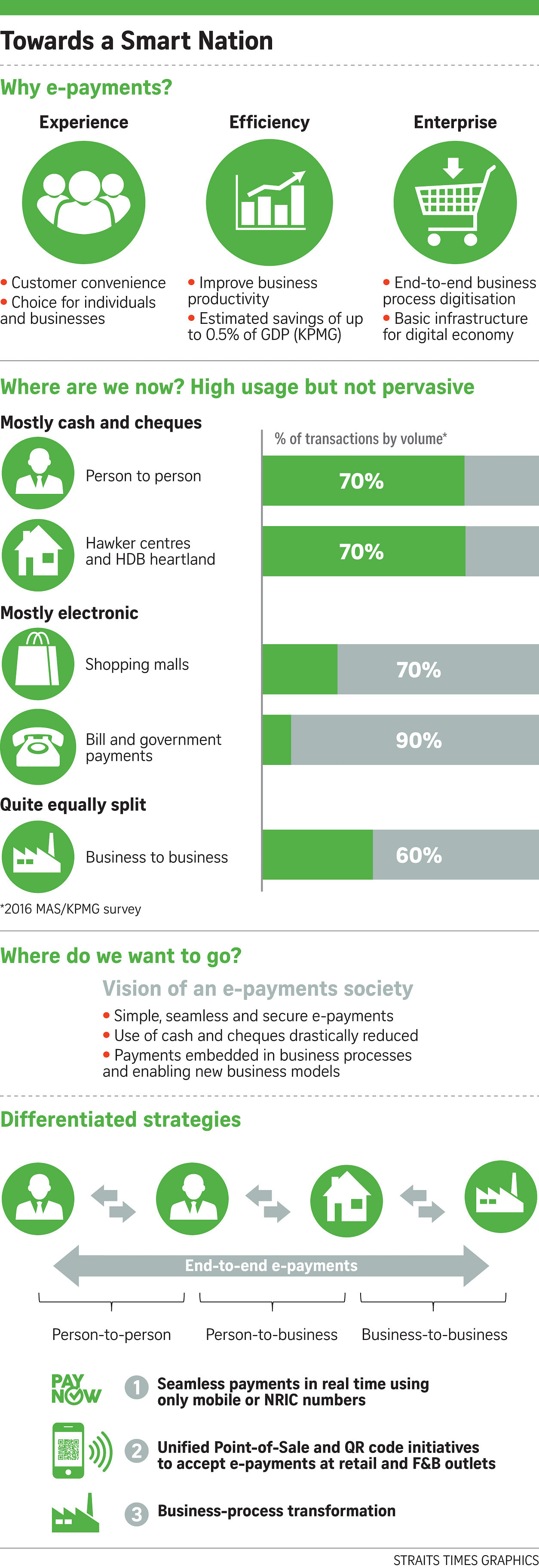

Singapore prides itself on being at the forefront of technology and innovation but, when it comes to paying for goods and services, the adoption of electronic payments has not taken off as fast as it has in countries such as China and India.

Consumers here still prefer cash options such as notes and coins; some continue to use cheque books.

Statistics show that generally six in 10 consumer transactions are made in cash here. At hawker centres and in the HDB heartland, the figure rises to 70 per cent.

On the bright side, e-payments are now more common at malls, where 70 per cent of transactions are electronic. And nine in 10 people pay their bills and government payments electronically.

The drive to be a Smart Nation took centre stage along with two other longer-term issues - early education and fighting diabetes - in Prime Minister Lee Hsien Loong's National Day Rally speech last month, so greater adoption of technology is clearly seen as important.

When it comes to payments, cash is not king. Cash and cheques impose a large cost on society and not just in terms of the printing expense, which is small, said finance experts. The greater proportion of the cost comes from storing, transferring and reconciliation/counting of the cash, especially at cash counters. There is also the cost of incineration for, say, unwanted notes.

Think of the hawker or taxi driver who has to ensure that he has cash on hand as well as take time to sort out change for every customer, holding up other users.

In contrast, e-payments have taken major Chinese cities by storm. It is common to see people there scanning a quick response (QR) code and using digital wallets Alipay and WeChat Pay to transfer their money. Linked to users' bank accounts, these services are widely accepted at retail points and roadside stalls and in taxis.

In India, the government pushed for a national digital fund transfer system, called Bharat Interface for Money, and a biometric identification system, dubbed Aadhaar, to secure transactions. By doing so, it aimed to ensure that all Indians, including the rural poor, would have access to financial services through digital banking.

Here, the Singapore Government wants an e-payment system that is simple, seamless and secure, with the use of cash and cheques drastically reduced.

Individuals would enjoy greater convenience, and e-payments embedded in business processes would enable innovation. This could change for the better the way businesses are run, resulting in higher levels of productivity and cost savings.

Such moves would be made possible with a basic infrastructure for a digital economy and a positive attitude towards change.

WHAT NEEDS TO BE DONE?

Mr Aditya Gupta, who heads e-business for Singapore at OCBC Bank, believes that, for the country to go truly cashless, we need to avoid fragmentation arising from closed loop systems. In such systems, the merchant and customer need to be with a single bank or organisation to facilitate the payment.

"We prefer open, nationwide infrastructures that have universal acceptance across Singapore, and that multiple bank users can ride on together," says Mr Gupta.

"Hence, for our OCBC Pay Anyone app, we are working with Nets and other international schemes to provide universal acceptance."

Mr Yuen Kuan Moon, who is chief executive of consumer business here at Singtel, says Singapore has all the "right ingredients" for a thriving mobile-payment market - a strong regulatory framework, reliable and ultra-fast mobile networks, secure and safe platforms, and one of the world's highest smartphone penetration rates.

"However, the rate of mobile-payment adoption is disappointingly low - perhaps because the landscape is fragmented, with multiple online and offline payment systems available," he notes.

"There is a recognised need to drive adoption on a common platform," he adds.

Singtel is part of an industry task force looking into developing a standard QR code for Singapore.

A QR code is a square barcode that is used to scan all sorts of data onto smartphones.

In 2014, Singtel launched a mobile digital wallet, Dash, which provides secure mobile payments for anyone here with a smartphone.

Mr Yuen notes: "Once we address challenges such as regulatory hurdles and multiple front-end user interfaces, we see Dash as (being) the digital wallet behind PayNow."

He adds that Dash can accept systems such as payWave and any of the payment codes that "hawker centres are likely to deploy".

PAYNOW

Started in July, PayNow is a concerted nationwide effort by the financial services industry here to simplify and standardise the way customers can pay and be paid.

It enables customers to pay others by keying in the recipient's mobile or NRIC number. This does away with the need for the recipient to share bank account numbers, which they might not have at hand.

And the sender can make payments instantly via mobile phone, says UOB's head of personal financial services for Singapore, Ms Jacquelyn Tan.

OCBC's Mr Gupta adds that PayNow lets people link accounts at any of the seven participating banks to their mobile phones or NRIC numbers.

OCBC has integrated OCBC Pay Anyone with PayNow.

"This means that, when an OCBC customer makes a money transfer using OCBC Pay Anyone, the recipient no longer needs to 'collect' the money by entering the six-digit passcode (created by the sender) and their bank account number," Mr Gupta points out.

"Instead, the sender can just input the recipient's mobile number when making the OCBC Pay Anyone money transfer, or make the payment by simply scanning a QR code using the OCBC Pay Anyone app. The money will then be transferred directly to the recipient's bank account."

Mr Anthony Seow, DBS Bank's head of cards and unsecured loans, says the industry as a whole has surpassed 500,000 PayNow registrations, with DBS/POSB taking almost half of the market share.

He adds that DBS PayLah! is leading the pack for mobile wallets with more than 600,000 users since its launch in May 2014.

"More than 10,000 transactions are made daily by our users. For PayNow, we've had more than 350,000 users registered since it was launched, which comes to around 47 per cent of the total market share," he says.

Mr Gupta notes that PayNow has reached an inflection point in Singapore's drive to become a cashless economy. The adoption of e-payments and PayNow among OCBC customers has been exceptionally strong.

"Customers are also loving the added convenience of PayNow integrated with OCBC Pay Anyone. We have over 200,000 sign-ups for PayNow - as a percentage of overall industry sign-ups, that is higher than our natural market share of customers," he says.

OCBC Pay Anyone transactions have increased 35 per cent since the launch of PayNow. One in two such transactions is done via OCBC Pay Anyone. Since last year, e-payments on this platform have gone up 12-fold in dollar value.

NEW DIGITAL KEYBOARDS TO MAKE TRANSACTIONS EASIER

To make PayNow even more seamless and integrated into our lives, OCBC has introduced OCBC Keyboard for Android phones, while UOB launched UOB MyKey recently as well.

These mobile keyboards enable customers to make PayNow transfers directly within any mobile or social networking app such as WhatsApp or Facebook Messenger.

All you need to do is switch to the specific keyboard to initiate the payment directly within the keyboard field.

UOB's Ms Tan says there has been a strong response from its customers since the service was launched on July 10. Even though the PayNow fund transfer service is available through Internet banking as well, more than 90 per cent of the PayNow transactions by UOB customers are made using mobile phones.

KEY MILESTONES

Common QR code for Singapore (SGQR): A task force set up to promote e-payments is working on creating a common QR code for Singapore (which could be used for e-payments islandwide).

A common code, which PayNow would be able to ride on, could be ready by the end of the year.

The aim is for merchants to display just one QR code, which could be scanned by any bank app - DBS PayLah, UOB Mighty and OCBC Pay Anyone - for fuss-free, instant fund transfers.

The common QR code is expected to accept both domestic and international payment schemes.

This initiative could put Singapore ahead of China, where merchants that accept Alipay and WeChat Pay have to display two separate QR codes as the two systems do not inter-operate.

The use of QR code-based payments is advocated as a practical and convenient way to facilitate payments for various payment schemes and e-wallets such as DBS PayLah! and Singtel's Dash, as well as for banks.

QR codes are already being used for e-payments. DBS, for one, has been encouraging small cash-based merchants such as hawkers and market vendors to adopt such codes as a payment method.

This is how it works. At the point of sale, the buyer scans the merchant's displayed QR code with his phone. This automatically displays the merchant's name in, say, the DBS PayLah! app, and the buyer can then enter the payment amount. The payment is deducted from the buyer's DBS PayLah! wallet and transferred to the merchant's.

DBS introduced QR code payments here in April and, in the process, it also launched a partnership with ComfortDelGro taxis to encourage commuters to use the new system.

The cabs now see around 15,000 QR code transactions a month via the DBS PayLah! app.

The common QR code initiative is timely as many customers and merchants are confused about which payment methods to use given the various standards and multiple codes at points of sale.

National digital identity (NDI) system: Over the next three years, a new system will be introduced to allow Singaporeans to do away with hardware tokens or one-time SMS passwords.

The NDI - which will be on trial over the next six months - will build on the existing SingPass system, set up in 2003 to allow access to e-government services.

The Senior Minister of State for Communications and Information, Dr Janil Puthucheary, has said that this initiative will take SingPass and elevate its usability, security and inter-operability so that, digitally, it can achieve what the NRIC does today.

SingPass includes the use of one-time passwords. These are generated by the government-backed OneKey hardware token launched in 2011, or sent via SMS. But such options can be inconvenient, and might be hijacked by hackers.

The NDI will entail a phone app that provides encryption for authenticating a person's identity online securely without the hassle of carrying another device.

The move is consistent with recent efforts by some banks to ditch hardware tokens in favour of software-based ones for convenience.