The first quarter delivered two surprises: faster-than-expected vaccine roll-outs and a bigger-than-expected United States fiscal stimulus package.

The backdrop of vaccination-led economic reopening plus substantial stimulus will likely pave the way for major economies to enter the reflation phase of the recovery in the second quarter.

This period will likely be characterised by high economic growth, rising inflation, low interest rates and persistent volatility. We remain pro-risk in both equities and credit markets.

About 28 per cent of the US population and 10 per cent of the European Union 27 population are likely to have received at least one dose of the vaccine by the end of the first quarter. At the current rate, the figures will climb to 70 per cent and 40 per cent, respectively, by the end of June. Vaccination drives in Asia are also gaining pace swiftly.

At the start of the year, few expected further substantial US fiscal stimulus. But the Biden administration managed to secure approval for its US$1.9 trillion (S$2.6 trillion) fiscal stimulus package in its entirety, overcoming pressures for a far smaller package.

The upshot is that growth expectations are being revised up.

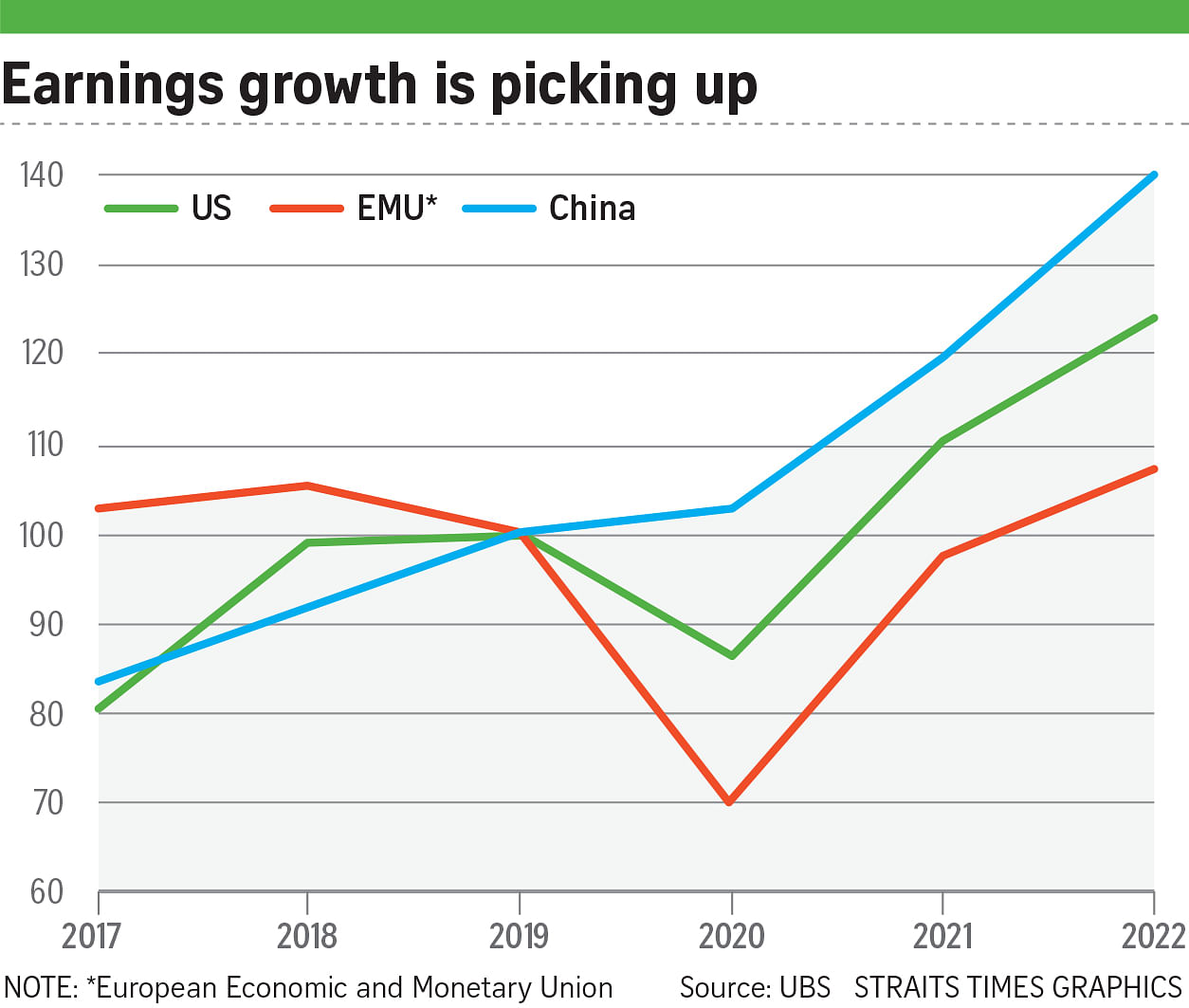

We expect gross domestic product (GDP) to be 9 per cent higher in the US by the end of next year compared with the end of 2019, 3 per cent higher in the Euro zone and 18 per cent higher in China. Similarly, corporate earnings look set to be 24 per cent higher in the US next year compared with 2019, 7 per cent higher in the Euro zone and 39 per cent higher in China.

The prospect of accelerating growth as well as an expected spike in inflation has also pushed yields higher. The 10-year US Treasury yield has risen 85 basis points since the start of the year to 1.75 per cent, while the federal fund futures market is now pricing in one rate hike late next year followed by two more in 2023.

We expect yields to rise further, with the 10-year US Treasury yield reaching 2 per cent by the end of this year, but we do not see this creating problems for risk assets.

The most rapid adjustment in yields appears to be behind us, in our view.

Yields are also rising for the right reason - higher growth. Contrary to market pricing, the US Federal Reserve has reiterated that it has no plans to raise rates until the end of 2023 and is willing to let the US economy "run hot" for a while.

With policy rates on hold and long-term yields higher, the yield curve will likely steepen further.

We also share the Fed's view that the spike in inflation is transitory and due to base effects, as well as demand-supply mismatches caused by the Covid-19 pandemic.

Against this backdrop, we think risk assets will continue to perform well and recommend the following strategies:

POSITION FOR REFLATION

We recently raised our forecast for the end of this year for the S&P 500 to 4,200, and believe cyclical sectors will benefit particularly from economic reopening.

Rising yields may also continue to drive a rotation out of momentum stocks into value stocks.

Reflation beneficiaries that look set to get a tailwind from easing mobility restrictions and a steepening yield curve include the financial and energy sectors, while reopening winners include small-and mid-cap stocks.

Reduced credit risk, increasing shareholder distributions and steeper yield curves support financials, which are one of the most attractively valued sectors globally.

Energy stocks should benefit from the recovery in oil demand; we expect Brent crude to rise to US$75 a barrel by the year-end.

Within Asia, Singapore and India are among our most preferred markets due to their catch-up potential. Singapore banks should benefit from both reopening and reflation, making them a favoured sector regionally.

Leading Chinese Internet platforms are candidates to buy on dips following their recent sell-off, as the country forges ahead with digitalisation. We think consumer discretionary stocks in Asia are a notable opportunity.

Investors should also consider commodities, including oil, copper, and palladium, which are beneficiaries of faster economic growth and can help hedge against the risk of more persistent inflation.

HUNT FOR YIELD

Now more than ever, investors are deeply divided over the outlook for longer-term interest rates and inflation as global GDP growth rebounds and central banks keep policy rates on hold.

In the meantime, real rates of interest (after inflation) on the safest bonds look set to remain negative, making the hunt for yield increasingly challenging.

Still, we see opportunities in US high-yield and senior loans, which tend to benefit from an accelerating economy and have historically been more resilient than investment-grade bonds to rising rates. Dividend stocks are another alternative, as firms that cut payouts last year increase them again as profits recover.

Asia also provides some of the most compelling yield opportunities. Asia US dollar high-yield credit could deliver total returns of 7 per cent to 8 per cent by the end of the year.

Chinese government bonds have a 10-year yield-to-maturity of 3.2 per cent compared with 1.6 per cent for similar tenors in the US and minus 0.3 per cent in Europe. On a 12-month view and on the back of a faster normalisation of monetary policy, the Chinese renminbi should appreciate relative to the euro and the US dollar.

The transition into a reflationary environment, risks of potential shifts in fiscal and monetary policies, increased institutional and retail activity in the options market and the rising share of growth stocks in major indexes all suggest continued elevated volatility in the coming months.

Pre-profit, early stage and expensive tech stocks are likely to remain vulnerable to volatility in rates. But not all tech companies are equal - some are cyclical, and others are cash generative and profitable, which puts them in good stead in this new market regime.

The key is to manage downside risks while staying exposed to long-term secular tech disruption themes such as 5G, greentech, fintech and healthtech.

Investors should use periods of high volatility to phase into large-cap tech firms with established business models and revenue visibility. We also like cyclical semiconductor and memory chip makers that are now benefiting from tight global supply, as well as digital subscription models that are already demonstrating steady revenue growth and cash-flow generation.

• The writer is the Asia-Pacific head of UBS Global Wealth Management's chief investment office.