, making it one of the region's best-performing markets, at least in Asean.

Given the supportive backdrop, a rekindling of investment is the next big thing that will extend this year's economic expansion. Conditions will likely fall in place starting from the second half of 2017. Already, we are seeing early signs of a modest recovery in bank credit growth, stronger corporate profitability and faster imports of capital goods. In addition, the declining real cost of capital for companies, better capitalised banks and subdued inventory positions should provide legs to the economic expansion.

And in China, long the bellwether of Asia's economic vigour, stronger infrastructure spending, a recovery in private investment and a surge in housing activity have recently led to more bullish expectations. UBS economists recently upgraded China's 2017 gross domestic product growth estimate to 6.7 per cent from 6.4 per cent. While the sustainability in housing activity remains ambiguous, the firming external environment and solid fiscal support should keep its economy humming throughout the year.

CYCLICALS ARE YOUR BEST BET AS EARNINGS JUMP

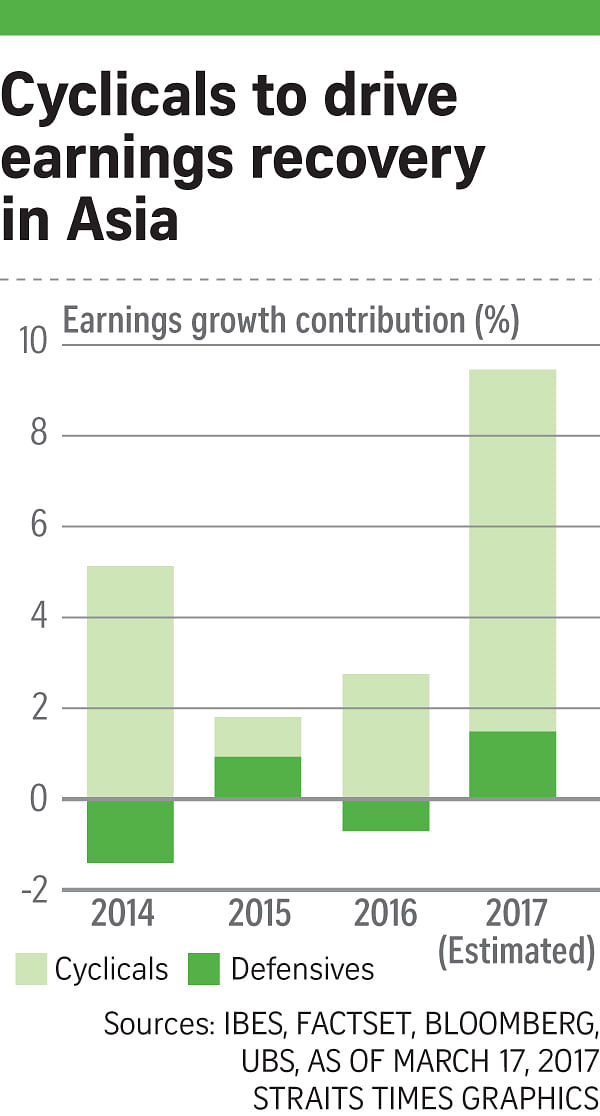

In the US and Europe, cyclicals account for about 60 per cent of the benchmark indices, while in Asia, the exposure to cyclicals is disproportionately higher and concentrated in five sectors - consumer discretionary, financials, industrials, IT and materials. In aggregate, cyclicals make up 80 per cent of the region's benchmark index and 85 per cent of earnings.

This high cyclicality has been a drag on Asian markets' performance in recent years as earnings growth and return-on-equity (ROE) ratios came under pressure. This year, cyclicals will likely be at the forefront of regional markets' rebound. Besides the surge in trade and the capex recovery on the horizon, the general state of reflation (that is, higher inflation backed by stronger economic growth) should drive a strong earnings recovery. Asia's earnings growth is strongly correlated to nominal GDP growth, and nominal GDP in Asia is set to increase by 2 percentage points this year, thanks to stronger real activity and, importantly, the end of producer price deflation.

In Singapore, earnings growth and ROE are at an inflection point, with the consensus expecting 6.1 per cent earnings per share growth in 2017 following two years of declining earnings. That said, the Singapore equity market remains neutral in our tactical asset-allocation strategy as we see stronger earnings recovery and better valuations elsewhere in the region.

THE SECTORS POISED FOR OUTPERFORMANCE

We are still at an early stage of the US interest-rate normalisation path, which remains supportive of the Asian business cycle. Despite the recent outperformance, risk-reward for Asian cyclicals remains attractive as their solid earnings recovery, improving balance sheets and relatively attractive valuations should become more apparent as the cycle progresses.

Across Asia, the key beneficiaries will likely be financials, IT and materials stocks, and our tactically overweight markets of China, India and Thailand. In Singapore, financials, real estate and consumer discretionary sectors are set to outperform the broad local market. Banks, in particular those in India, Indonesia, Hong Kong and South Korea, offer the best risk-reward amid reasonable valuations and an improving earnings outlook. In China, insurers look more appealing than banks, thanks to better fundamentals and more attractive valuations.

To be sure, investors should also be mindful of the risks that could cut this cyclical upswing short. Politics in Europe could still shift right, while Trump-related risks in the form of significant disappointment over the US fiscal agenda or Sino-US flare-ups could roil markets. Barring these external risk events, Asian cyclicals look set for a strong rebound in the next 12 months.

• The writer is the Apac regional head at the chief investment office of UBS Wealth Management.